Evolution AB's Q4 2025 Results: Flat Live Revenue, Contracting Leverage, and Why I Exited

Europe’s channelization is slipping, Asia cybercrime issue has no timeline, and growth is shifting to lower-leverage regions

Back in Q1 2025, I described Evolution’s slowdown as potentially temporary, and I flagged three fault lines that had to heal for the growth story to hold: cybersecurity in Asia, proactive ring-fencing in Europe (especially in low-channelization markets), and rising compliance/expansion costs that could pressure operating leverage if revenue didn’t re-accelerate.

By Q3 2025, my stance had shifted: those same issues were starting to look structural. Europe’s ring-fencing was becoming a lasting headwind, Asia’s counter-piracy measures were proving hard to stabilize without collateral damage to legitimate demand, and operating leverage had flipped from a tailwind to a constraint.

The Q4 2025 year-end report reinforced that framework. Europe is now constrained by declining channelization (players pushed to unlicensed operators Evolution won’t serve), Asia remains “slow and methodical” with no timeline, and incremental growth is shifting to regions with lower operating leverage. That combination reduced my confidence in a durable re-acceleration, so I exited after Q4.

What Q4 2025 Results Said

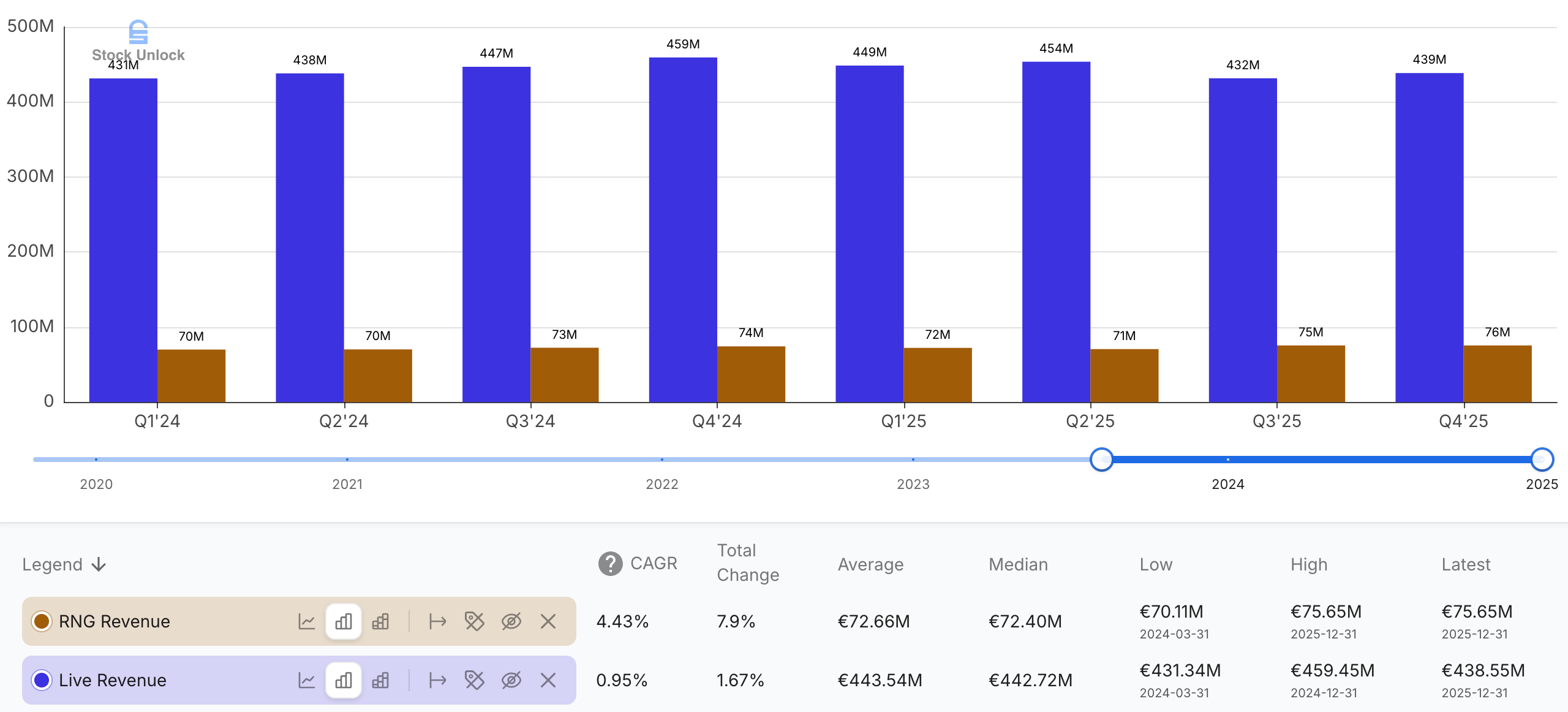

Evolution reported Q4 net revenues of €514.2 million (-3.7% YoY, +1.4% QoQ). Live Casino remains the engine: €438.6 million (85.3% of revenue) versus RNG at €75.7 million (14.7%). Live has effectively plateaued since early 2024 (€430-€460 million per quarter), while RNG has grown modestly (€70-€76m). The mix matters: without renewed Live growth, the consolidated top line struggles to compound.

Live revenue contracted 4.3% YoY in Q4.

From a cash perspective, operating cash flow (OCF) was €296.6 million in Q4 (-10% YoY), and management highlighted “Operating Cash Flow after Investments”1 of €258.2 million.

For 2025, total operating revenue was €2,119 million (-4.3% YoY). OCF was €1.25 billion (-3.5% YoY); less €134.8 million of CapEx implies €1.12 billion of free cash flow. The tension is clear: the company is still executing, but the revenue engine isn’t responding like it used to. As the year-end report puts it, “overall, we are proud but not happy with 2025”.

Demand Is Maturing

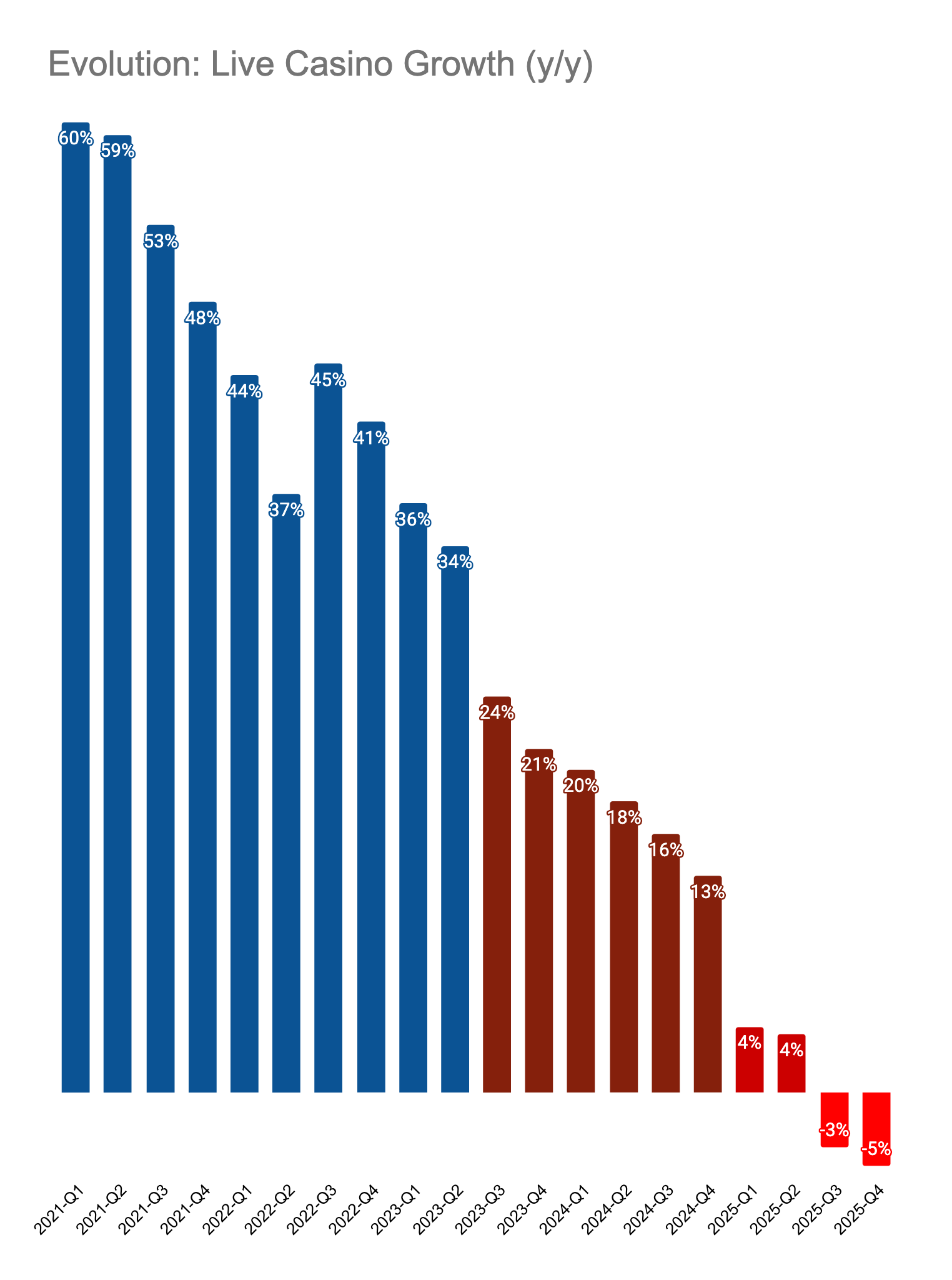

From 2006 through 2023, Evolution benefited from two forces: strong execution and a steadily expanding global audience for online casino. The last two years suggest the second force is weakening. Live revenue has largely stalled, which increasingly looks like market maturation rather than a passing hiccup.

By 2023, most of the addressable audience outside China had already encountered online casino - often through offshore sites with fewer friction points, amplified by aggressive post-COVID marketing. Since only a fraction of people are naturally interested in casino-style gambling, incremental net-new user growth may simply be harder to find. Meanwhile, the remaining “clean” growth pockets are less accessible for a large, regulated supplier without raising compliance and reputational risk, and newer gambling formats (prediction markets, crypto-native schemes) are competing for share.

That leaves a business that can still be best-in-class, but with fewer easy growth paths and a risk profile that matters more when the upside is no longer expanding.

Where Q4 Hits My Q3 Thesis

In Q3, I argued the key question was no longer “will the headwinds fade?” but “is this the new operating baseline?” Q4 pushes the answer toward the latter.

Europe

Ring-fencing is no longer the whole story; channelization is. Management framed Europe’s weakness as regulation pushing players from licensed operators toward unlicensed ones Evolution won’t serve. CEO Martin Carlesund: “players are pushed out of the regulatory remit”, with the addressable market dropping “to 50% level in certain countries”.

That’s the same dynamic I flagged in Q1 - ring-fencing bites hardest where channelization is already low. Q4 makes it look less like a short-term adjustment and more like a structural shrink in the regulated pool.

Asia

Q4 was better than Q3, but not fixed. Management still describes progress as “slow, methodical”, and Carlesund reiterated they “don’t know exactly when that will happen”. In Q1, the message was “great potential” once Evolution “come[s] to terms with […] cyber criminality”; by Q4 the timeline remains open-ended, which is why I no longer underwrite a clean rebound.

It’s also plausible that piracy isn’t the only headwind - maturity may be part of the story. Either way, Asia snapping back to old growth no longer feels like a base case.

Margins / Operating Leverage

Management reiterated margins “in line with 2025 meaning 66%” for 2026. For me, the key is operating leverage.

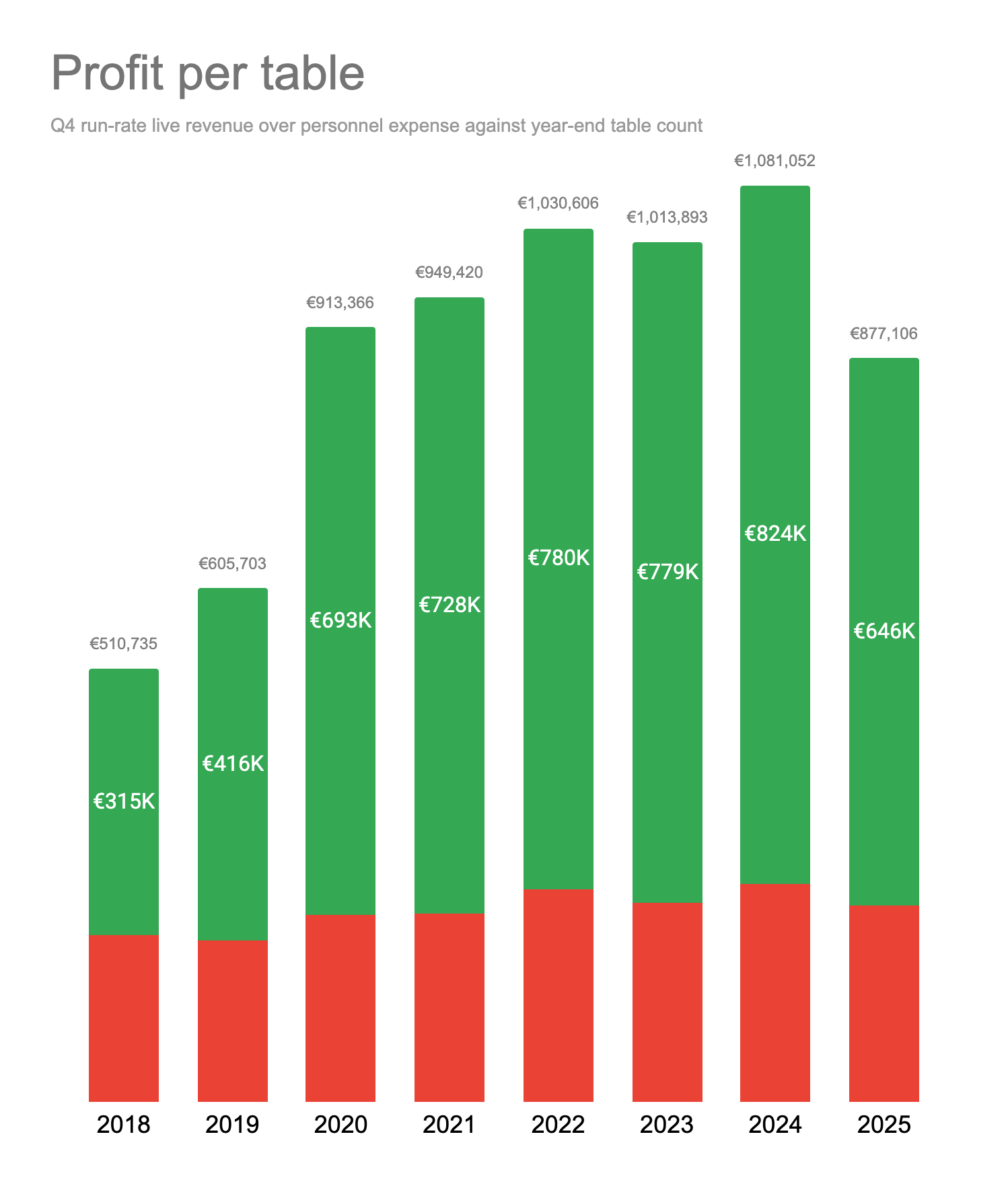

Profit per table fell to €877k in 2025 (from €1.08 million in 2024). Evolution’s Live model is personnel- and capacity-heavy, so costs are sticky once studios/tables are deployed. In a growth regime, that structure creates strong drop-through; in a flat regime, unit economics compress. The profit-per-table decline is the unit-economics proof.

Management effectively acknowledged this in Q&A: higher volume would have meant “higher volume on the same capacity”. Without renewed Live momentum, operating leverage isn’t working in shareholders’ favor.

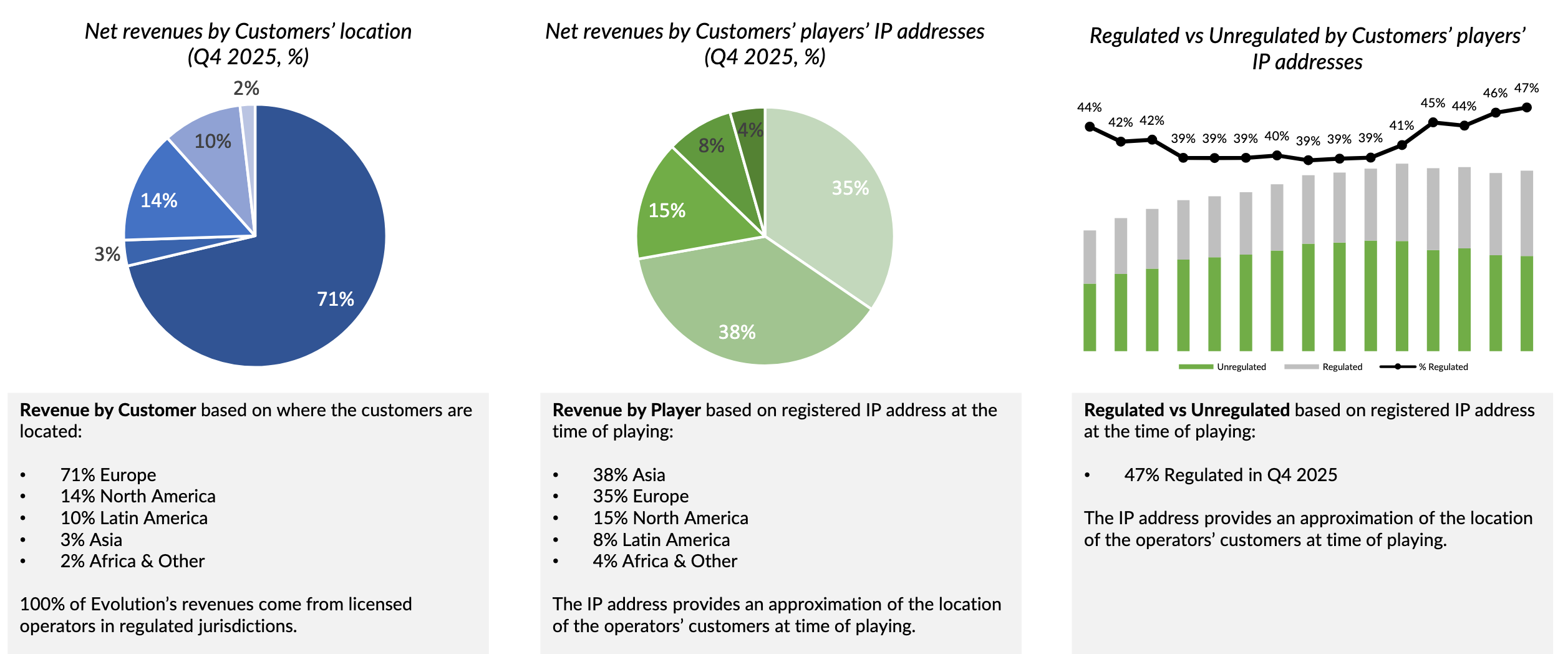

The New Disclosure: Customer vs Player IP

The customer-location view is Europe-heavy (71% Europe), but the player-IP view shows Asia and Europe as the two largest demand pools (38% and 35%).

It’s worth reconciling Evolution’s “regulated” language with this disclosure. Evolution only supplies licensed operators, so in a B2B sense “all revenue is regulated”. Yet, the player-IP estimate implies only 47% of end-player activity was in regulated markets in Q4 2025 - highlighting how much underlying demand sits outside well-functioning regulated channels. That is where ring-fencing and declining channelization bite. Evolution’s compliance stance turns market leakage into lost addressable demand.

“New World vs Old World” Framing

Ali Gündüz’s write-up frames Evolution’s reality as bifurcating: “older markets in Asia and Europe face stagnation and even decline”, while the Americas and Africa provide needed growth. The part that matters for me is not just growth rates, but the economic model.

The “Old World” (Europe and Asia) benefited from scale and operating leverage: serving many markets from a few central studios. Meanwhile, major “New World” (North America, LatAm and Africa) markets require local studios (U.S. state-by-state; Brazil language/localization), structurally limiting leverage. Europe and Asia are still the majority of end-demand (73% combined in the player-IP split). The Americas and Africa could grow fast, but from a smaller base they need to grow exceptionally quickly just to offset stagnation in the “Old World”.

Evolution’s own year-end report contains the strategic breadcrumb that aligns with this: “Our primary focus will be on the USA, Latin America”.

Even if the Americas grow, the question becomes whether they can offset “Old World” declines and do so with comparable margins and cash generation. Ali’s conclusion is that this is “difficult to imagine”. I agree.

Profitability and Capital Allocation: Good, But Not Thesis-Saving

Earnings per share (EPS) came in at €5.23 (-11.46% YoY). Net income-to-OCF cash conversion remained solid at 1x, and the balance sheet stayed strong (cash €818 million at year-end) with a debt ratio of 0.26x. Buybacks continued (€500.2 million in 2025) and so did dividends (€572.5 million in 2025).

Strong cash generation is no longer sufficient if the question is durability. In my Q3 article, I said the company was “managing for stability rather than market share gains”. Q4 did not change that characterization.

Ali adds another nuance worth keeping in mind: €200 million of “ghost taxes” from Pillar Two creating a gap between reported tax expense and cash taxes, with uncertainty on timing/settlement.

Why I Exited After Q4

What changed since Q1 isn’t that new risks emerged - it’s that the “temporary” label stopped fitting. I was willing to treat Asia mitigation and Europe ring-fencing as short-term measures that would strengthen the foundation; by year-end, both remained unresolved, and the economics reflected it.

Q4 reinforced the opposite of what the re-acceleration thesis required: Europe is framed as a channelization problem (“regulated markets are losing ground”), Asia remains “slow, methodical” with no timeline, and incremental growth is shifting to lower-leverage regions. Add unresolved distractions (ongoing Playtech litigation, rising headcount, and a weaker H2 Game Round Index due to Europe/Asia measures), and the setup depends too much on external stability.

The most telling line in Q&A was what it would take for operational progress to match financial results: “just a stable environment […] No more, no less”. If re-acceleration depends primarily on external stability rather than controllable execution, I don’t see an asymmetric risk/reward anymore.

Final Thoughts

Evolution remains a quality operator with a strong balance sheet and meaningful capital returns. Q4 reinforced the new baseline: Europe is constrained by channelization decline, Asia has no clear timeline beyond “slow, methodical” progress, and growth is shifting to lower-leverage regions that can’t easily offset weakness in Europe/Asia. If re-acceleration depends mainly on “a stable environment”, the risk/reward is no longer asymmetric. That’s why I exited after Q4 at a -25.8% internal rate of return (IRR).

Evolution AB defines “Operating Cash Flow after Investments” as OCF less CapEx, excluding M&A and financial investments, a proxy for free cash flow (FCF).