Alphabet Inc. (Google) Q1 2026 Results: Cloud Breaks Escape Velocity, Multiple Catches Up

Cloud at +63%, Search at +19%, OCF/share compounding 32% YoY, and the P/OCF multiple has run from ~20x to 28x

Alphabet Inc. (GOOGL 0.00%↑) reported Q1 2026 results on April 29, 2026. The headline numbers were the strongest I have seen since I initiated the position in October 2022. CEO Sundar Pichai opened the earnings call with the line that captures the quarter:

“It’s clear that our AI investments and full stack approach are driving performance across our business.”

I take that statement seriously despite market commentators did not in 2023, when AI Overviews launched and they feared for nearly two years that Google was about to lose Search. The 2025 year-end results and Q1 2026 numbers are the most direct evidence yet that the full stack (silicon, models, products, distribution) is monetizing.

In Q1 2026, Cloud revenue grew 63.4% year-over-year (YoY) to $20 billion, with operating margin expanding to 32.9% and a $462 billion backlog. Search grew +19.1% YoY to $60.4 billion, with paid clicks +13% YoY and cost-per-click +5% YoY - both volume and price rising. Trailing twelve months (TTM) operating cash flow reached $174.4 billion, up 31.5% from the prior year. Cloud added $2.3 billion of net new revenue quarter-over-quarter (QoQ), more than AWS on a base half AWS’s size. Meta and Amazon are growing ads faster than Google in percentage terms; Google’s offset is the agentic-commerce surface - asymmetric, not yet monetized.

In the Q3 2025 article I argued that the full-stack flywheel was meeting relentless execution. Six months later the flywheel has clearly accelerated: Search re-accelerated, Cloud broke escape velocity, capital allocation pivoted, and management raised CapEx guidance again. This article walks through what I see, what changed since my last earnings results article in November 2025, and how my valuation looks anchored on operating cash flow (OCF).

Q1 2026 Highlights

Here are the five data points I am writing down for this quarter:

Revenue $109.9 billion, +22% YoY - the 11th consecutive quarter of double-digit growth.

Operating margin 36.1%, +2 points YoY. Operating income $39.7 billion (+29.7% YoY); TTM operating cash flow climbed +31.5% YoY from $132.6 billion a year prior to $174.4 billion.

Search & Other revenue re-accelerated to +19% YoY ($60.4 billion vs. $50.7 billion in Q1 2025); paid clicks +13% YoY, cost-per-click +5% YoY - both volume and price rising. More than 30% of customer Search spend now flows through AI-enabled campaigns (AI Max or Performance Max), up from roughly zero two years ago.

Cloud revenue had its first $20 billion quarter, up 63.4% YoY; operating income tripled YoY from $2.2 billion to $6.6 billion, and operating margin expanded to 32.9%, a +84.8% YoY jump. Revenue from products built on Google’s generative AI models grew “nearly 800% year over year”. The acceleration is real and the operating leverage is showing.

Waymo crossed 500,000 fully autonomous rides per week, doubling in less than a year; received $16 billion in funding in February 2026, with the significant majority funded by Alphabet, the largest single funding event in Other Bets’ history.

Q1 2026 Lowlights

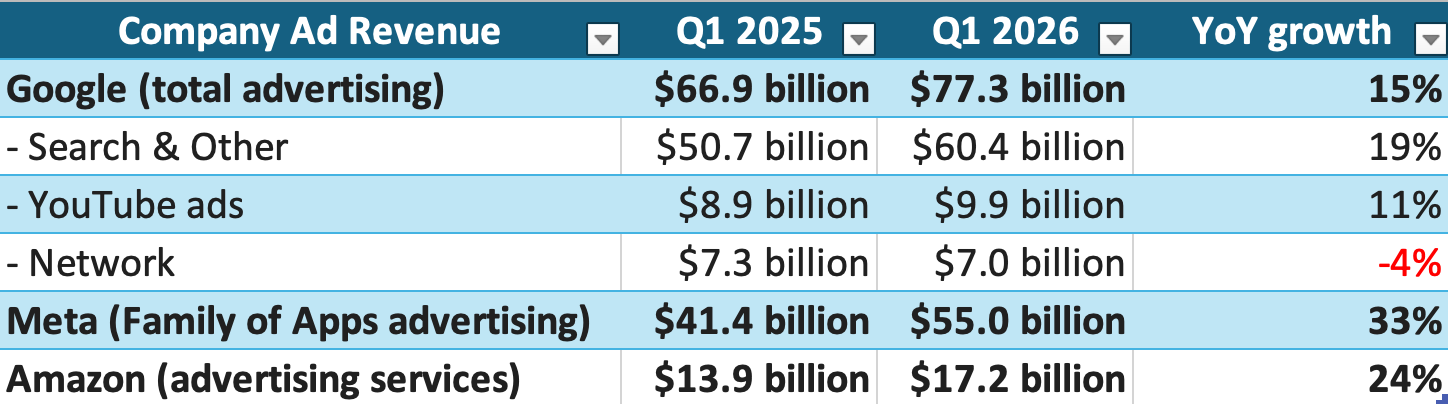

Google is no longer the fastest-growing major ad platform. Meta’s Family of Apps advertising grew +33% YoY to $55 billion; Amazon advertising grew +24% YoY to $17.2 billion. Google’s total advertising grew +15% YoY to $77.3 billion. Google is losing market share in percentage terms because the base is bigger and Meta’s AI-creative engine plus Amazon’s retail-media flywheel are compounding faster. Inside Google’s mix, YouTube ads at +11% are slower than the rest of the ad market, and Network ads at -4% are the slow leak.

TTM Free Cash Flow (FCF) has compressed dropping from $74.9 billion in Q1 2025 to $64.4 billion a year later - CapEx ($109.9 billion TTM, +90.4% YoY) is outrunning OCF growth (+30.5% YoY). The Q1 buyback pause plus the $31.4 billion of debt issuance is the cleanest evidence that growth CapEx and inorganic capacity (Wiz & Intersect acquisitions) additions are now eating the entire after-dividend cash flow. The old Alphabet was a capital-light advertising monopoly; the new Alphabet is a capital-intensive AI infrastructure platform that still operates an advertising monopoly.

Services: Search Re-accelerates, Network Drags

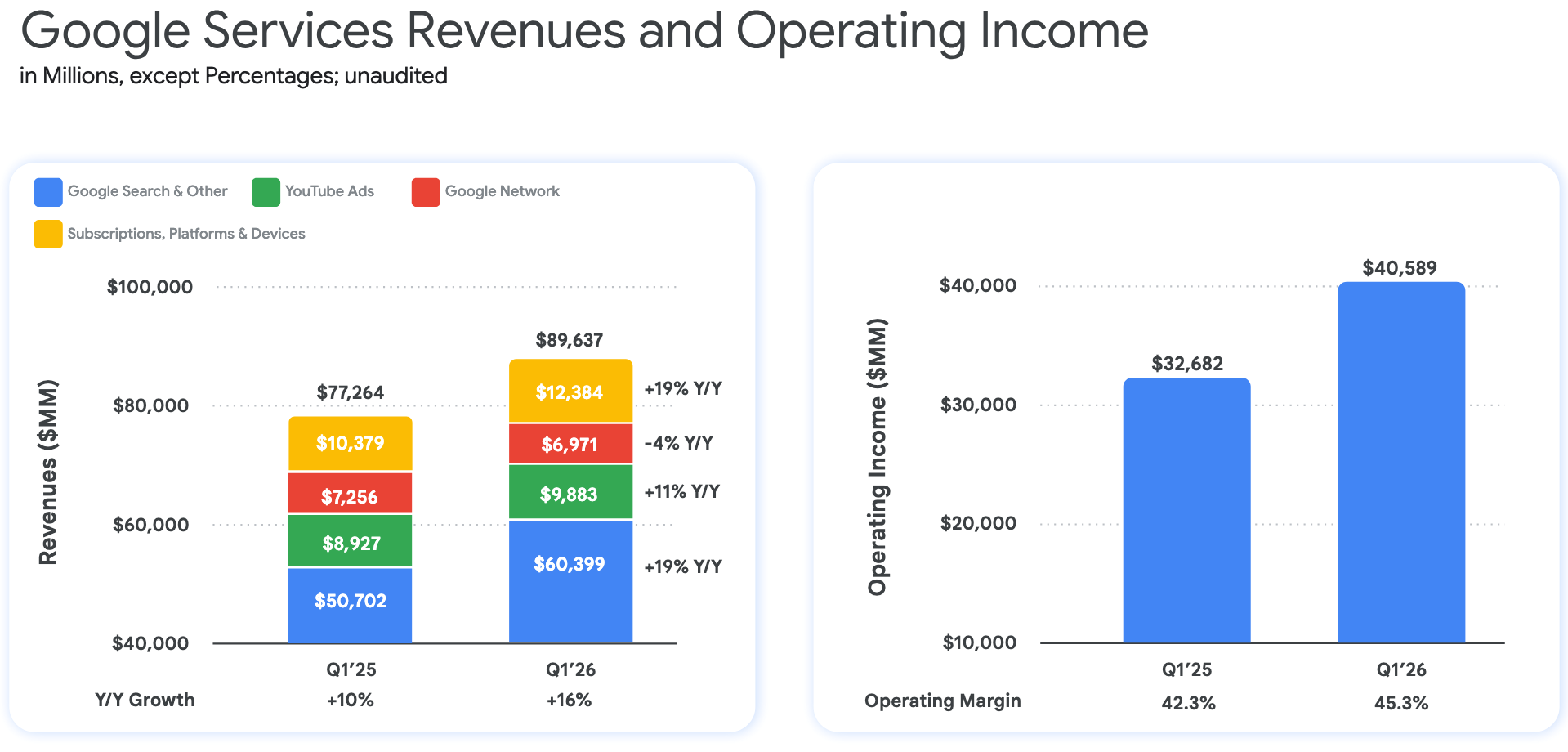

Google Services revenue was $89.6 billion (+16% YoY), with the segment flexing the operating leverage muscle at a 45.3% operating margin and $40.6 billion of operating income (+24% YoY). Inside Services:

Search & Other: revenue came in at $60.4 billion (+19.1% YoY) - the standout. The vertical drivers were retail and finance, with health contributing.

YouTube ads: revenue grew 11% YoY to $9.9 billion - driven by direct response and brand. Living-room watch time keeps growing (over 200 million hours/day in the U.S.), and YouTube has now led streaming watch time in the U.S. for three consecutive years.

Subscriptions, Platforms & Devices: revenue was $12.4 billion (+19% YoY) - the strongest quarter ever for consumer AI plans, driven by Gemini App adoption. Total paid subscriptions across Alphabet have reached 350 million, with YouTube and Google One as the key drivers. YouTube Music & YouTube Premium had its largest non-trial subscriber gain since launch in 2018.

Network ads: revenue came in at $6.98 billion (-4% YoY) - the only piece of Services in decline. This has been a slow leak for several quarters as ad budgets shift onto first-party AI experiences. I would not extrapolate; it is the smallest and shrinking share of the mix.

CBO Philipp Schindler was strongest on the ad-stack mechanics, naming three monetization levers: ads quality, advertiser tools, new AI user experiences, with two concrete client results:

“Take Hilton EMEA. They captured one third more clicks for a fifth of the spend, while simultaneously increasing the average booking value by 55%. And Etsy saw a 10% search volume uplift, with 15% of those queries being net new to their business.”

The aggregate adoption number was the more important data point in the same passage:

“More than 30% of our customers’ Search spend now uses AI enabled campaigns AI Max or Performance Max. And these advertisers are seeing more conversion for the same spend.”

Three out of every ten advertiser dollars on Search are now flowing through Google’s AI-driven ad products, up from roughly zero two years ago. That is a measurable shift in advertiser behavior, not a forecast.

The 10-Q filing gives the cleanest read on what is actually happening underneath that growth. Q1 2026 monetization metrics for Search & Other with paid clicks up 13% YoY and cost-per-click +5% YoY; both volume and price are rising. Maturing ad businesses rarely see that combination, usually you grow one at the expense of the other. Google Network impressions fell 9% while cost-per-impression rose 6%; budget rotating off third-party inventory onto first-party AI surfaces.

A consequential exchange on the call was on ad coverage. Schindler:

“I think with the ability of AI to better understand intent and a lot of other vectors around it, I think there is upside in that coverage number.”

For a business that has spent two decades at roughly 20% ad coverage on Search, that is a non-trivial admission that the AI-driven conversational format is opening monetizable inventory that did not exist before. Schindler framed the dynamic explicitly:

“AI is fundamentally changing how the world searches for, and how it accesses information. Queries are at an all time high. […] And overall, just the understanding that we have with Gemini on intent has just significantly expanded our ability to deliver ads on longer, more complex searches that were previously really difficult to monetize.”

The Universal Commerce Protocol (UCP), now with Amazon, Meta, Microsoft, Salesforce, and Stripe joining the Tech Council alongside founding members Shopify, Etsy, Target, Wayfair and Google, is the mechanism. Ulta Beauty has already gone live with agentic checkout inside AI Mode and the Gemini app.

Two new ad formats Schindler called out in the same prepared remarks are also worth tracking. Direct Offers in AI Mode - a Google Ads pilot Gap, L’Oréal and Chewy have signed up to test - places ad inventory inside conversational responses themselves. Separately, Google is testing a new ad format that displays retailers who sell the products AI Mode organically recommends. Both formats reinvent ads for the conversational layer rather than retrofitting Search-style auctions into AI surfaces. Neither is yet generating disclosed revenue, but they are the early answer to “what does the agentic ad format look like?”.

The 2024 bear case said generative AI would compress the funnel and remove the click. The segment’s Q1 numbers - 19% revenue growth, queries at an all-time high, cost-per-AI-response down 30% - argue against that directly. The bear case worth engaging with now is sharper: someone else (e.g. ChatGPT, or a vertical agent on top of Amazon) owns the starting point for commercial intent, eroding Google’s two-decade hold even as Search keeps growing.

UCP and AI Mode checkout are Alphabet’s answer. Advantages: a frontier model, the largest distribution surface in consumer software, and a payment ecosystem the biggest U.S. retailers are now plumbing into. Risk: Google has tried commerce repeatedly over twenty years and has rarely won. The difference this time is that the agent does the work the user used to do (compare, decide, check out) inside the same surface where the intent originated. For the first time in Search’s history, the discovery layer and the transaction layer can collapse into one. However, Alphabet has disclosed no GMV, no take rate, no transaction-layer revenue, but the optionality is non-zero and asymmetric.

Where Google Stands Versus Meta And Amazon In Ads

How Google’s ad franchise stacks up against the other two scaled players, all reporting within hours of each other.

Meta and Amazon are both growing their ad businesses meaningfully faster than Google in percentage terms. Meta at +33% on a $55 billion base is the standout, driven by 19% ad impressions growth and a 12% increase in average price per ad, with the AI-creative engine now used by 8+ million advertisers (up from 4 million at end-2024) and a Value Optimization run-rate above $20 billion. Amazon advertising sits at $70+ billion on a TTM basis and grew 24% YoY - it is taking durable market share in performance advertising via retail-media ads and ad-supported Prime Video. Google’s added $10.4 billion YoY for total advertising, second to Meta, and a smaller percentage on a larger base.

Google is no longer the fastest-growing major ad business, but it remains the most monetizable surface in the funnel because it sits closest to commercial intent. Meta wins on creator-and-creative AI; Amazon wins on retail-media flywheel. Google’s offsetting bet is the agentic-commerce surface - asymmetrically larger than at either competitor because Google sits at the discovery layer with a first-party model. The risk: Meta’s AI-creative engine and Amazon’s retail-media flywheel keep compressing the gap before agentic-commerce monetization shows up in Google’s revenue line.

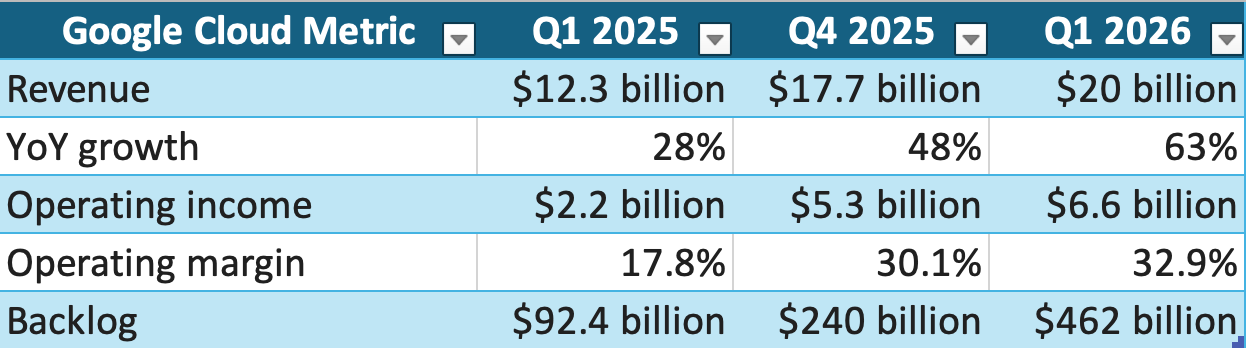

Cloud: $20 Billion Revenue, 32.9% Margin, And A $462 Billion Backlog

Six months ago I called this segment the “full-stack flywheel”. This quarter reinforced the framing.

Three things I had not seen before in the segment’s disclosure:

Enterprise AI is the primary growth driver: “revenue from products built on our gen AI models grew nearly 800% year over year”. New customer acquisition doubled YoY. The number of $100 million to $1 billion deals doubled. Existing customers outpaced their initial commitments by 45%, an acceleration vs. last quarter.

The AI infrastructure stack got cheaper to run and faster to deploy: at Cloud Next 2026, Google introduced two eighth-generation TPUs - TPU 8t (training, 3x the processing power of Ironwood, 7th generation TPU) and TPU 8i (inference, 80% better performance per dollar than the prior generation); and “since upgrading AI Overviews and AI Mode to Gemini 3, we have reduced the cost of core AI responses by more than 30%, thanks to continued hardware and engineering breakthroughs”. That is the core of the aggregator economics thesis playing out in real time: control the silicon and the model, drive marginal cost toward zero, then either expand usage at the top or expand margin at the bottom - Google is doing both at once.

Cloud is starting to sell TPUs into customers’ own data centers. Pichai framed this as opportunistic rather than strategic - capital markets firms, frontier AI labs, and high-performance-compute customers want TPUs on-premise. Most of these revenues will land in 2027. The $462 billion backlog already includes some of these contracts. By selectively letting a small set of customers run the highest-value AI workloads on TPUs in their own facilities, Alphabet prevents those workloads from defaulting to NVIDIA-only infrastructure and leaving the Google ecosystem entirely. Unit economics on a one-off TPU shipment are worse than on a multi-year GCP contract. CFO Anat Ashkenazi was direct about the lumpiness: “revenues from TPU hardware sales will fluctuate from quarter to quarter”. That creates a backlog-quality question I am now watching. A dollar of recurring GCP consumption is not the same as a dollar of episodic hardware sale. As the latter grows, the headline backlog number gets harder to interpret; Ashkenazi said the “majority” of the $462 billion is typical GCP contracts.

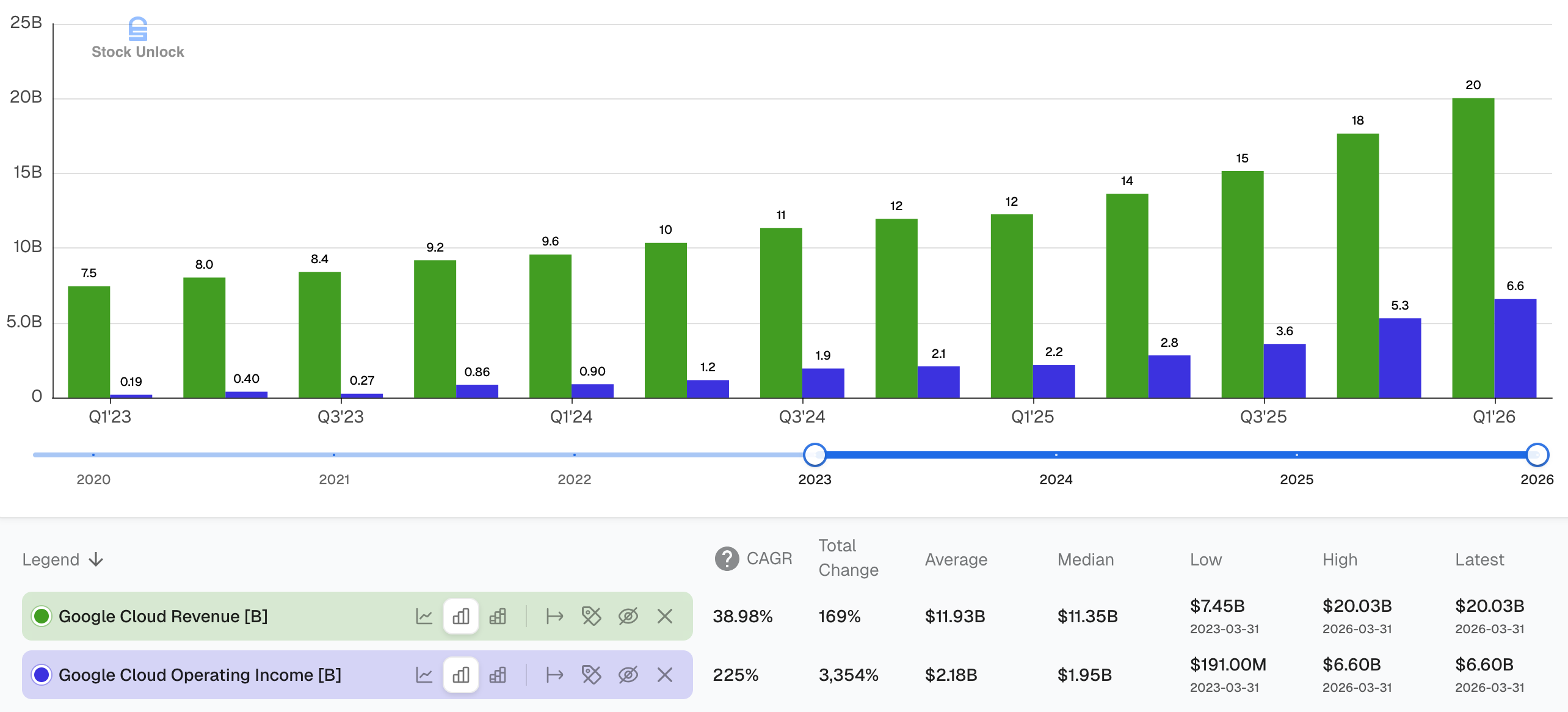

The longer arc is even more telling than the YoY view. Twelve quarters ago, Q1 2023, Google Cloud was a $7.5 billion/quarter business with $191 million of operating income and a 2.5% margin. Today it is a $20 billion/quarter business with $6.6 billion of operating income and a 32.9% margin. Revenue compounded at 39% annually over that span; operating income compounded at 225%. The pattern is consistent across the chart: revenue scaling steadily, then operating income inflecting and pulling away as the segment crosses break-even and operating leverage takes over. The YoY acceleration to +63% revenue growth and the tripling of operating income are the new fact pattern.

On the broader competitive position, Pichai’s framing on the call is a clean articulation of Alphabet’s argument:

“We are unique in the market because of our vertically optimized AI stack and the way we co-develop the components from our infrastructure and models, to platforms and the tools, to applications and agents. And the fact that we own frontier models, own the silicon, really helps us stay ahead of the curve. […] I think we are the only provider on the market that offers all of these in a vertical stack.”

I do not take CEO claims of uniqueness at face value, but the Q1 numbers (63.4% segment growth, 32.9% margin, 800% gen-AI revenue growth, the cost-per-AI-response cut) are consistent with the claim. Pichai explicitly anchored the CapEx spending to “a robust ROIC framework”, and said allocation decisions across business units are governed by it.

Pichai called the GCP momentum “tangible demand signals” with just over half of the $462 billion backlog converting to revenue within 24 months: roughly $230 billion of GCP revenue is contracted to land between Q2 2026 and Q1 2028, against $58.7 billion of Cloud revenue for all of 2025. The growth pipeline is fully funded for the next two years. The question is whether Google can build the capacity to deliver it. Pichai’s answer on the call was unambiguous: “Our Cloud revenue would have been higher if we were able to meet the demand”.

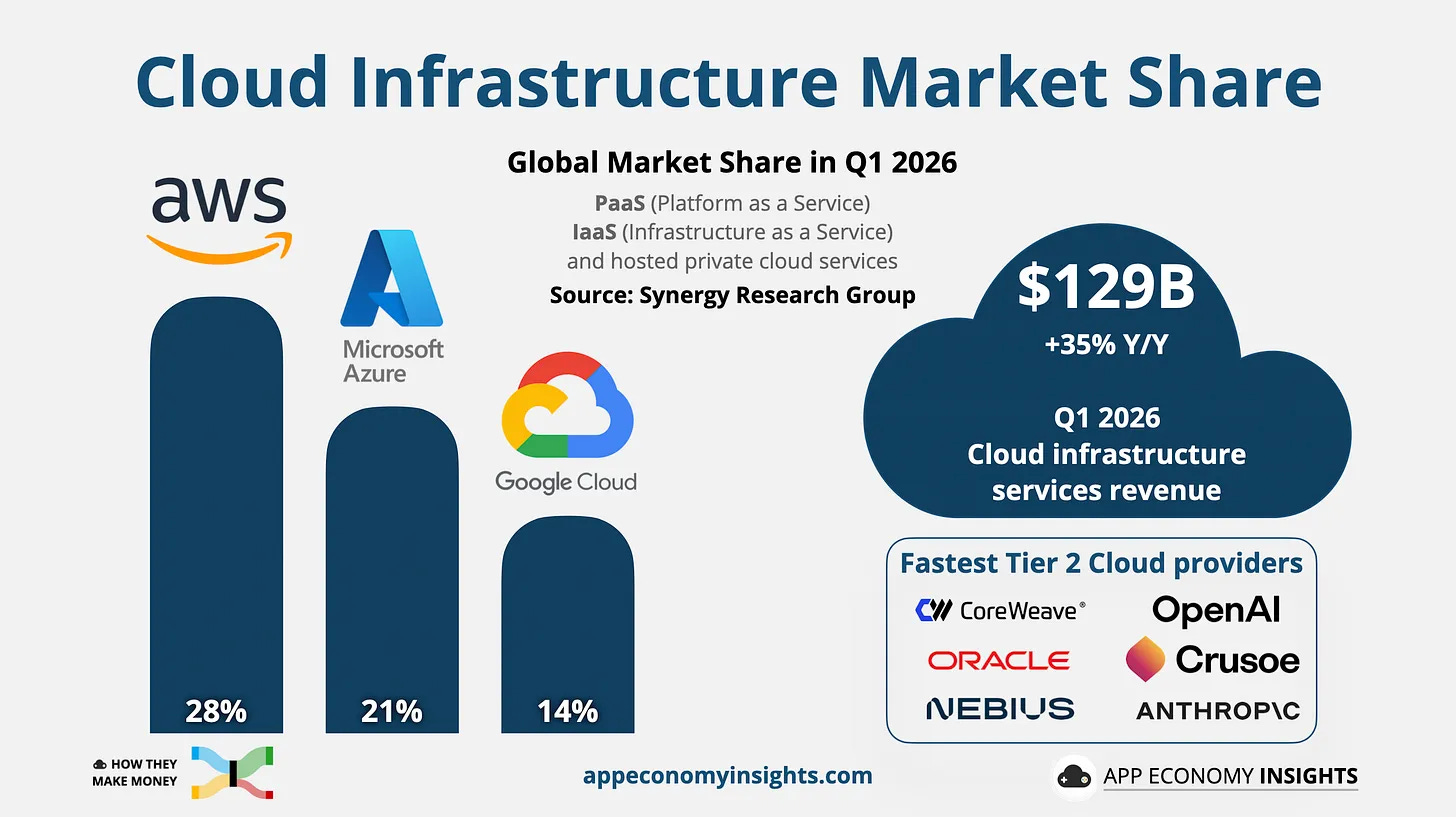

How Google Cloud Stacks Up Against AWS And Azure

All three major hyperscalers reported Q1 2026 results on the same day, and the picture is unambiguous on growth.

¹ Microsoft does not break out Azure as a standalone dollar line. The figures here apply Synergy Research Group’s cloud market share estimate: Microsoft = 21% of the global cloud infrastructure services market in Q1 2026 to Synergy’s market size of $128.6 billion, giving $27 billion for Q1 2026. Q4 2025 estimated by applying the same ~21% share to Synergy’s implied Q4 2025 market ($119 billion). Q1 2025 derived from Microsoft’s reported “Azure and other cloud services” +40% YoY growth back-applied to Q1 2026.

² Microsoft’s reported growth rate for “Azure and other cloud services” within Intelligent Cloud (Intelligent Cloud segment as a whole grew 30% to $34.7 billion in Q1 2026).

Cloud has minimal seasonality and Google Cloud added more net new revenue sequentially than AWS this quarter, on a base half AWS’s size. AWS’s $2 billion was its biggest Q4-to-Q1 sequential increase ever. Microsoft added roughly $2 billion on the Synergy-basis estimate. Google added $2.3 billion on a $17.7 billion base.

The market frame from Synergy Research Group: Q1 2026 enterprise cloud infrastructure spending was $129 billion globally, +35% YoY - the ninth consecutive quarter in which the YoY growth rate has accelerated, the fastest market-wide growth since Q4 2021 (when the market was 40% of its current size). AWS leads at 28% market share, Microsoft 21%, Google 14%; the three together hold 63% of quarterly cloud infrastructure spend.

Two takeaways from putting the company numbers next to the market data.

Google is taking market share: AWS at 28% share is growing +28% YoY, below Synergy’s +35% market growth, and its share is broadly stable. Azure at +40% YoY growth is gaining a small amount of share. Google at +63% YoY is gaining market share materially on the smallest base of the three, and is now growing roughly twice as fast the market rate. Synergy’s estimated 14% Google market share has expanded from low double digits over the last two years.

Margin still belongs to AWS in absolute dollars, but the margin gap is closing fast: AWS’s $14.2 billion of operating income is more than double Google Cloud’s $6.6 billion, that is what a $150+ billion run-rate business looks like once it has paid down its initial CapEx wave. The direction is what matters: Google Cloud’s operating margin expanded from 17.8% to 32.9% in twelve months, while AWS margin sits stable in the high-30s (37.7% in Q1 2026). At current trajectories, Google Cloud’s operating margin converges with AWS’s inside two years, on a base growing more than twice as fast.

The 16-Billion-Tokens-A-Minute Tell

One detail from the prepared remarks that I think matters:

“Our first party models now process more than 16 billion tokens per minute via direct API use by our customers, up from 10 billion last quarter.”

From 10 to 16 billion tokens/minute QoQ is the clearest token-volume disclosure Google has given. Pair it with the customer-tier disclosure: “330 Google Cloud customers each processed over one trillion tokens. 35 [customers] reached the ten trillion token milestone”. That is the kind of usage curve that turns a backlog number into actual P&L over the next several quarters.

Gemini Enterprise paid monthly active users (MAUs) grew 40% QoQ. Partner-channel seats grew 9x YoY.

Capital Allocation: Debt In, Buybacks Out, M&A On

This is the line item that surprised me most when I read the cash flow statement.

Q1 2026 changes vs. last year:

CapEx more than doubled ($35.7 billion vs. $17.2 billion): 60% servers, 40% data centers and networking. 2026 guide raised to $180-190 billion (from $175-185 billion) to absorb the Intersect acquisition. Ashkenazi: “these strong results reinforce our conviction to invest the capital required to continue to capture the AI opportunity. As a result, we expect our 2027 CapEx to significantly increase compared to 2026”.

Buybacks paused: Zero in Q1 2026 vs. $15.1 billion in Q1 2025. Diluted shares rose modestly (12,238 million Q1 2026 vs. 12,116 million issued at year-end 2025 due to SBC vesting). Deliberate pause, not structural shift; dividend raised 5% to $0.22/share.

Debt-funded M&A: Alphabet issued $31.1 billion of senior unsecured notes in Q1 to fund the Wiz close ($29.5 billion) and Intersect acquisition ($5.9 billion). Long-term debt rose to $77.5 billion from $46.5 billion at year-end 2025. Against $174.4 billion of TTM OCF plus $126.8 billion of cash and marketable securities on the balance sheet, leverage remains trivial. Alphabet is consciously using the balance sheet rather than retained cash flow for the first time in years.

Q1 FCF was depressed by front-loaded CapEx and $33.6 billion of acquisition cash hitting the same quarter. The buyback pause plus debt issuance is a financing mix shift to fund the two large acquisitions and the AI-CapEx ramp without depleting the cash buffer. The dividend hike says management does not see financial stress.

Time will tell if growth CapEx and inorganic capacity additions will keep eating the entire after-dividend cash flow - this is part of the growth-vs-maintenance CapEx call I made in February 2026.

Waymo: The Inflection From “Someday” To Operating Network

Other Bets revenue was $411 million in Q1; operating loss widened to $2.1 billion. Two segment moves made it functionally about Waymo: Verily completed an external capital raise and was deconsolidated; GFiber announced a combination with Astound Broadband and will deconsolidate at deal close (expected Q4 2026). What is left is increasingly Waymo plus Wing.

Waymo crossed 500,000 fully autonomous rides per week; doubled in less than a year, and now operates in 11 U.S. cities (six new in 2026, including Nashville). The scaling curve I have been watching since the Uber Q3 2025 article, and on the evidence so far, this is not a beneficiary-vs-threat story. Both Uber and Waymo will scale.

In February 2026, Waymo received $16 billion in funding, the significant majority funded by Alphabet, the largest single funding event in Other Bets’ history. Management is preparing Waymo for a meaningfully bigger build-out than the eleven-city footprint implies today. This is capital-intensive investment at scale, not a small-budget science project.

Other Bets has historically obscured Waymo as much as revealed it - a single line that lumped life-sciences, fiber ISP, autonomy, and several smaller efforts. Stripping Verily and GFiber out leaves a cleaner segment in which Waymo’s economics become at least theoretically separable. I do not expect Waymo to IPO, no need when the parent funds it from $174.4 billion of TTM OCF, but at some point the market will start asking what Waymo is worth on its own. The answer is no longer obviously zero.

What would unlock a real Waymo valuation: revenue per ride, gross profit per ride, or city-level cohort economics. None disclosed today. Until they are, Waymo is an option whose strike price is whatever future quarter management chooses to pull back the curtain.

Valuation: Pricing The Full-Stack Compounding Engine

I anchor Alphabet on operating cash flow (OCF) per share. Same reasons as in the Q3 2025 results article and the December 2025 article on hyperscaler depreciation: in a CapEx ramp, FCF gets depressed by growth CapEx that has not yet earned its way into the revenue line, and accounting earnings get distorted by useful-life choices and large mark-to-market swings on equity stakes. OCF stays close to actual cash generated by the business.

TTM OCF per share has compounded at 21.6% per year over the past decade and has accelerated to 32% YoY, the very window in which the AI-CapEx mega-cycle has intensified (+90.4% YoY): At Q1 2026, TTM OCF per share was $14.25, up from $10.79 a year ago. As the CapEx cycle has heavied up, the cash-generation engine has compounded faster, not slower. That is the cleanest read I have on whether the spend is impairing the business, and so far the answer is no.

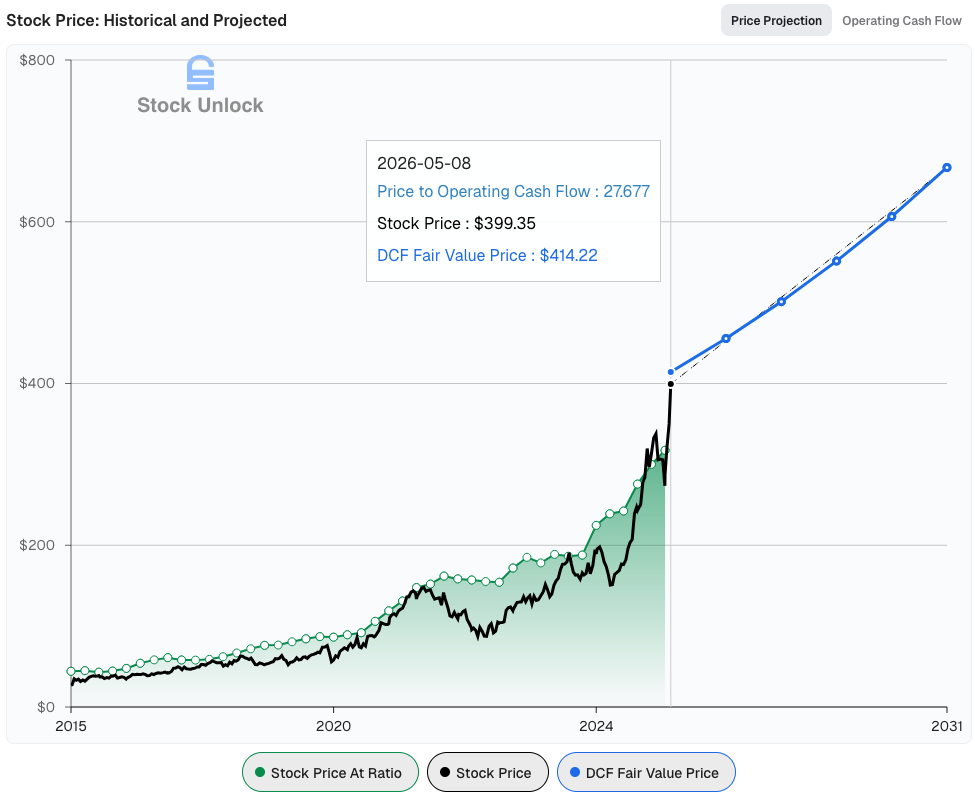

A 5-year discounted cash flow (DCF), kept deliberately conservative on growth and on share count assumptions: TTM OCF of $174.4 billion compounding at 15% per year for five years gets to $350.7 billion in Q1 2031, well below both the 10-year average and compounding run rate of OCF/share. Share count drifts from 12.24 billion today to 11.64 billion (-1%/year; conservative given the Q1 2026 buyback pause; if buybacks resume at the prior $60-80 billion/year pace, year-5 share count lands closer to 11 billion). That gives year-5 OCF/share of $30.13. Apply a 22x P/OCF exit multiple, in line with what the market has been paying for high-quality compounders with growing OCF, and year-5 implied price is ~$662.9/share, plus ~$4.2/share of cumulative dividends along the way, for a total return of ~$667.1/share. Discounted back at my 10% portfolio hurdle rate, fair value is ~$414.2/share today. If Cloud holds 40%+ growth another year and cost-per-AI-response keeps falling, OCF/share could compound above 15%, in which case fair value today moves into the high $400s. If 2027 CapEx is materially higher without a corresponding OCF response, fair value compresses toward the low $300s.

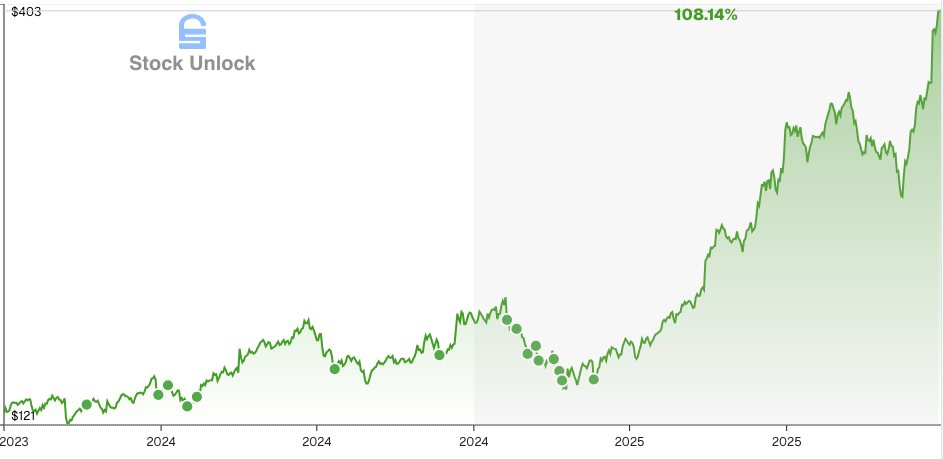

At today’s price of $399/share, Alphabet trades at 28x TTM OCF/share, meaningfully above both the 22x exit multiple I assume in the DCF and the 10-year average of 17.4x. The stock has run up 108% as the operating numbers have caught up to and overtaken the bull case I was making in December 2024.

Against my conservative fair value of $414.2/share, today’s $399/share price is a small 3.7% discount, and the implied 5-year IRR from today is 10.8%, slightly above my 10% portfolio hurdle rate. In my DCF, GOOGL is fairly priced after a run that has compressed the margin of safety. That does not change my view of the business - Q1 2026 numbers tell me the next several years could sustain mid teens OCF/share compounding. I am happy to hold at this price.

If the price multiple were to reset back toward the high teens on TTM OCF, I would add aggressively, the way I did during the March-April 2025 tariff scare sell-off.

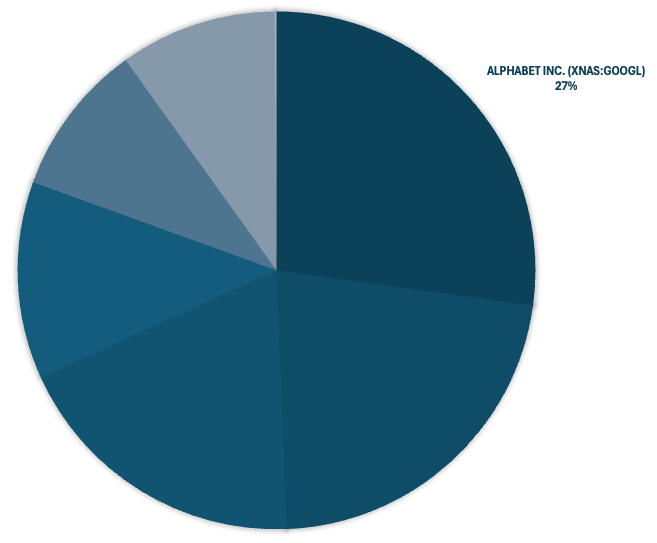

Until then, I firmly believe in the future outlook of the company and Alphabet remains my largest portfolio position at 27%.

Final Thoughts

Q1 2026 is the most decisive evidence yet that the full-stack approach is not a slogan - Search re-accelerated. Cloud crossed from “fast-growing infrastructure business” to “fast-growing, scaling-margin infrastructure business”. Token volumes, the backlog doubling, and the cost-per-AI-response cut all describe one thing: marginal cost falling and demand rising at the same time.

The question I came into 2025 with, “does AI break Search?”, is now the wrong question.

The market spent most of 2024 and early 2025 worried Google was the AI loser. The numbers now say otherwise. The risk now is not that the thesis breaks, it is that I get complacent about a business executing better than I had expected when I first underwrote it in late 2022, or that I get tempted by a price that has run ahead of my conservative fair value to trim a position whose underlying compounding rate is now accelerating.