The Portfolio I Can Explain to a Ten-Year-Old

Why "know what you own" is the only thing that keeps the stomach calm when the brain wants to sell

In a 1994 talk, former Fidelity Magellan fund manager and legendary investor Peter Lynch put it plainly:

“The single most important thing […] is to know what you own. I’m amazed how many people own stocks they would not be able to tell you why they own it […] If you can’t explain a ten-year-old, in two minutes or less, why you own a stock you shouldn’t own it.”

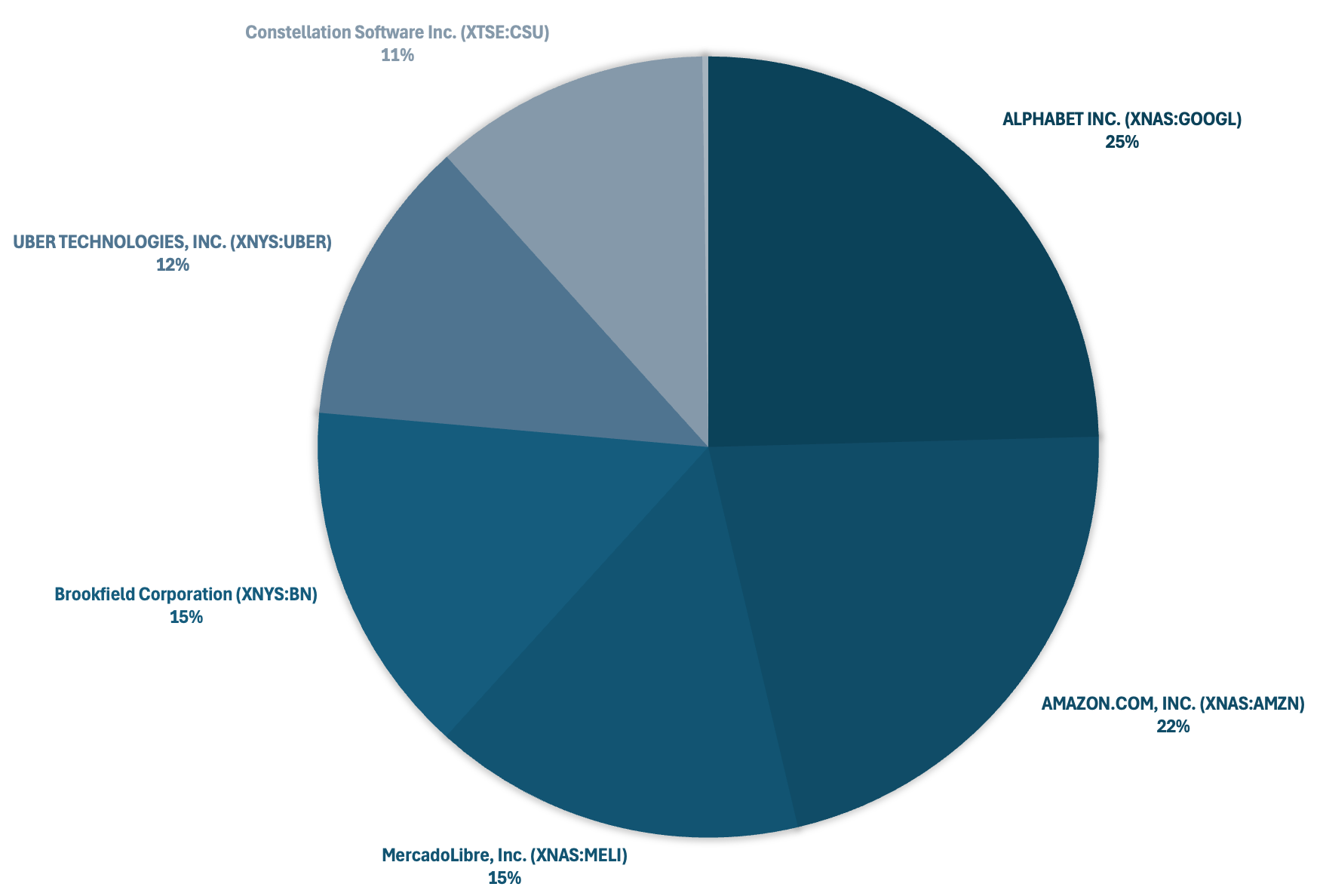

I put my own portfolio to that test. Below are my six holdings, in order of weight as of July 2026, each in a few sentences, with the risks attached. Lynch’s point was that the market falls 10% about every two years and 25% about every six - a cadence I put updated numbers to in Why Investing Is Hard, Part 1: The Price of Admission, where the S&P 500’s average intra-year drop since 1980 has been 14.1% and yet the index finished the year positive in 35 of those 46 years.

Declines are the schedule, not the exception, and the only investors who use them instead of fearing them are the ones who already know what they hold.

How I Invest

Before the companies, the principles - they’re the same ones I set out in my very first newsletter post, Introduction to Level-Headed Investing. I buy, hold and maintain a portfolio of individual businesses for the long term with a disciplined, long-term approach - never speculating, gambling, or buying out of fear or hype. The businesses I want share a recognizable profile: dominant market position with widening moats, operating leverage that expands margins as they grow, ample reinvestment runways, led by capable management that allocates capital intelligently. I buy them at a rational price. As Warren Buffett put it in the 1989 Berkshire Hathaway shareholder letter, “it’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price”, and I am willing to pay a fair price for genuine quality.

I try to get right three things: company selection, temperament, and portfolio management. Selection is identifying high quality businesses and acting decisively when I build conviction. Temperament is staying disciplined, patient and long-term focused when the stock market is anything but. As I argued in Volatility Isn’t Risk, volatility itself is not the risk - reacting to it is; the stock price drops are a “creator of opportunity”, and the key is not to get scared out of great businesses by a falling quote. Portfolio management is the rest of the craft - sizing positions by conviction, holding to specific buy and sell criteria, and anchoring every decision to an estimate of intrinsic value, investment thesis and signposts. I have a bias toward two kinds of company: dominant platform businesses and skilled capital allocators. The portfolio is 100% equities, concentrated in 5 to 10 large-cap companies, and it is volatile by design. I treat that volatility as the price of admission, as I set out in Why Investing Is Hard, Part 1. When volatility overshoots, I treat it as a chance to buy the dip rather than a reason to flinch, the very flinch I dissect in Why Investing Is Hard, Part 2: The Psychology of Flinching.

My goal is the same one I named on day one of this newsletter: financial independence by 2038 at a portfolio compounding rate above 10%.

There Is A Company Behind Every Stock

Lynch was blunt about why this matters:

“Stocks are not lottery tickets. There’s a company behind every stock. The company does well, the stock does well. It’s not that complicated.”

His complaint was that most people who own stocks can’t say why. Pressed, they admit the real reason: “the sucker’s going up”. He found that absurd - people research a refrigerator, a microwave, a holiday in Europe, then put half their savings into a tip they heard on a bus. The fix is Lynch’s own rule, knowing what I own: there is a company behind every stock, and if the company does well, the stock eventually does too. Coca-Cola earned thirty times more than it had thirty-two years earlier, and the stock rose thirty-fold. Not magic - arithmetic. He also gave permission to ignore the noise:

“Spend fourteen minutes a year on economics and you’ve wasted twelve.”

His point is that trying to forecast interest rates, recessions or where the economy is headed is a waste of effort, because nobody does it reliably and the hours are far better spent understanding the companies I actually own. What I can do is understand a handful of businesses well enough to hold them through the moments that test my nerve. So here is that understanding, holding by holding, heaviest first.

Alphabet (GOOGL) - 25%

What it does: Owns Google Search, YouTube, the Android phone system, and Google Cloud, so most of the questions, videos, ads, and apps moving through the internet pass through something it owns.

Why I own it: Billions use its products by habit, for free, and advertisers pay enormous sums to reach them. It owns the AI stack end-to-end - from its own TPU chips and data-centers, through its Gemini models, up to the billion-plus-user products that distribute them (Search, YouTube, Android, Cloud) - and it earns high returns on the money it reinvests. The core has proved far more resilient than the “AI will kill Search” story implied: even against ChatGPT, Claude and the other AI chatbots, Search keeps growing double digits, with query volume, revenue and profits still rising. On top of that sits real optionality - above all Waymo, whose paid robotaxi rides keep doubling. CEO Sundar Pichai, in charge since 2015, has turned a search company into an AI-and-cloud business without breaking the ad engine that pays for it.

What could go wrong: Antitrust cases, AI chat changing how people search and eroding the ad business, rivals like Meta and Amazon now growing their ad sales faster, and vast data-center spending that has yet to pay off over a cycle.

Amazon.com (AMZN) - 22%

What it does: Two businesses under one roof: the e-commerce marketplace that ships you almost anything, and AWS, the leader in cloud computing, which rents computing power and a plethora of services to much of the web.

Why I own it: E-commerce has the widest selection and the fastest delivery, with a loyalty program (Amazon Prime), high-margin advertising and a third-party marketplace layered on top. AWS is the high-margin engine that funds everything else. CEO Andy Jassy, who built AWS before taking over from Jeff Bezos in 2021, has kept the founder-era habit of reinvesting ahead of profit - and there’s real optionality further out, from the Amazon Leo satellite network to Zoox in robotaxis.

What could go wrong: Thin-margin retail suffers in a weak economy, AWS growth could slow as Microsoft Azure and Google Cloud chase the same customers, and the bill for AI and warehouses is large - ~$200 billion CapEx plan in 2026 - free cash flow stays thin until those investments earn their keep.

MercadoLibre (MELI) - 15%

What it does: The e-commerce and fintech leader of Latin America - the region’s biggest online marketplace, plus a fast-growing payments and digital banking arm in Mercado Pago for people the traditional banks overlooked.

Why I own it: It leads a region moving online and into digital money, and it built both its own delivery network and its own payment rails - two moats at once. It is deliberately spending today, on credit, logistics and lower prices, to own the next decade of growth rather than harvest profit now. Founder Marcos Galperin moved up to Executive Chairman at the start of 2026 and handed the CEO seat to long-time commerce head Ariel Szarfsztejn, so the owner-operator who built it is still steering.

What could go wrong: It lends money, and lending in volatile economies can sour quickly; the macro is genuinely hostile (Argentina’s 32.7% YoY inflation); margins are compressing, possibly the price of defending its lead against Shopee and others across the region.

Brookfield Corporation (BN) - 15%

What it does: Owns and operates real, cash-producing assets for decades - power plants, toll roads, ports, data-centers, property - both on its own balance sheet and with money it manages for big pension funds, for fees. Its insurance arm adds a second engine, investing annuity float into those same real assets.

Why I own it: It’s a compounding machine run by owner-operators: buy hard assets cheaply, improve them, recycle the cash into the next deal, and grow a steady fee-and-insurance business on top. CEO Bruce Flatt, in the seat since 2002 and a large shareholder himself, is exactly the owner-minded capital allocator this thesis rests on. It’s my real-assets anchor, deliberately different from the technology names.

What could go wrong: It uses borrowed money, so high interest rates hurt; its insurance arm has to keep earning a spread on the float it invests; much of its value rests on carried interest it still has to realize over time; and it is a complex group that takes real work to understand.

Uber Technologies (UBER) - 12%

What it does: Runs the app connecting riders to drivers and eaters to restaurants - a toll booth on local movement and delivery in cities worldwide.

Why I own it: It leads most of its markets, and the network feeds itself: more riders pull in more drivers, which shortens waits, which pulls in more riders. Its profitability has been climbing fast since Q2 2022, and the same app sells rides, food, and advertising. It’s the local-commerce royalty in my book - a small cut of an enormous everyday flow. CEO Dara Khosrowshahi, who took over in 2017, is the manager who turned a cash-burning land-grab into a profitable, multi-product platform.

What could go wrong: Robotaxis cut both ways - if Uber can’t field competitive autonomous technology, the AV partners it leans on could route around it; regulators could force it to treat drivers as employees and raise costs; and its heavy reliance on international markets brings currency and political risk on top of growing insurance reserves.

Constellation Software (CSU) - 11%

What it does: Buys lots of small, unglamorous, niche software companies - the kind that quietly runs a single industry’s plumbing, from golf clubs to bus schedules to pharmacies - and holds them forever.

Why I own it: It has turned acquiring these businesses into a repeatable science, earning high returns and reinvesting the cash into the next deals, while each little company keeps customers who can’t easily switch. It’s my “compounding by acquisition” holding. Founder Mark Leonard wrote that playbook and, since stepping back in 2025, handed day-to-day leadership to long-time operator and now-President Mark Miller. Its edge is the discipline and decentralized culture, not any one product.

What could go wrong: The whole engine depends on finding enough good companies at sensible prices, which can get harder with size; its founder is stepping back, testing the bench; and some fear AI could erode old niche software.

Moats and Geographic Reach

Six names is not as narrow as it sounds, because the businesses themselves are globally diversified. Alphabet and Amazon each earn a large share of their revenue outside their home market and sell into almost every economy on earth; Brookfield owns and operates real assets across North America, Europe, South America and Asia-Pacific; Uber runs in thousands of cities across dozens of countries; and Constellation acquires niche software businesses all over the world, with a European engine in Topicus. So the portfolio gets meaningful geographic diversification through what each company does, not through owning more tickers. The deliberate exception is MercadoLibre, concentrated in Latin America - the one place I knowingly take real country-level risk.

What ties the six together is that each owns a structural advantage, not merely a good product: network effects and brand at Alphabet; scale economies and a logistics network at Amazon; regional network dominance at MercadoLibre; capital allocation expertise across cycles at Brookfield; switching costs and a decentralized operating culture at Constellation; and, at Uber, a network effect moat whose strength scales with its lead. I grade these businesses as very high quality.

The Risks I’m Taking

At the portfolio level, concentration amplifies my exposure to sector-wide downturns and to single-company events.

Take concentration first. By the arithmetic it is high - there are currently only six holdings, weighted toward technology-driven platforms. I don’t regard that as the real risk, and I’ve argued why before. Risk, as Graham framed it and as I keep returning to, is the permanent loss of capital, not the size of a position or the wobble of its stock price. A concentrated portfolio, as I put it in my 2025 review, “is a ranking of conviction, renewed over and over again”.

The way I’d actually raise my risk is to dilute that ranking into businesses I understand less well in the name of diversification. When the market handed me the chance, I did the opposite: through the 2025 tariff sell-off I added to my highest-conviction names and let the top three rise from roughly 51% to 59% of the portfolio on purpose. Concentration is the deliberate output of conviction.

Sector risk is the more real version of the same concern: heavy digital-platform exposure means that if technology valuations compress or growth slows, much of the portfolio moves together. Cyclicality is moderate and lives in two places - Brookfield, where economic cycles affect deal flow and asset values, and MercadoLibre, where Latin American currency swings and political instability can cloud earnings visibility even when the operations themselves are performing. On valuation, I’d call it moderate: Alphabet trades at an elevated multiple of operating cash flow (P/OCF) relative to its own history on the strength of growth expectations, while the others I consider underrated against my own estimates of their worth - the cases I’ve laid out holding by holding in earlier articles Regulatory risk is moderate-to-high: Alphabet and Amazon face ongoing antitrust scrutiny, Uber the long-running fight over whether its drivers are contractors or employees, and MercadoLibre regional financial regulation, so policy is something to monitor. Leverage risk is low-to-moderate and concentrated in Brookfield, which uses debt strategically for acquisitions - manageable, but worth watching as interest rates move. Competitive-disruption risk is moderate across the board: rapid innovation can erode any leadership position if the incumbent fails to adapt.

What Ties Them Together

That is my concentrated portfolio, built around high-moat businesses, mostly dominant technology platforms, complemented by one major capital allocator and one serial acquirer, each a leader in its arena, each earning high returns on reinvested capital, each run by people who allocate capital like owners. In other words, every one of these is a compounder - the kind of business, with high returns on capital and a long runway to reinvest them, that I laid out in Compounders: The Key to Long-Term Investment Success.

There is always something to worry about - Lynch rattled off war, depression, Japan, Latin American debt, every fear of his era - and the “key organ in your body in the stock market is your stomach, it’s not the brain”. Declines are not the exception; they are the schedule. When the next one comes, I won’t have to decide what I think in the middle of the panic. I’ll already know what I own.

If you want the source that inspired this article, Peter Lynch’s 1994 talk is worth the 50 minutes.