Why Investing Is Hard, Part 1: The Price of Admission

Why even a rational investor would struggle: a 14% average drawdown, a 93% twenty-year failure rate for professional investors, guaranteed costs, and unforgiving leverage

Investing is hard before you even make your first mistake. The game is built that way: returns come bundled with drawdowns you must sit through, competitive markets price in news faster than you can act on it, costs are guaranteed while returns are not, and leverage converts temporary errors into permanent ones. The scoreboard is unambiguous - the large majority of professional managers lose to their benchmark in every market SPIVA tracks, so humility is the rational starting point. This is the easy half of the problem. The hard half is the player, which is Part 2 of this series.

In January I wrote Why Saving Is Hard: The Psychology of Spending, and the answer came down to wiring: spending is vivid and now, while the benefits of saving are abstract and later. Investing is the same problem turned up a notch. The rewards are not just delayed, they are probabilistic, and the path to them is emotionally punishing. Markets will routinely make you feel wrong before they make you right.

This article closes the loop on the series. Slack is what’s left after fixed costs. Saving is the discipline of building it. Investing is the discipline of deploying it without sabotaging yourself. This first part is about the game itself - the four structural forces that make investing hard for everyone. Part 2 is about the player: the wiring that makes it harder still, and the guardrails that actually hold.

Volatility Is the Price of Admission

Investing is hard because the outcome is uncertain and the path is unpleasant. Those are two different problems, and the second one breaks more investors than the first.

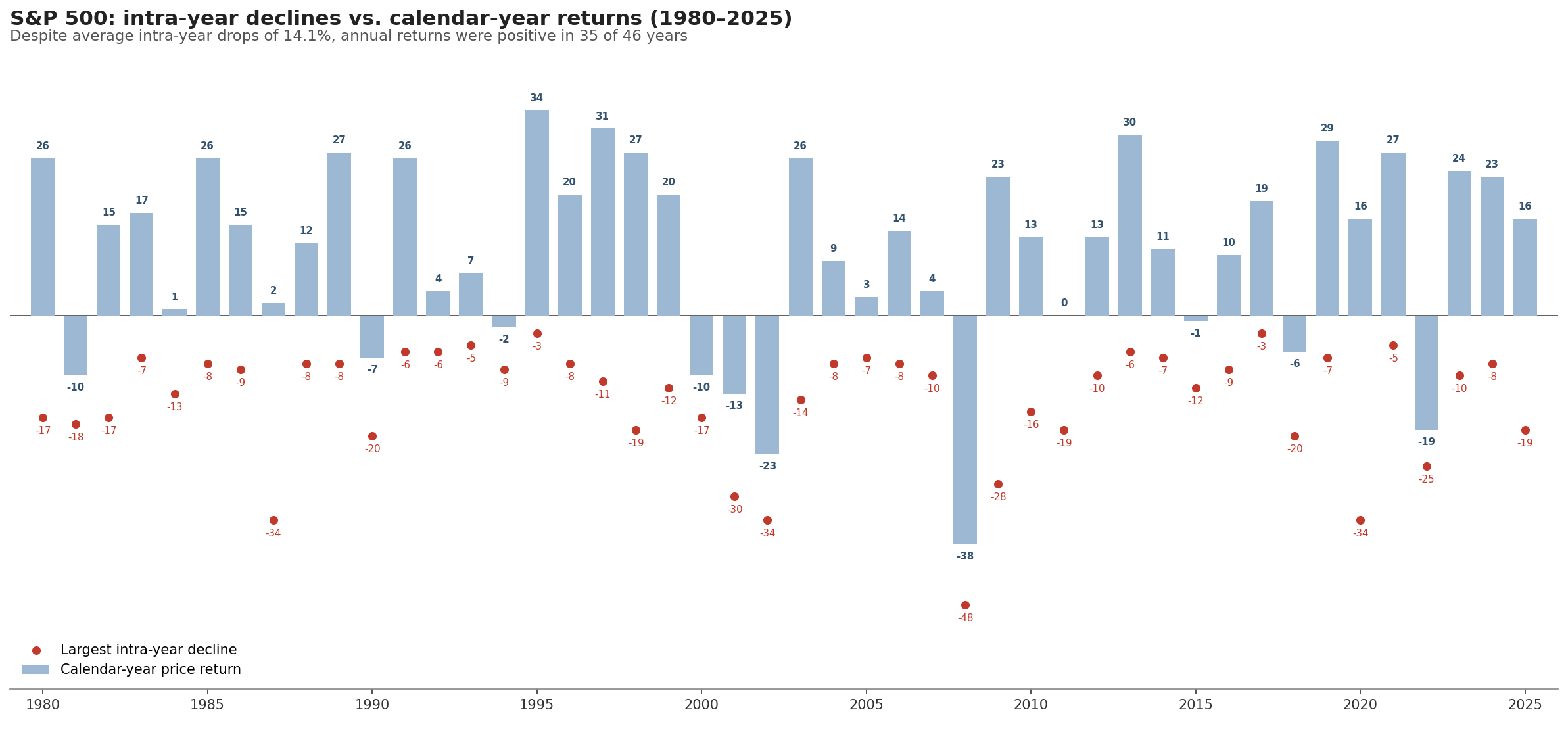

Even in “normal” years, markets drop meaningfully before they recover. Since 1980, the S&P 500’s average intra-year peak-to-trough pullback1 has been 14.1% - yet annual returns were positive in 35 of those 46 years (per J.P. Morgan Asset Management’s Guide to the Markets). The chart below shows each year’s largest decline against where the year actually finished. The implication is uncomfortable but clean: if you can’t emotionally tolerate drawdowns, you can’t reliably earn equity-like returns. There is no version of the equity premium that comes without the stomach ache.

Trying to time your way around the unpleasant parts is harder than it looks, because the best and worst days tend to cluster in the same turbulent stretches. Missing a small number of the market’s best days dramatically reduces long-term returns, and those days have a habit of arriving right after the worst ones, when a recently-burned investor is least likely to be holding. That’s why “getting out and back in” is such a dangerous game: it requires two correct decisions, made under maximum stress, in opposite emotional directions.

I covered the temperament side of this in Volatility Isn’t Risk. My conclusion hasn’t changed: volatility is not the risk. Reacting to it is.

Guardrail: Treat volatility as the fee you pay for long-term growth, not a bill you can negotiate. Decide your risk tolerance level, your asset allocation2, in calm conditions, and commit to staying invested through ordinary drawdowns. The decision belongs to your calm self; the execution is just refusing to overrule it.

Beating the Market Is a High Bar

The second reason investing is hard: you are competing in a market designed to be hard to beat.

The Efficient Market Hypothesis3 - formalized by Eugene Fama in his 1970 review of the theory and evidence - doesn’t claim prices are always right; they obviously aren’t, or there would be no manias and no panics. What it formalizes is a useful baseline: in competitive markets, publicly available information gets reflected in prices quickly, which makes consistent outperformance difficult. Whatever you just read in the news is, with high probability, already in the price by the time you act on it.

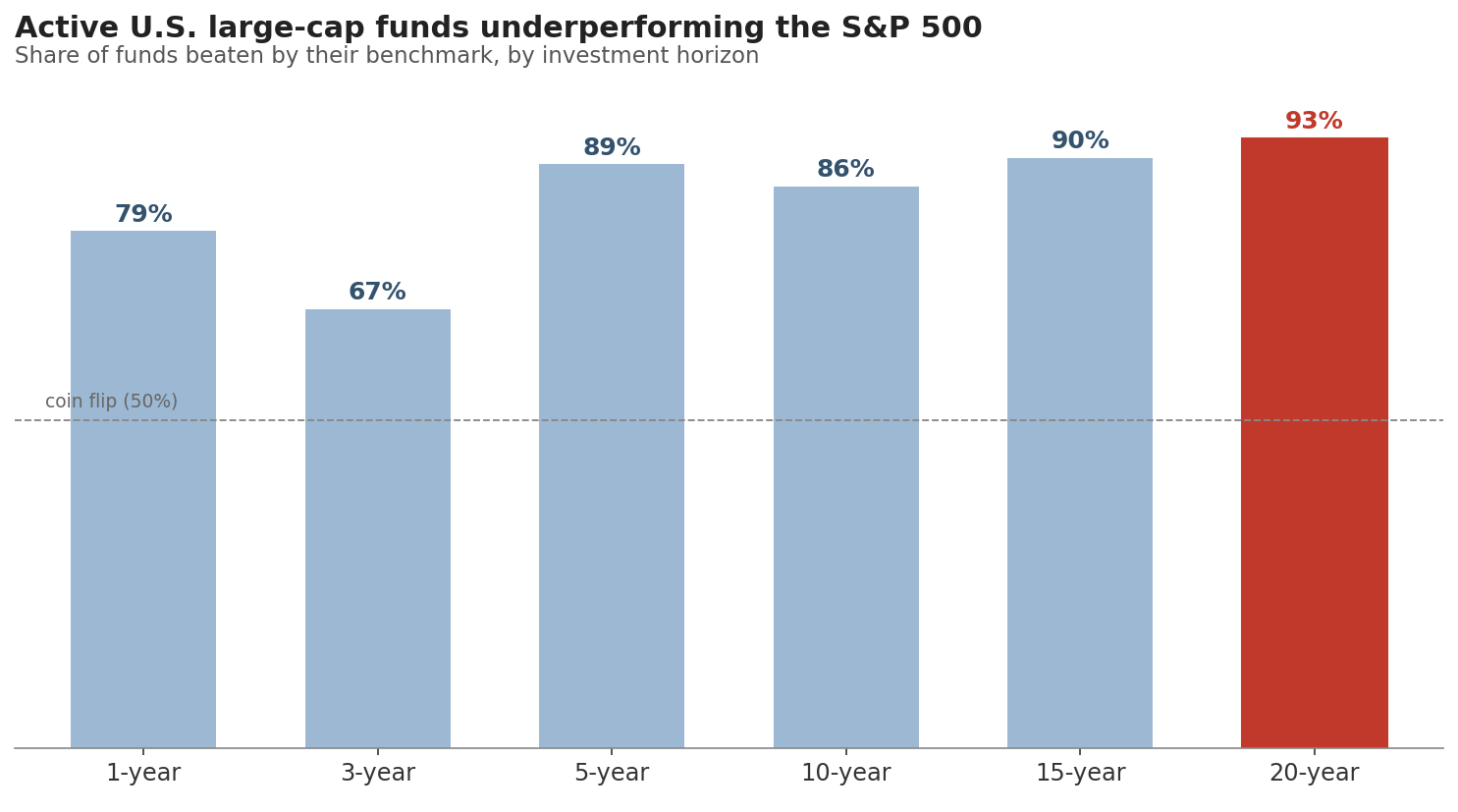

The real-world scoreboard backs the theory. In the latest SPIVA4 U.S. Scorecard (Year-End 2025), 78.8% of actively managed U.S. large-cap funds underperformed the S&P 500 over one year, and the longer the horizon, the worse the numbers get: 89% fell short over five years, 85.6% over ten years, 90% over fifteen, and 92.9% over twenty.

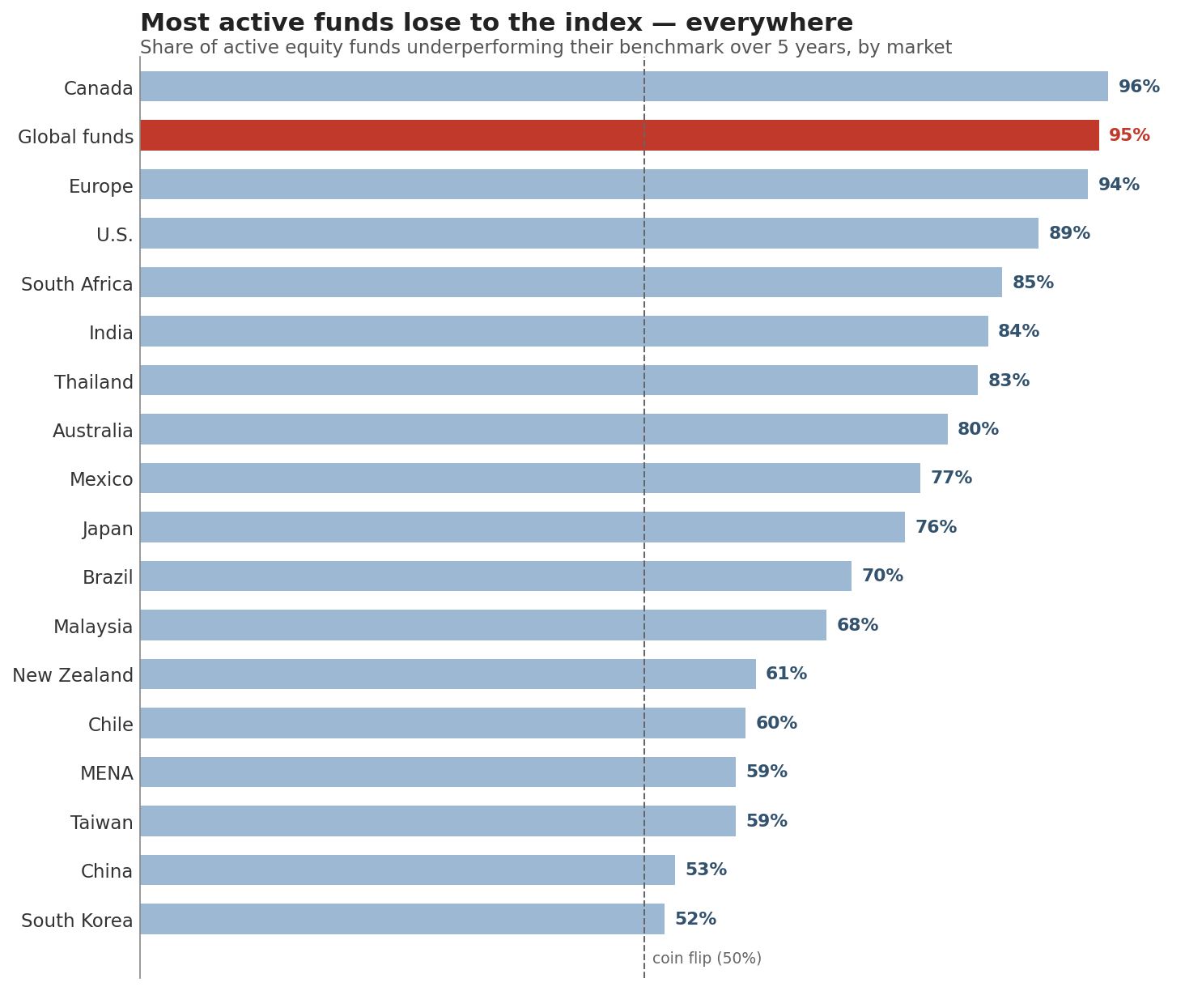

This is not an American phenomenon. SPIVA runs the same scoreboard across markets worldwide, and over the five years through December 2025 a majority of active equity funds lost to their benchmark in every single one of the 18 markets tracked: 95.9% in Canada, 93.9% in Europe, 84% in India, 76% in Japan, and even in the supposedly less efficient markets, where stock pickers are said to have an edge, the failure rate never dropped below half. Longer horizons are harsher still: over ten years, 97% of European funds and 98.8% of Canadian funds trailed their index. These are professionals with research teams, data terminals, and direct access to management. If barely one in fourteen U.S. managers clears the bar over two decades, and no market anywhere gives a majority of them a passing grade over five years, the default assumption for any individual investor should be humility.

Guardrail: Default to broad, low-cost diversification unless you have a clear, testable edge, and the temperament to stick with it through years of underperformance. Note that the second condition is the harder one. I’ll come back to where I personally land on this in Part 2, because I am not a neutral party here.

Small Drags Compound Quietly

Investing is hard because the costs are guaranteed and the returns are not.

Fund fees (expense ratios5), trading spreads6, account and platform charges, advisory fees, and tax inefficiency are not abstractions - they are the one part of your future return you can know in advance, and they compound with the same relentlessness as gains, just in the wrong direction. The SEC’s investor bulletin on fees and expenses makes the point with one worked example: on a $100,000 portfolio growing 4% a year for 20 years, a 1% annual fee leaves you nearly $30,000 poorer than a 0.25% fee - on the same gross returns. A drag that looks trivial in any single year becomes a meaningful slice of terminal wealth over twenty.

There’s a behavioral angle too: most friction is self-inflicted, because activity is what generates it. Every trade carries spreads, possible taxes, and the chance of error. A trade feels like you’re doing your job as an investor, but much of the time it’s simply converting your time into costs.

Guardrail: Make all-in cost a primary metric. Prefer low-cost, tax-efficient vehicles, minimize turnover, and treat every extra trade as a hurdle the idea must clear: it isn’t enough to be right, you have to be right by more than the friction.

Leverage Changes the Rules of Survival

Everything above makes investing hard. Leverage makes it fragile, and those are different things.

Margin7 increases your purchasing power, but it also introduces a failure mode that unlevered investors simply don’t have: forced selling. A margin call8 liquidates you at the worst possible moment because the worst moment is exactly when the call arrives. The SEC’s bulletin on margin accounts spells out the mechanics most investors miss: your broker can sell your securities to meet a call without notifying you first, and it chooses what to sell. An unlevered investor who is wrong loses money. A levered investor who is temporarily wrong can lose everything, and temporarily wrong is the normal state of even excellent investments. It’s also a dangerous match for the wiring mentioned in the intro (and discussed at length in Part 2): an SEC economic staff paper, The Financial Illiteracy and Overconfidence of Margin Traders, found that margin traders score lower on financial literacy than non-margin traders - only 15% could answer a basic question about margin itself, versus 31% of investors who don’t use it - while rating their own investment knowledge higher. The worst possible pairing of fuel and spark.

Guardrail: For most long-term investors, the answer is simply no leverage. It is a return-destroyer disguised as sophistication. The whole premise of long-term investing is the ability to be wrong for a while without it becoming permanent; leverage sells that ability for a faster ride.

The Solvable Half of the Problem

Take note of what the game asks of you: sit through a 14% drawdown in an average year without flinching, accept that the information you trade on is probably already in the price, pay only the costs you must, and never let borrowed money turn a temporary mistake into a permanent one. None of it is easy - the SPIVA scoreboard is the record of an entire profession struggling with exactly these forces. This is the half of the problem that is solvable: every one of these bars yields to rules and discipline.

The other half of the problem doesn’t yield to a rulebook, because the obstacle is the person holding the rulebook. In Part 2: the biases the platforms are engineered to exploit - loss aversion, overconfidence, and the disposition effect, including where they show up in my own ledger - and the system that makes good investing behavior the default instead of a daily fight.

A drawdown (or peak-to-trough pullback) is the decline from a market high to its subsequent low, before recovery.

Asset allocation is the split of a portfolio across asset classes (stocks, bonds, cash) - the main lever controlling how violent the ride will be.

The Efficient Market Hypothesis (EMH) holds that asset prices rapidly incorporate publicly available information, making it hard to consistently profit from that information.

SPIVA (S&P Indices Versus Active) is S&P’s recurring scorecard comparing actively managed funds against their benchmark indices.

An expense ratio is the annual percentage a fund deducts to cover its operating costs, charged automatically against your returns whether the fund gains or loses.

A bid-ask spread is the gap between the price you can buy at (the ask) and the price you can sell at (the bid); you cross it on every trade, and it widens in less liquid securities.

Margin is borrowed money used to buy securities.

A margin call forces you to deposit funds or sell holdings when their value falls below a threshold.