Why Investing Is Hard, Part 2: The Psychology of Flinching

Loss aversion, overconfidence, and the disposition effect - the research on why investors lose to themselves, the platforms that profit from it, and the guardrails that hold

“The investor’s chief problem, and even his worst enemy, is likely to be himself.”

— Benjamin Graham

Part 1 was about the game; this is about the player, and Graham named the problem decades ago. There I covered the structural half: volatility as the price of admission, markets that price in news faster than you can act, costs that compound against you, and leverage that turns temporary mistakes into permanent ones. Demanding, but learnable. A disciplined robot could handle all of it. You are not a disciplined robot, and neither am I.

The average investor’s biggest enemy isn’t the market; it’s their own behavior: panic selling, performance chasing, and over-trading, amplified by platforms engineered to reward activity. None of these are character flaws; they are predictable outputs of human wiring, and I can show you each one in my own ledger.

This second part is about that wiring - why good investing decisions feel wrong in the moment, how the industry monetizes that discomfort, and what a system that protects you from yourself actually looks like. It also closes the arc that started with lifestyle inflation: build slack, defend it from your own psychology, deploy it without flinching. The people who do best aren’t necessarily the smartest; they’re the ones who design their process so they don’t have to win a daily fight with themselves.

Your Brain Was Not Built for This

Investing is hard because it forces you to bet against your own instincts, and the instincts are not subtle.

Start with loss aversion, the foundational finding of behavioral finance, established in Daniel Kahneman and Amos Tversky’s 1979 paper on prospect theory: losses hurt roughly twice as much as equivalent gains feel good. In markets, that asymmetry becomes “sell after losses to stop the pain”, precisely when the long-term action is to hold or buy. This is the same Kahneman-Tversky machinery I wrote about in Why Saving Is Hard, pointed at a different target. There, present bias made you spend.

Here, loss aversion makes you sell, and not only after a loss: the same machinery fires preemptively, in the urge to “get ahead of” a downturn before it arrives. Legendary portfolio manager Peter Lynch put the cost of that instinct bluntly in a September 1995 interview:

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

Myopic loss aversion, the term Shlomo Benartzi and Richard Thaler coined in their 1995 paper on the equity premium puzzle, adds a nasty twist: the more frequently you evaluate your portfolio, the more salient short-term losses become, and the less willing you become to hold “risky” assets, even when the long-term payoff is attractive. Thaler, Tversky, Kahneman and Schwartz then confirmed it experimentally: subjects who received the most frequent feedback on their returns took the least risk and earned the least money. Checking your portfolio more often makes you a worse investor. The information is the same; the emotional exposure changes. Berkshire Hathaway chairman Warren Buffett has a line for exactly this temptation:

“Games are won by players who focus on the playing field - not by those whose eyes are glued to the scoreboard.”

Then there’s overconfidence. In the landmark study of individual investor behavior, Brad Barber and Terrance Odean examined 66,465 households at a large discount broker from 1991 to 1996 and found that higher trading activity was associated with worse performance - the most active traders earned 11.4% annually while the market returned 17.9%, a gap that isn’t subtle. The authors summed it up in their paper’s blunt title, Trading Is Hazardous to Your Wealth. The average household in the sample turned over 75% of its portfolio every year - activity with all the associated costs and none of the rewards.

The disposition effect rounds out the set: investors systematically sell winners too early (to lock in the good feeling) and cling to losers too long (to avoid making the loss “real”). Hersh Shefrin and Meir Statman named the pattern in 1985, and Odean later confirmed it in the trading records of 10,000 brokerage accounts: investors were 1.5 times more likely to realize a gain than a loss - and the winners they sold went on to outperform the losers they kept. It is loss aversion expressed as portfolio management, and it shows up in dataset after dataset. The practitioner’s version is blunter and more memorable; in his 1989 One Up on Wall Street bestseller, Lynch wrote:

“Selling your winners and holding your losers is like cutting the flowers and watering the weeds.”

My Brain Wasn’t Built for This Either

I’m not writing about these biases from the outside. My clearest failure is Evolution AB (EVO.ST): across three quarters my own thesis-check articles documented the business deterioration and I held anyway, losing confidence more slowly than the business was losing its case, until I exited in February 2026 at a -25.8% internal rate of return (IRR). At no single moment did the loss feel “real” enough to force the decision. That is the disposition effect operating inside a written thesis, signpost-driven process, which is exactly why I don’t trust willpower alone.

Overconfidence has a name in my ledger too: PDD Holdings (PDD 0.00%↑), a position I built to a tenth of my portfolio on what I later admitted was a country-level thesis rather than company-level conviction. The overconfidence was at the entry - sizing that much opacity that large. The exit was the trade working as it should: I trimmed the position in October 2025 and sold out in November 2025 at $132/share at a +27% gain, before the market priced in the risks I could no longer underwrite. Since then, revenue growth has collapsed to a 9.9% CAGR from 65.8% over the prior five years, operating income and operating cash flow have gone backwards (-2% and -7.3% CAGR), and the stock trades at $84.60/share today. The capital went into higher-conviction businesses whose fundamentals have improved substantially since. The lesson isn’t the exit; it’s never sizing a thesis I can’t fully underwrite at a tenth of the portfolio again.

None of these are character flaws. They are predictable outputs of wiring that was optimized for short-term survival, dropped into an environment that rewards the opposite.

To be fair to my own ledger, it has an opposite column too. In March 2020 I added during the COVID-19 crash rather than selling. In March-April 2025 I was buying Amazon (AMZN 0.00%↑), Alphabet (GOOGL 0.00%↑), Brookfield (BN 0.00%↑) and MercadoLibre (MELI 0.00%↑) aggressively into the tariff sell-off - my top three holdings went from 51% to 59% of the portfolio while the index was down nearly 19%.

With the proceeds from the trim of PDD, I initiated a position in Constellation Software (CSU.TO) in October 2025 in the deepest drawdown of the stock’s history, and I have been adding to MercadoLibre through a 40% drawdown over the past year. I don’t list these as evidence of superior temperament, because the honest reading is less flattering and more useful: buying discipline is the part of my process with the most structure - written theses, valuation triggers, signposts that say what a “gift” looks like - so when the stress arrived, the plan did the deciding. The disposition effect won where no signpost forced a sale (EVO.ST). The biases didn’t disappear; they migrated to the part of the process with the least structure.

Guardrail: Reduce decision frequency. If your strategy is long-term, your feedback loop should be long-term. Limit how often you check the portfolio, pre-commit to rules for adding and rebalancing, and treat every trade as a last resort rather than a hobby. You cannot delete the wiring; you can starve it of opportunities to act.

Diversification Is Simple, Not Easy

Modern portfolio theory, going back to Harry Markowitz’s 1952 paper Portfolio Selection, the work that later earned him a Nobel, formalized a basic truth: diversification reduces risk without requiring you to forecast anything. It is the closest thing investing has to a free lunch. Yet investors routinely end up concentrated, usually without having decided to be.

The most common driver is home bias: the tendency to overweight your own country’s assets even when global diversification is a click away. Kenneth French and James Poterba documented it in 1991: at the time, Japanese investors held over 98% of their equity portfolios domestically, Americans 94%, and Britons 82% - allocations that only made sense if each group expected its home market to beat everyone else’s by several points a year. They can’t all be right, and the pattern persists across markets and decades. Coval and Moskowitz later showed it operates even within countries: U.S. fund managers overweight firms headquartered near their own offices. It feels safe - “I know these companies, I understand my country”, but the feeling is the trap. If your job, your home, and your portfolio all depend on the same local economy, you haven’t diversified anything. You’ve tripled down on one bet and labeled it prudence.

The same applies, with less drama, to employer stock, to whatever sector you work in, and to whatever did well last year, which is just home bias in time rather than space.

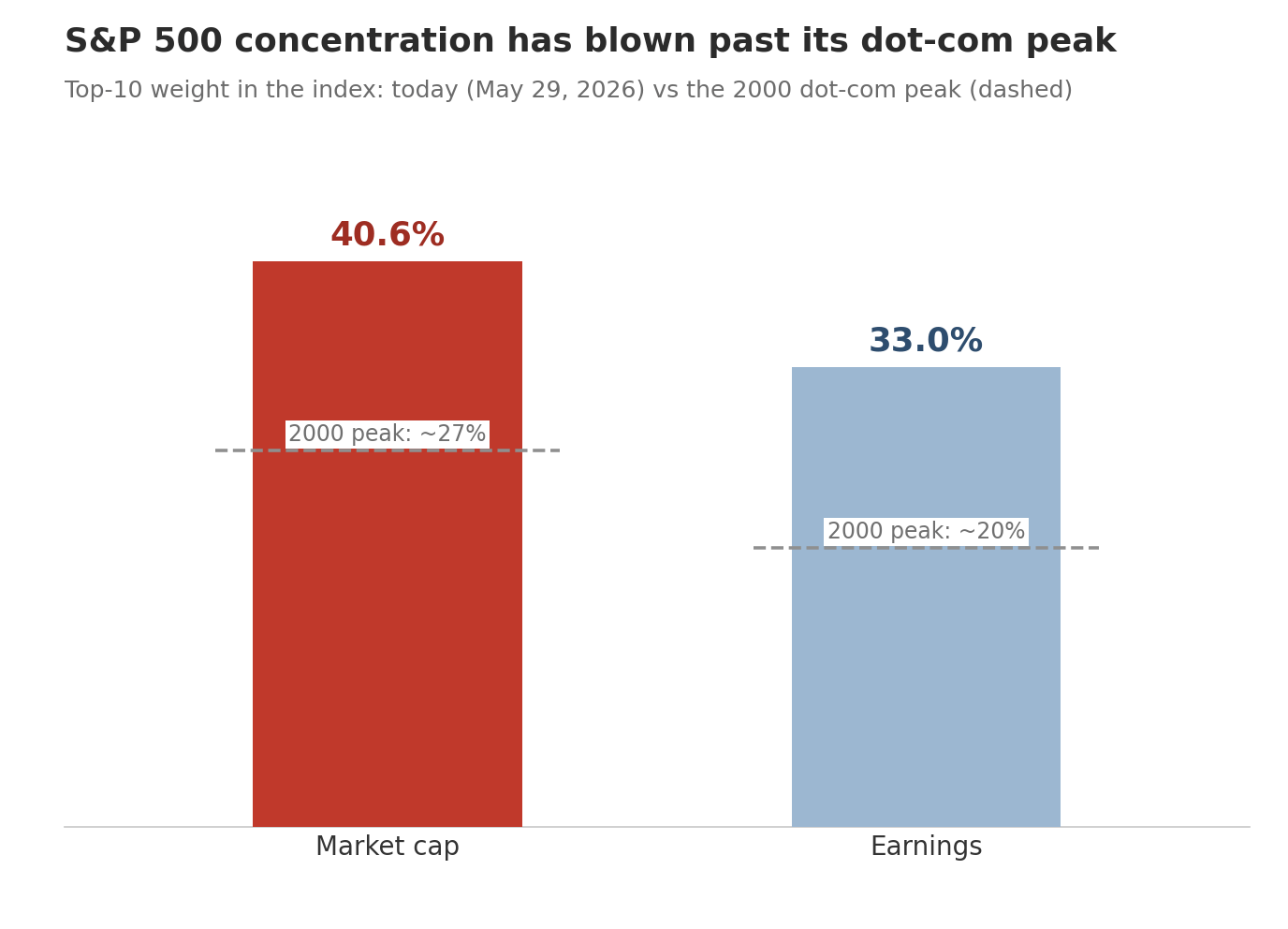

Lately, concentration arrives through the index itself. As of May 29, 2026, the ten largest companies account for 40.6% of the S&P 500’s market capitalization - well above the 27% peak reached at the height of the dot-com bubble - while contributing a smaller 33% of the index’s trailing earnings (per J.P. Morgan Asset Management’s Guide to the Markets).

The Magnificent 7 alone drove 63% of the index return in 2023, 55% in 2024, 46% in 2025, and 29% in Q1 2026. None of this makes an S&P 500 fund a bad instrument. It means the label “diversified” is doing less work than it used to: a U.S. index fund today carries a larger top-ten bet than at any point in its history, and its buyer should know that’s what they own.

Guardrail: Use globally diversified funds as the default. If you choose to overweight your home market, or anything else, do it consciously, write down why, and cap it.

The Industry Sells Activity

If the previous sections describe the headwinds nature built, this one is about the headwinds we built on purpose.

Many investing platforms are engineered to encourage engagement, not calm execution. Regulators have started naming the problem. In 2021, the SEC requested public comment on digital engagement practices1 - behavioral prompts, differential marketing, and game-like features - because they are designed to influence retail investor behavior. The report flagged gamification as glorifying risky trading. The UK’s FCA went further and ran the experiment in June 2024: in a trial with over 9,000 consumers, gamification-style features increased both trading frequency and risk-taking, with the strongest effects on participants with low financial literacy, women, and 18 to 34 year-olds. The pattern rhymes with what I described in Culture of Consumerism: the environment has a business model, and the business model is your activity. A brokerage that profits from order flow has the same relationship to your patience that a social media feed has to your attention.

Nobody at these businesses needs you to lose money. They need you to do things. The losing happens on its own, via every mechanism in these two articles. The irony is that the opposite behavior is where the returns live, as Buffett’s longtime partner Charlie Munger put it:

“The big money is not in the buying and the selling, but in the waiting.”

Guardrail: If your strategy is long-term, don’t use tools optimized for short-term engagement. Turn off notifications, hide the watchlists and “most traded” feeds, and avoid platforms that make trading feel like a game. Quiet environments are an asset class of their own.

Investing Without the Basics

Finally, investing is hard because many people attempt it without the foundations.

The “Big Three” financial literacy questions - compounding, inflation, and diversification, developed by Annamaria Lusardi and Olivia Mitchell - have been used in research across dozens of countries, and performance on them strongly predicts planning and saving behavior. The results are consistently sobering. In the sixth wave of FINRA’s National Financial Capability Study (25,500+ U.S. adults, fielded 2024), only 27% answered at least five of seven financial knowledge questions correctly, and the share clearing the core-question bar has fallen from 42% in 2009 to 32%, where it has sat since 2021. I covered Italy’s even weaker figures in Why Saving Is Hard.

If you don’t understand compounding, inflation, and diversification, you are not choosing a portfolio. You’re guessing, and the market charges tuition for guessing, with no cap on the bill.

Guardrail: Don’t learn by trading; the lessons are real but the tuition is brutal. Learn the basics once, then automate a simple, diversified plan that doesn’t require ongoing brilliance to work.

The Predictable Ways Investors Lose

Put the two parts together and a pattern emerges. Most long-run investing failure isn’t a lack of access to good products - the products have never been better or cheaper. It’s predictable leakage:

Volatility triggers selling.

Frequent checking amplifies loss aversion.

Overconfidence drives over-trading.

The disposition effect sells winners and rides losers.

Overestimating your edge - your own, or the active manager you hire - loses to the index.

Hidden concentration (home bias, employer stock, a top-heavy index) undoes diversification.

Fees compound against you.

Platforms nudge you toward activity.

Skipping the basics turns investing into guessing.

Leverage turns temporary mistakes into permanent ones.

Different mechanisms, one pattern: in almost every case the move that feels natural - selling the dip, checking the screen, trading on a hunch, hiring the active manager, staying close to home - is the one that costs you. None of this requires a bad market or bad luck. In a crash the damage is at least visible: you see the loss, and the shock can correct you. A bull market is more dangerous, because every one of these leaks operates silently inside rising prices - your account goes up, so nothing feels wrong. The cost never arrives as a loss you can point to; it arrives as the gap between what you earned and what you would have earned by buying a low-cost index and leaving it alone. Opportunity cost doesn’t sting like a realized loss, so nothing forces you to stop, and by the time the underperformance is undeniable, measured in years rather than days, the compounding you gave up is already spent.

Where I Stand: Defensive by Default, Enterprising by Choice

Readers who follow my newsletter will notice a tension. Everything above points toward broad, low-cost, automatic diversification - and I run a concentrated portfolio of six to ten businesses, with my largest position around a quarter of the total. That concentration was a deliberate move: in 2024 I transformed the portfolio, selling my remaining funds to back individual high-conviction businesses instead.

Graham’s distinction between the defensive and the enterprising investor is the honest way to frame it. The defensive investor wants average results with minimal effort and emotion: index funds, automation, low cost, no forecasts. The enterprising investor treats investing as a serious, ongoing endeavor - research, valuation work, written theses - in exchange for the possibility of better results. Graham’s point is that these are both legitimate paths, with the worst position being in the middle: defensive effort with enterprising risk.

For nearly everyone, the defensive path is the right one, not as a consolation prize, but because it converts the guardrail in these articles into a default setting. That is the advice I give friends and family, and I gave it in my beginner’s presentation in October 2024.

I chose the enterprising path with open eyes, and I am conscious about what that means. The SPIVA statistics apply to us all; concentration removes the diversification guardrail entirely, which means every other guardrail has to carry more load. I keep the guardrails deliberately heavy: no leverage, small turnover, decisions tied to business fundamentals rather than stock prices’ fluctuations, a written thesis per holding with explicit “what would change my mind” conditions, and a feedback loop measured in 5+ years against my benchmark (MSCI All Country World Index, ACWI 0.00%↑), not in trading days. When the March-April 2025 tariff sell-off hit, the system’s job was to make adding to my highest-conviction names mechanical rather than heroic. That time, it held.

Because that portfolio transformation happened in 2024, the honest comparison runs from there: I beat my benchmark in 2024 by +3.11% on a FX-neutral basis and I trailed it in 2025 by -4.03%. That’s what this path actually looks like - not a steady stream of validation, but a multi-year bet that must be re-earned. If I stop clearing the bar over a full cycle, the defensive path will still be there, and taking it would be a result.

Final Thoughts

If you accept these forces, the goal stops being “pick the perfect investment” and becomes something less glamorous and far more achievable: build a system that makes good investing behavior the default.

Make diversification automatic, so you don’t need forecasts. Make costs minimal, so compounding works for you rather than against you. Make activity rare, so you don’t pay the behavioral tax of over-trading. Make your environment quieter, so nudges and comparison don’t hijack a plan your calmer self already made.

This closes the arc that started with lifestyle inflation: build slack, defend it from your own psychology, and then deploy it without flinching. Each step is hard for the same underlying reason - the right move feels wrong in the moment, and the wrong move feels productive. In a 1994 talk, Lynch reduced all of it to one organ:

“I’ve always said, the key organ in the stock market isn’t the brain, it’s the stomach.”

Investing is hard because it rewards patience and punishes flinching. The people who do best aren’t necessarily the smartest - they’re the ones who designed their process so the daily fight with themselves never gets scheduled.

Digital engagement practices (DEPs) is the SEC’s term for design features - notifications, streaks, leaderboards, and other game-like or behavioral prompts - that nudge retail investors toward more frequent trading.