Tariffs and the Trade War Sell-off: A Case of Conviction and Disciplined Investing

Echoes of 2008, 2020, and every panic before; history doesn't repeat, but it rhymes

“There is nothing about the price action of a stock that tells you whether you should keep owning it. What tells you whether you should keep owning it is what you expect the company to do in the future.”

— Warren Buffett

One of the most enduring lessons in investing comes from Warren Buffett. It’s a deceptively simple idea, yet in times of heightened volatility, it becomes incredibly difficult to follow. As stock prices swing wildly in reaction to headlines and political noise, many investors lose sight of the underlying businesses. However, it’s precisely in these moments, when fear dominates and stock prices detach from business fundamentals, that level-headed investors must return to this principle: long-term value is driven not by market sentiment, but by what the company will earn and grow into over the next 5, 10, and 20 years.

Few investors have articulated this mindset better than Warren Buffett. In the depths of the 2008 financial crisis, in his article Buy American. I Am, he urged investors to buy U.S. stocks amid widespread fear, revealing that he was shifting his personal portfolio from government bonds into stocks, emphasizing the principle “Be greedy when others are fearful”. While acknowledging he couldn’t predict short-term market moves, Buffett argued that long-term prospects for strong American businesses remained intact. Historically, market rebounds occur before economic recoveries, and cash, though comforting, is a poor long-term asset. His message: ignore short-term fear, focus on value, and invest with a long-term mindset.

Buffett’s focus on long-term fundamentals over short-term noise is crucial, especially when policy shocks hit the stock market. That’s exactly what happened in the first part of 2025, especially on April 2, 2025, when President Donald Trump unveiled sweeping tariffs that upended international trade expectations and sent stock markets into turmoil.

Reciprocal Tariffs, Market Chaos, and Rational Allocation

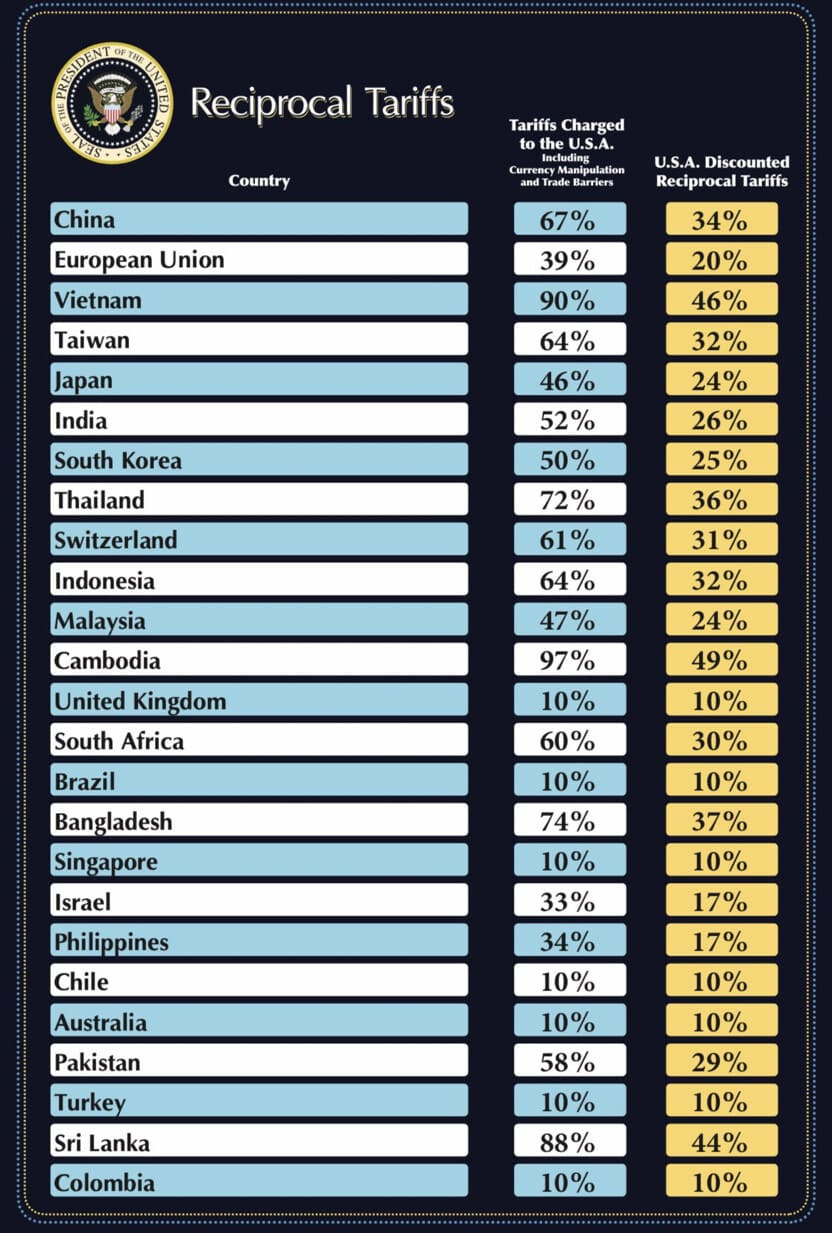

On April 2, 2025, United States’ President Donald Trump unveiled one of the most significant shifts in U.S. international trade policy in recent history, a day he called Liberation Day. He announced a universal tariff of 10% on all goods imported into the U.S., alongside higher “reciprocal tariffs” aimed at more than 60 countries, determined by their respective trade surpluses with the U.S.

China, specifically, was targeted with an additional 34% tariff, stacked upon the already existing 20%. Major trading partners including Japan, and the European Union countries were notably affected by these measures. Canada and Mexico, however, received temporary exemptions from these heightened “reciprocal tariffs”.

These escalating tariff concerns have ignited significant market volatility, causing widespread fear and triggering a notable market correction.

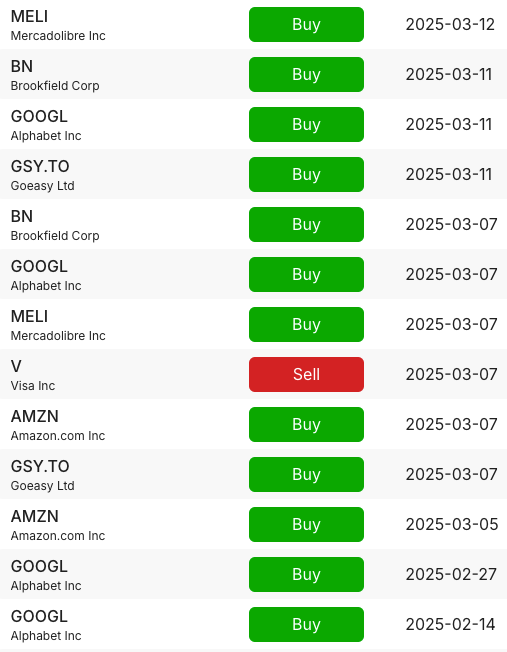

Amid this turbulence, I saw a compelling opportunity and aggressively invested in high-conviction assets like Amazon (AMZN 0.00%↑) and Brookfield (BN 0.00%↑), companies selling at a discount to intrinsic value, whose fundamentals are solid and long-term prospects bright. I covered the year-end 2024 financial disclosures of Amazon and Brookfield, and shared my valuation of both in dedicated posts.

Buying the Dip: Easy in Theory, Hard in Practice

Investors often talk enthusiastically about “buying the dip”, imagining themselves bravely capitalizing on market downturns when everyone else is fearful. While attractive in theory, the reality of buying the dip is more complex psychologically and practically, particularly when the market pullback is substantial.

Buying small dips, say 5%, feels relatively straightforward. These modest declines are common occurrences driven by typical market volatility. They don’t trigger significant uncertainty or anxiety, making it easy to step in confidently. However, substantial market-wide corrections of 15% or more, pose a different psychological challenge entirely. These deeper declines bring heightened uncertainty, leading many investors to fear that stocks might continue dropping even after buying in. The anxiety of potentially “catching a falling knife” often paralyzes investors or leads them to question their strategies entirely.

Timing market bottoms precisely is virtually impossible. Despite countless attempts by economists and market commentators, nobody has consistently and accurately pinpointed when markets hit their absolute lowest.

“Missing the bottom on the way up won’t cost you anything. It’s missing the top on the way down that’s always expensive.”

— Peter Lynch

As Lynch wisely noted, rather than trying to guess market bottoms while sitting on the sidelines with cash, I believe I can benefit far more by focusing on identifying high-quality companies that have become significantly undervalued, and buying them consistently throughout the dip.

During severe market sell-offs, investors frequently abandon their original investment strategies, setting stop losses to crystalize what they deem are acceptable losses and missing the upside when stock prices eventually recover, or shifting from carefully selected individual companies to perceived safer options such as Exchange-Traded Funds (ETFs). While ETFs aren’t inherently problematic, such reactive shifts often reduce exposure precisely when investors should be maintaining, or even increasing, their exposure to discounted, quality assets.

The Discipline to Stay Invested Through the Noise

Every major market downturn feels uniquely threatening, often accompanied by claims that “this time is different”. It’s true, events like the Dot-com bubble, the Great Financial Crisis, COVID-19, and now tariff issues carry their own distinct factors, whether regulatory changes, economic policy shifts, geopolitical tensions, or unprecedented global events. Yet, precisely because each crisis is unique, investors become fearful, leading to panic-selling, dramatic stock price discounts, creating buying opportunities for level-headed investors. If the circumstances causing the broad market sell-off were predictable and familiar, stock prices wouldn’t experience deep discounts in the first place.

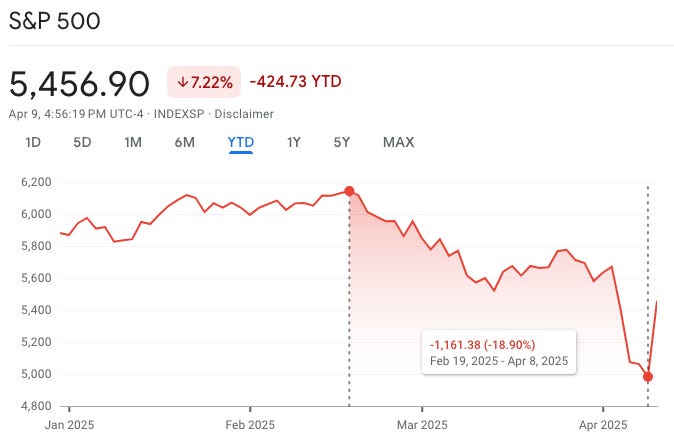

Periods of extreme uncertainty almost always coincide with significant market declines. Many investors, driven by fear rather than logic, often overshoot, discounting stocks excessively compared to actual risks. Just as overconfidence drives stocks to irrationally high valuations, panic and pessimism can cause them to become excessively undervalued. This uncertainty was evident when markets rebounded sharply on April 9, 2025, surging nearly 10% in a single day after a post on social media by President Trump announced a 90-day pause and a significant reduction in the recently announced “reciprocal tariffs” on U.S. imports, later confirmed by an official statement from The White House.

Despite imposing a steep tariff of 125% on China due to ongoing trade tensions, President Trump’s softened stance on other global tariffs significantly boosted market confidence. The U.S. stock market, which had been experiencing a nearly 20% drawdown from February 19, 2025’s peak amidst international trade policy uncertainty, exploded upward within minutes of President Trump’s announcement.

The rapid nature of the move highlighted just how unpredictable short-term market dynamics have become in an era where a single post on social media can cause swings in the stock market of 10% or more. Furthermore, the volatility of the past two months demonstrated vividly how swiftly investor sentiment can shift and why attempting to time the market based on short-term news, political statements and market commentators views is futile: Investors who sold out in fear just days before President Trump’s announcement found themselves scrambling as the stock market rapidly reversed course. Those who waited on the sidelines, hoping to buy lower, instead watched from afar as markets rapidly recovered. I’ve previously explored market fluctuations, psychological responses, and strategies for separating volatility from actual risk in an earlier post.

Ultimately, market noise is transient. Today’s headlines, social media posts, and short-term fears will fade with time. In ten years, we likely won’t even recall the specifics that triggered this volatility. By maintaining a disciplined, fundamental approach, level-headed investors position themselves to benefit from temporary market dislocations rather than fall victim to them.

Markets Move Fast: A Reminder from the COVID-19 Crash

Consider March 2020, during the onset of the COVID-19 pandemic: Investors experienced extreme panic and uncertainty. Businesses shut down globally, supply chains collapsed, and fear dominated headlines. Yet, looking back, we now recognize March 23, 2020, as the very bottom of that market cycle. Despite widespread pessimism and calls for caution from leading experts, investing aggressively at this low point proved exceptionally rewarding for level-headed investors that bought into the fear and uncertainty. It was a powerful reminder that markets often rebound as quickly as they declined, a truth clearly illustrated in the market’s recovery from that moment onward.

While today’s economic environment differs significantly from the COVID-19 crisis, the fundamental lesson remains the same: periods of heightened fear and uncertainty often present extraordinary opportunities to invest in high-quality businesses at substantial discounts. Companies with robust business models, solid balance sheets, and strong competitive advantages usually survive, and even thrive, after the crisis passes.

When Prices Drop, Conviction Counts

As the market started dipping from mid-February 2025, I reassessed the fundamentals of every holding in my concentrated portfolio. Despite Visa (V 0.00%↑) being an exceptional company, its stock price rally from early August 2024 when I had initiated the small position had pushed its valuation to uncomfortable levels, widening the gap between the business fundamentals and its stock price. Recognizing this overvaluation, I decided to liquidate my Visa position on March 7, 2025, locking in a 30% profit and freeing capital to deploy into companies I hold higher conviction in and believe were trading at attractive discounts amid the market decline. The rationale behind my decision is effectively summarized by Warren Buffett in this speech:

“[…] the only question with every stock, every day, and you don’t do this frequently, is ‘can I get more for my money someplace else?’ […]

You can rearrange your business empire which you own through that little portfolio that you have at a moment’s notice with practically no cost. It’s a huge advantage that people turn into a disadvantage. […]

What tells you whether you should keep owning it [stock] is what you expect the company to do in the future versus the price at which you’re selling now, compared to the other opportunities of businesses that you think you know equally well and make that same comparison.”

As the market downturn continued amid international trade tension and uncertainty, I deployed new capital into my investment account, steadily buying great businesses at discounted prices without attempting to predict or time the market bottom.

When the market sell-off intensified following the aggressive international trade measures introduced by President Trump on April 2, 2025, I took another step to enhance my portfolio’s resilience and growth potential by selling at a 13% loss my position in a small-cap holding, North American Construction Group (NOA 0.00%↑), a company in which I held comparatively lower conviction. This exit allowed me to unlock additional capital and take advantage of compelling discounts on my high-conviction holdings.

This deliberate approach aligns closely with Warren Buffett’s philosophy of evaluating each stock in comparison to available alternatives, ensuring capital is always optimally allocated based on the relative attractiveness of current prices and long-term business fundamentals.

I can’t know if stocks will go lower tomorrow or surge again based on a new development. President Trump could easily post on social media again, reversing yesterday’s optimism. Market timing based on unpredictable external factors is inherently flawed. Instead, I focus on company’s fundamentals, a grounded and reliable approach. Before making any purchase, I ask myself whether I am comfortable with the company’s current stock price relative to its intrinsic value. If the answer is yes, I buy, regardless of whether the price might dip further in the short term. This mindset is well captured by Mohnish Pabrai, who described in an article in November 2001, two months after the tragic events of September 11, 2001, how moments of market panic can open rare windows of opportunity for level-headed investors:

“The public equities markets are mostly efficient, but not fully efficient. Events like Sept. 11 tend to widen the efficiency gap […] In times like these, Mr. Market gets severely depressed and can only think about doom, gloom and uncertainty.

Investors who use times likes these to make investments in a few great businesses and make these investments meaningful portions of their portfolio for the long haul can take advantage of these inefficiencies. With his occasional mood swings, Mr. Market offers a wide array of great businesses on ‘clearance sale’ for a few weeks every few years. This is a good time to take advantage of Mr. Market.”

Pabrai’s perspective resonates deeply with how I’ve been managing my own portfolio during this period of heightened volatility. In the spirit of sharpening focus and increasing exposure to my highest conviction ideas, I deployed new capital and exited two smaller positions (V 0.00%↑ and NOA 0.00%↑), concentrating my portfolio further into my high-conviction holdings. This move was driven by a deliberate effort to double down on the businesses I understand best and believe are most attractively priced relative to their long-term potential. As a result, my top three holdings now make up 59% of my portfolio, up from around 51% prior to the past two months’ correction, despite them not being immune to the broad, panic-driven market decline.

Year-to-date, my portfolio is down around 16%, a reflection of the market-wide sell-off rather than a change in business quality. I’m comfortable with this level of concentration because I see these companies as resilient, competitively advantaged, and well positioned to compound value over the next decades. I remain confident in this approach irrespective of heightened volatility, fully aware, and accepting, that a concentrated portfolio of high-quality businesses will be more volatile than a broadly diversified portfolio or an ETF tracking an index composed of hundreds of companies.

Amazon’s Mispriced Opportunity

Despite the run-up in stock prices from yesterday’s optimism, many great businesses remain significantly below their intrinsic value. For example, Amazon is attractively priced under $200 per share relative to its fundamental strengths, growth prospects and historical performance.

The company is generating a record $115.9 billion a year in operating cash flow (OCF), up nearly 13x from 2015, representing a 30.85% compound annual growth rate (CAGR). Despite this remarkable growth, Amazon’s price-to-operating cash flow (P/OCF) ratio currently stands at just 17.5, well below its historical average of 26.7. This valuation compression suggests that the market is discounting Amazon’s long-term cash generation potential, even as its operating cash flow margin has increased to a solid 18.2% demonstrating increased operational efficiency over time. The combination of multiple drivers of future growth (third-party seller, advertising and Amazon Prime on the e-commerce front and cloud & AI growing demand on the AWS front), strong operating performance and a historically low valuation multiple presents a compelling opportunity.

Final Thoughts

It’s impossible to predict exactly when stock markets recover after a market-wide sell-off, clarity often emerges only in hindsight. However, what history demonstrates time and again is that investing during periods of uncertainty and widespread fear, though mentally challenging, tends to reward patient, disciplined investors. Over time, markets inevitably recover, driven by human adaptability, innovation, and the relentless pursuit of growth and profitability. And in the long run, stock prices have a strong tendency to converge toward the fundamental performance of the underlying businesses.

Today, many high-quality companies are trading at meaningful discounts due to short-term uncertainty. As an investor, I choose to seize this moment, fully aware that I can’t know precisely when the recovery will begin or how quickly it will unfold. What I do know is that investing in resilient, well-managed businesses at attractive valuations during turbulent times has historically proven to be a winning strategy.

In summary, I will continue to invest methodically, ignoring short-term market noise, posts on social media, market commentators and scary headlines. My approach is grounded in business fundamentals and valuation discipline, using moments of panic as opportunities to build and grow positions in exceptional companies.

Focus on long-term value, maintain composure amid volatility, and invest consistently when opportunities arise, this is the mindset shared by great investors like Buffett, Lynch, and Pabrai.