2025 in Review: From Transformation to Sedimentation

How I kept concentrating into higher-quality compounders while using volatility to upgrade the portfolio

2025 was a weaker year in headline return terms than 2024, but a stronger year in terms of business progress, portfolio quality, and strategic clarity. Measured by money-weighted return (MWRR)1, or IRR, my portfolio returned 5.6% in 2025 (vs 28.2% in 2024).

Because I live in Italy and earn in euros, the euro is the base currency of my portfolio, even though 94% of my investments are denominated in U.S. or Canadian dollars. I record each purchase and sale at its euro value on the transaction date, using the prevailing exchange rate, and then compare that historical euro cost to the current market value translated back into euro. As a result, my reported IRR captures both the performance of the underlying holdings and the effect of currency movements.

In 2025, the euro strengthened against both the U.S. dollar and the Canadian dollar, creating a meaningful headwind for my reported returns.

A stronger euro reduces the euro-denominated value of foreign holdings even when those holdings perform well in local currency. On an FX-neutral basis, excluding that currency effect, my 2025 MWRR was 18.8%, compared with 22.9% for the USD-denominated MSCI All Country World Index (ACWI)2, which I view as the appropriate benchmark for a globally invested portfolio. Put differently, the underlying portfolio performance was materially stronger than the headline euro-denominated figure suggests, even if it still lagged my primary benchmark.

In 2024, I moved away from funds and from positions that no longer fit my framework, restructuring the portfolio around individual businesses I understood better and was willing to own more decisively. In 2025, I reinforced that discipline. The portfolio became less a collection of interesting stocks and more a concentrated group of businesses I believe can compound intrinsic value at high rates over many years. Put differently, 2024 was about transformation; 2025 was about sedimentation.

Portfolio Turnover: Fewer Positions, Higher Conviction

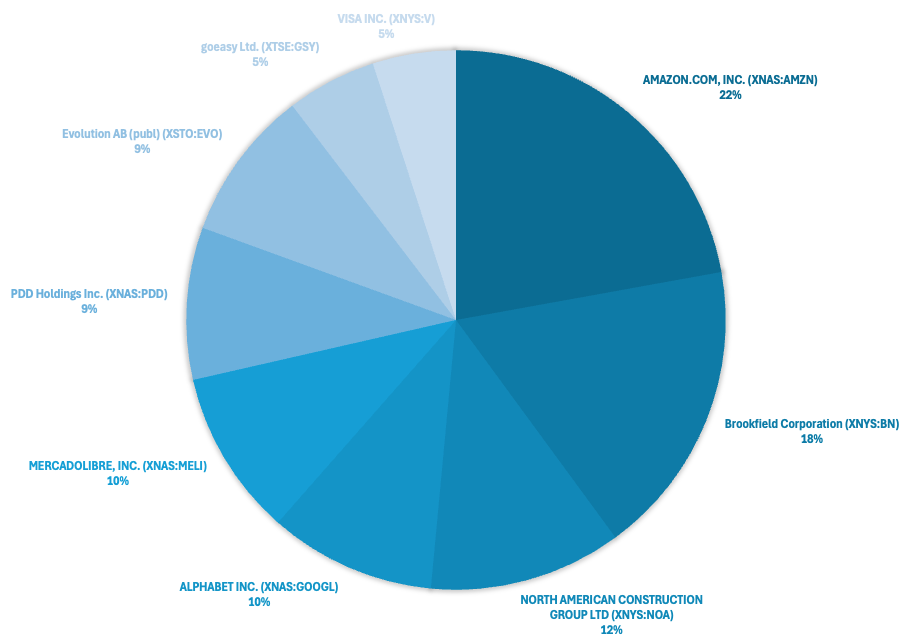

Portfolio turnover in 2025 was meaningful, and it was driven by selectivity rather than activity for its own sake. I began the year with a portfolio spread across nine holdings (Amazon, Brookfield, North American Construction Group, Alphabet, MercadoLibre, Pinduoduo, Evolution AB, goeasy, and Visa).

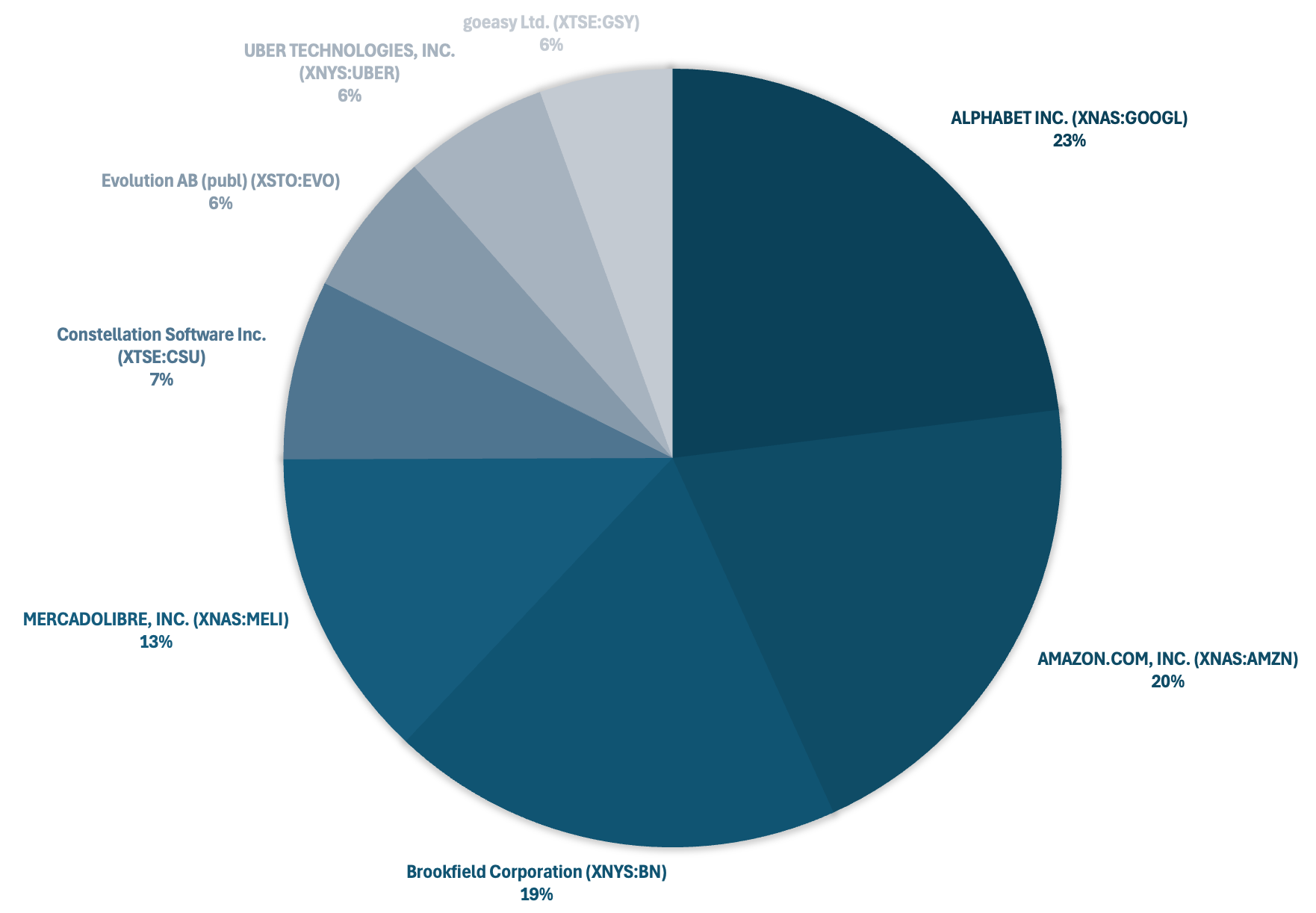

By year-end, the portfolio was concentrated around eight higher-conviction businesses. Alphabet had grown from 10% to become my largest position at 23%, followed by Amazon at 20.2% (vs 22.1%), Brookfield at 18.8% (vs 17.8%), MercadoLibre at 12.9% (vs 9.9%), while new positions in Constellation Software and Uber had grown to 7.5% and 6% respectively.

That shift reflected a deliberate high-grading process. During the year, I exited Visa and North American Construction Group in the March-April selloff to fund higher-conviction businesses, sold Pinduoduo in November for portfolio-quality reasons, and began building positions in Uber and Constellation Software when dislocations gave me attractive entry points. Evolution AB remained in the portfolio at year-end, but at a 3% smaller weight than where it started, before I ultimately exited it in February 2026. goeasy also remained in the portfolio at year-end at a similar weight, before I exited it in March 2026. The result was a portfolio with fewer holdings, larger position sizes in my best ideas, and a clearer tilt toward the businesses I believe offer the best combination of quality, reinvestment runway, and underwriting clarity.

Portfolio Holdings’ Returns

Before turning to the qualitative progress of each business, it is worth looking briefly at how my holdings performed in 2025 on a position-by-position basis. In this section, I show the IRR of each position from December 31, 2024 to December 31, 2025, excluding the effect of foreign exchange, to isolate the underlying investment performance of each holding. Alongside each return, I also show its approximate contribution or detraction to portfolio performance, based on its weight at the start of the year.

I am only showing positions that I held at both the start and the end of the year. That keeps the comparison cleaner and more comparable across holdings, since a full-year IRR is more meaningful when measured over the same time window. Positions that I initiated or exited during the year are better discussed in the sections on portfolio turnover and exited holdings, where the context around timing and capital reallocation matters more than a simple one-year return figure.

Returns show what the stock did over the year, while contribution and detraction show how much that move mattered at the portfolio level. The rest of the article is my attempt to answer the next question: whether the underlying business strengthened, whether intrinsic value likely increased, and whether my conviction became stronger or weaker as a result.

Alphabet Inc. (GOOGL 0.00%↑): 86.8% (+8.68 pp)

Amazon.com Inc. (AMZN 0.00%↑): 9.38% (+2.06 pp)

Brookfield Corp. (BN 0.00%↑): 25.8% (+4.64 pp)

MercadoLibre Inc. (MELI 0.00%↑): 13.1% (+1.31 pp)

Evolution AB (EVO.ST): -22.1% (-1.99 pp)

goeasy Ltd. (GSY.TO): -17.5% (-0.88 pp)

Alphabet (Google): AI Did Not Dilute The Moat; It Widened It

Alphabet Inc. (GOOGL 0.00%↑) had one of the most important years in the portfolio because 2025 moved the debate from theory to evidence. I used the March-April 2025 market selloff, when broad U.S. tariffs sparked a market scare and pushed the stock to a more attractive valuation, to add to my Alphabet position at more attractive prices.

The company delivered strong business performance while showing, more convincingly than ever, that its long-standing advantages in data, distribution, infrastructure, and research can be translated into real AI product and financial momentum. Full-year revenue rose 15.1% to $402.8 billion, operating cash flow increased 31.5% to a record $164.7 billion. Within that, Google Services revenue grew 12.4% to $342.7 billion and Google Cloud revenue rose 35.8% to $58.7 billion, with Cloud profitability continuing to scale meaningfully from 14.1% in 2024 to 23.7% in 2025.

That progress also reinforced the core thesis I laid out in my December 2024 article on Google’s AI leadership: the market was underestimating how well Alphabet’s existing strengths in data, distribution, infrastructure, and research would translate into AI leadership at scale. For years, the market framed AI mainly as a threat to Google Search. In 2025, that narrative started to break down. AI Overviews scaled to more than two billion users across over 200 countries, becoming the most widely used AI product in the world by a wide margin, while helping drive additional query growth, especially among younger users. That matters because it suggests AI is not weakening Google’s core franchise, but reinforcing it. Search remained resilient, YouTube continued to benefit from both advertising and subscriptions momentum, and Cloud became a far more important profit engine than it was when I initiated the position in October 2022.

What stood out most was the combination of research leadership and improving product velocity. DeepMind, which Google acquired more than a decade ago, remains one of the company’s most important strategic assets, and the release of Gemini 3 further strengthened that position. More importantly, Google is getting faster at turning frontier research into live products across Search, YouTube, Cloud, and its broader app ecosystem. In YouTube, multimodal AI is already improving recommendations and creator tools. Across the company, Alphabet increasingly looks less like a collection of products and more like a full-stack AI platform operating across models, consumer surfaces, infrastructure, and monetization.

Google Cloud exited the year at a revenue run-rate above $70 billion, grew 48% in Q4, and reached 23.7% operating margins for the full year, a dramatic improvement from around break-even profitability in mid-2023. I continue to think Google’s full-stack approach is becoming a real differentiator here: proprietary TPUs, leading models, strong infrastructure, and improving scale economics are reinforcing one another. Cloud is no longer just promising optionality; it is now a major engine of value creation in its own right.

Alphabet delivered one of its strongest operating years in recent memory, and my thesis strengthened in 2025: AI did not erode Google’s moat; it widened it.

Amazon: A Full-Stack Platform Built for the Next Cycle

Amazon.com Inc. (AMZN 0.00%↑) was one of the clearest examples in my portfolio of intrinsic value increasing in 2025. I took advantage of the March-April 2025 selloff to add more to my position. At 17.5x operating cash flow (OCF), near the low end of its historical range, the stock looked mispriced for a business that owns two category-defining franchises: AWS, the $140 billion run-rate leading cloud hyperscaler, and Amazon’s unmatched e-commerce platform, supported by a logistics network fulfilling well over $700 billion in GMV annually. My view was that the market was underestimating both the resilience of Amazon’s model and the length of its growth runway.

The numbers were strong, but the bigger story was the shape of the progress. Full-year revenue reached $716.9 billion (+12% YoY), operating cash flow rose to $139.5 billion (+20% YoY), and AWS revenue grew 20% to $128.7 billion. More importantly, AWS growth accelerated from 17% in Q1 to 24% in Q4 despite ongoing capacity constraints, showing that demand remains ahead of supply. Amazon is not spending heavily to create demand; it is spending because demand is already there. I continue to believe AI, especially inference workloads, can materially extend AWS’s runway, and that today’s infrastructure build-out should generate attractive returns over time.

Just as important, Amazon looked increasingly like a full-stack infrastructure and computing company with commerce attached. The company kept investing across cloud, chips, AI tooling, logistics, consumer interfaces, and connectivity. Alexa+, Amazon Leo (“Project Kuiper”), and AWS’s expanding Trainium and Bedrock ecosystem all reinforced that direction. While reported results included some noise from charges and impairments, the broader picture was clear: Amazon was laying more rails for the next decade.

I also continue to think the market undervalues the retail business. It is not just a low-margin merchandise engine, but a scale-driven platform benefiting from logistics density, automation, faster delivery, and a fast-growing, high-margin advertising business. I believe retail margins can move meaningfully higher over time, supported by efficiency gains already visible in the steady decline in per-unit shipping costs.

Put simply, my thesis on Amazon broadened in 2025. This is no longer just a story of strong retail plus AWS, but of an integrated industrial and computing platform with multiple reinforcing engines of value creation. Even after the stock’s appreciation, I still view Amazon as attractively valued relative to the quality of the business and its medium-term earnings power.

Brookfield Corporation: More Levers, More Earnings Power, Same Discipline

Brookfield Corp. (BN 0.00%↑) was another holding where my conviction strengthened in 2025, even if the progress was less flashy than in some of my technology-linked positions. I initiated my position in October 2023 and also took advantage of the March-April 2025 market sell-off to add more shares at attractive prices. That fit well with my broader approach during the year: using dislocations to add to high-quality businesses when the gap between price and intrinsic value widens. Brookfield has long stood out to me as an asset-rich, high-quality company with an exceptional capital allocation record, strong insider alignment, and ownership of assets that sit close to the backbone of the global economy. 2025 made the case clearer rather than more complicated.

In 2025, Brookfield reported total distributable earnings (Brookfield’s own free cash flow metric) of $6 billion for 2025, versus $6.3 billion in 2024, while DE before realizations, the cleaner measure of recurring earning power, rose 10.6% to a record $5.4 billion from $4.9 billion the year before. The company made broad-based progress across all three major engines of the business. Asset Management continued to scale impressively, with fee-bearing capital rising 12% to $603 billion, fee-related earnings up 22% to $3 billion, and fundraising reaching a standout $112 billion, supported by flagship strategies and growing traction in retail and wealth channels. Wealth Solutions also advanced meaningfully, with DE reaching $1.7 billion as annuity sales lifted insurance assets to $143 billion, underwriting profitability improved sharply in P&C, and Brookfield kept redeploying insurance float into higher-yielding Brookfield-managed strategies. Meanwhile, the Operating Businesses remained a solid cash generator, producing $1.6 billion of DE, supported by renewable power, infrastructure, and private equity, while real estate fundamentals improved through stronger occupancy and leasing activity.

What Investor Day reinforced for me is that Brookfield is a compounding platform with several underappreciated growth engines. One important engine is Brookfield Wealth Solutions, where the investment-led insurance model continues to scale and contribute a growing share of DE. More broadly, Brookfield’s current earnings still understate the earnings power embedded in the platform. As funds are monetized and capital is returned to investors, Brookfield should begin recognizing a much larger stream of realized carried interest on its own balance sheet, which is one of the clearest reasons management expects DE growth to accelerate from here. Management is targeting high-teens annual growth in operating DE over the medium term, and when combined with the expected step-up in realized carry, total DE growth could approach 25% annually over the next five years. If Brookfield comes anywhere close to that, the current valuation still looks very attractive despite the stock trading near highs.

Not every business line was equally strong in 2025. Real estate remained softer in places, and some of the headline earnings still masked the underlying progress. But that is also part of why I like Brookfield: it does not rely on one segment, one macro outcome, or one source of value creation. It has multiple levers - asset management, insurance, operating businesses, capital recycling, and balance-sheet opportunism, and they are overseen by managers who have earned a high degree of trust.

Put simply, my thesis on Brookfield became clearer in 2025. This is a business with several embedded growth engines, led by management that has repeatedly shown it can allocate capital well across cycles. Even after the stock’s strong move, I still believe Brookfield offers an attractive combination of quality, valuation support, and long-duration compounding potential.

MercadoLibre: Still Compounding, Still Investing, Still Playing Offense

MercadoLibre Inc. (MELI 0.00%↑) was a clear example in my portfolio of a business still compounding at a remarkable rate while deliberately choosing to reinvest rather than maximize near-term margins. Full-year net revenues and financial income rose 39.1% to $28.9 billion, while operating income increased 21.7% to $3.2 billion despite heavy investment in shipping, fulfillment, cross-border commerce, and newer credit cohorts. The company did not slow down to protect optics. It leaned harder into the opportunity set.

That progress was visible across both of its core engines: Commerce revenue reached $16.3 billion (+34% YoY) and Fintech revenue rose to $12.6 billion (+46.2% YoY), underscoring how balanced and powerful the business has become. GMV grew 26.4% to $65 billion, TPM rose 41.3% to $277.8 billion, and acquiring TPV climbed 32.3% to $188.1 billion. By Q4, net revenues and financial income had accelerated to $8.8 billion, up 44.6% YoY, while management pointed to broad-based strength in Brazil and Mexico, rising buyer frequency, and continued market share gains across the platform. Just as importantly, this was not a one-off spike in growth. MercadoLibre has now delivered 28 consecutive quarters of 30%+ revenue growth, which speaks to how unusual the durability of the business really is.

What gives me the most confidence is that MercadoLibre’s moat is not built around one product, but around the interaction of several. It is the leading e-commerce, payments, credit, and increasingly advertising platform across Latin America, operating in markets that remain under-penetrated and still offer a long runway. Its commerce platform helps bring users and merchants into its financial ecosystem, while its fintech products expand access to payments, credit, and digital banking and, in turn, deepen engagement across commerce. That flywheel is difficult to replicate because competitors tend to be strong in only one layer. A pure e-commerce player does not have the same fintech engine. A pure fintech player does not have the same commerce platform, merchant relationships, logistics footprint, or customer purchase data. MercadoLibre has the full stack.

Scale is a major competitive advantage here. In e-commerce, the first player to achieve real scale in a market often gains durable advantages in logistics density, fulfillment efficiency, merchant breadth, customer trust, and data. Those advantages improve service, lower costs, and make it harder for newer entrants to compete without sacrificing economics. MercadoLibre has the first-mover advantage in Latin America. The stock sold off from its highs partly on renewed competition and macro concerns, but neither of those are new. MercadoLibre has been competing, gaining market share, and operating through volatile political and economic environments for over two decades. Those concerns look more like recurring background noise than a broken thesis.

The apparent margin pressure in 2025 was the result of conscious choices that should strengthen the moat over time: The company effectively traded 5-6 points of operating margin for scale, speed, and deeper fintech penetration. MercadoLibre is still finding plenty of high-return ways to deploy capital across commerce, logistics, payments, and lending. Just as importantly, it did so without compromising the balance sheet, generating roughly $1.48 billion in adjusted free cash flow during the year even while stepping up investment intensity.

2025 also brought an important governance milestone. MercadoLibre announced that founder and CEO Marcos Galperin would become Executive Chairman effective January 1, 2026, with Ariel Szarfsztejn stepping into the CEO role. Founder transitions can expose fragility in a business, but here the change looked orderly and confidence-inspiring. To me, that reinforced the idea that MercadoLibre has evolved beyond founder dependence into a deeper, more institutional compounding machine. The business still has a long runway, management is willing to invest aggressively where returns justify it, and the ecosystem moat across Commerce and Fintech keeps widening. Put simply, my thesis on MercadoLibre strengthened in 2025: this remains one of the highest-quality growth businesses in my portfolio, and one that still looks far from finished.

Constellation Software: A Correction Gave Me The Opening; The System Gave Me Conviction

Constellation Software Inc. (CSU.TO) had been on my watchlist for years, but its quality usually came with a premium valuation. I began building the position in October, during the deepest drawdown in the stock’s history, when AI-driven software panic and succession concerns finally gave me an entry price I found attractive. Part of the correction was understandable given the rich starting valuation (peak 35.8x P/FCF), but the deeper derating struck me as an opportunity rather than a warning.

My thesis was that CSU is best understood as a reinvestment system: resilient vertical-market software (VMS) businesses generating cash, that cash being redeployed into acquisitions, and a culture designed to adapt without breaking. I was not buying a generic software company, but a compounding machine whose edge lies in niche mission-critical products, sticky customer workflows, disciplined capital allocation, and an unusually hard-to-replicate acquisition network.

The full-year 2025 results reinforced that view. Revenue rose 15% to $11.6 billion, operating cash flow increased 24% to $2.7 billion, and free cash flow available to shareholders (FCFA2S) rose 14% to $1.7 billion. Net income was much noisier, falling 30% for the full year to $512 million, largely because of items such as the IRGA/TSS membership liability revaluation and the revaluation of the Asseco investment rather than any break in the underlying operating model. That is exactly why, with Constellation, I pay more attention to revenue, cash generation, acquisition cadence, and reinvestment discipline than to any single year’s reported earnings line.

Just as important, the strategic picture remained intact. Constellation kept deploying capital into acquisitions throughout 2025, and the broader logic of the model did not weaken. CSU operates in the part of software where trust, workflow depth, switching costs, and accountability matter far more than flashy interfaces or short-term AI headlines. AI may make code easier to generate, but it does not make operational consequences easier to bear. That is why I think the market has been too casual in lumping Constellation into a broad “software is dead” narrative. Even management’s own framing has been more measured than alarmist: AI may create some risks around barriers to entry over time, but it may also improve internal efficiency and help portfolio companies build better products faster. At this stage, I still view it as far more likely to be a manageable variable than a thesis-breaking disruption.

The other major development in 2025 was leadership transition. In September, founder Mark Leonard stepped down as President for health reasons and long-time executive and COO Mark Miller took over, a change that understandably unsettled the market. To me, that moment actually highlighted the strength of the model. Constellation was built to outlast any one person. Its real intellectual property is not a single product or centralized strategy deck, but a culture of incentive alignment, decentralized decision-making, acquisition discipline, and capital allocation rigor. The continued strong execution at Topicus, Lumine, and other parts of the broader ecosystem reinforces that point. If anything, fear around succession and AI may prove helpful at the margin by softening valuations across the small software ecosystem and improving future returns on capital deployment. Put simply, my thesis on Constellation strengthened in 2025: this remains one of the highest-quality reinvestment systems in public markets, and the correction gave me the chance to buy it at an attractive price.

Uber: The Platform Thesis Became Harder to Dismiss

I initiated a position in Uber Technologies Inc. (UBER 0.00%↑) in May, taking advantage of a dislocation driven in part by misplaced market fears around autonomous vehicles (AVs). My view was that the market was anchoring to an older version of Uber: a ride-hailing company with fragile economics and uncertain long-term positioning. What I saw instead was a high-quality, capital-light platform with strong network effects, rising engagement, and durable earnings power. Over the course of 2025, that thesis became easier to defend. Uber is increasingly best understood as a “global royalty on movement”: a structurally advantaged platform that clips a small fee on a growing volume of rides, food delivery, groceries, retail, and local logistics without owning most of the underlying physical assets. Since I initiated the position, the stock has actually declined, reflecting the market’s continued skepticism around AVs.

The financial progress in 2025 reinforced my thesis. Trips rose 20.4% to 13.6 billion, gross bookings increased 18.9% to $193.5 billion, and revenue grew 18.3% to $52 billion. More importantly, operating leverage became much more visible: free cash flow climbed to $9.8 billion (+41.6% YoY). By year-end, Uber had 202 million monthly active platform consumers (+18.1% YoY) and was operating at a 15 billion annual trip run-rate. That combination of sustained volume growth, rising engagement, and sharply higher cash generation is exactly what a maturing platform should look like.

The part of the thesis that became more interesting during the year was autonomy. I continue to believe AV commercialization will be more gradual, more geographically constrained, and more partnership-driven than many market participants assume. Regulatory complexity, manufacturing bottlenecks, and the operational burden of deploying physical fleets all argue against a simple winner-take-all outcome. That is why I view Uber less as a business threatened by AVs and more as a beneficiary of them. In 2025, Uber launched Waymo rides exclusively on its app in Austin in March and Atlanta in June, and management said in Q1 that it was already operating at a 1.5 million annual run-rate of AV trips on its network. Uber also said its Austin Waymo vehicles were busier than more than 99% of human drivers in that market, and later noted high utilization in Atlanta as well. Those are important proof points because AV economics depend heavily on utilization, and Uber’s marketplace is built precisely to aggregate demand, reduce idle time, and improve asset productivity.

Just as important, Uber broadened its AV strategy well beyond Waymo. During 2025 it expanded or announced partnerships with a wide range of players, including Baidu, WeRide, Lucid and Nuro. That matters because I do not think the long-term value lies in guessing which AV stack wins everywhere. I think it lies in owning the demand layer, the routing layer, the network density, and the consumer relationship. As AV technology spreads, the value of the driver should diminish while the value of the marketplace should increase. Put simply, Uber looks less like a transportation operator and more like a “global royalty on movement”, with a long runway for both growth and margin expansion.

Exited Positions: Selling to Strengthen The Portfolio

I exited three positions during the year: NOA, V and PDD.

I exited North American Construction Group (NOA 0.00%↑) and Visa (V 0.00%↑) during the March-April selloff to reallocate capital into higher-conviction holdings at attractive prices: Visa sale at a 30% gain was driven by opportunity cost and NOA sale at a 13% loss was driven by deteriorating fundamentals. When the market dislocation created the chance to add aggressively to businesses where my conviction was higher, I chose to simplify the portfolio and move capital accordingly.

The sale of Pinduoduo (PDD 0.00%↑) in November at a 27% gain came from a different, though related, logic. I did not sell because I had turned negative on China. In fact, my broader view on China remained constructive. I sold because I wanted to further raise the quality bar of the portfolio and redeploy the proceeds into businesses I understood better and where my conviction was stronger. Taken together, these exits reflected the same principle that shaped the rest of 2025: a concentrated portfolio should keep evolving toward the businesses I believe are my best long-term capital allocation opportunities.

Exited Positions in Q1 2026

Since the beginning of 2026 I have exited two positions: EVO.ST and GSY.TO.

After Evolution AB (EVO.ST) reported Q4 2025, I exited it in mid-February 2026 at a 37% loss: the thesis that had been weakening for over a year finally fell below my bar for a concentrated holding. The issue was that Evolution’s path to reacceleration was becoming less visible and increasingly dependent on external normalization rather than controllable execution. Consecutive quarters of deteriorating fundamentals, ongoing operational issues, weaker channelization trends in Europe, unresolved cybercrime-related disruption in Asia, and a growing mix shift toward lower-leverage regions all made the investment case harder to underwrite with confidence. By the time I sold, it was clear to me that better alternatives existed elsewhere in the portfolio.

I also exited goeasy Ltd. (GSY.TO) in early March 2026 at a 67% loss after the company admitted that parts of its prior financial reporting could not be relied upon. In its March 10, 2026 operational update, goeasy disclosed a large incremental Q4 2025 charge off, withdrew its prior Q4 outlook and three-year forecast, said prior-period delinquency and staging disclosures would need to be revised, and acknowledged a historical reporting practice at the LendCare subsidiary under which certain customer payments were recorded as received even though they were heavily delinquent and, in some cases, were ultimately not collected. At that point, the investment thesis was broken. What had looked, for decades, like a subprime lender with a long track record of great operational performance became an uninvestable situation marked by damaged trust, unreliable historical numbers, covenant stress, and a far more uncertain path forward. I sold immediately because once confidence in management and in the integrity of the reported financials is gone, there is no place for the stock in a concentrated portfolio.

What 2025 Taught Me

2025 was the year my strategy became clearer. In 2024, I transformed the portfolio by moving away from funds and from positions that no longer fit my process. In 2025, I reinforced that shift by selling two weaker lower-conviction names, exiting another for portfolio-construction reasons, and concentrating further around higher-quality businesses. That is what high-grading the portfolio means in practice: raising the standard for what deserves a place and steadily shaping the portfolio around businesses whose intrinsic value I believe can compound through scale, reinvestment, and strong strategic positioning.

One thing 2025 reinforced for me is that my best decisions often come when the market is most uncomfortable. I learned that lesson years ago during the COVID-19 crash. Back then, I was still investing primarily through diversified funds, and when markets bottomed around March 23, 2020, I did not let the drawdown dictate my emotions. I doubled down. In 2025, during the March-April selloff, I applied that same mindset again. I did not want fear, headlines, or short-term price action to make decisions for me. I wanted volatility to be something I could use, not something I merely endured.

The year also reminded me that market narratives are often less nuanced than the businesses they try to explain. AI was framed as a threat to Google, hyperscaler CapEx was treated as a warning sign for Amazon, AVs were seen as a reason to doubt Uber, and software was dumped into one broad fear bucket that obscured what makes Constellation Software different. In each case, the more useful question was not what the market feared, but whether the underlying business was making real progress in the face of uncertainty.

2025 also reinforced that the strongest moats increasingly sit at the ecosystem level, not the product level. What draws me to businesses like Alphabet, Amazon, MercadoLibre, and Uber is not just that they offer strong products, but that they own broader systems of infrastructure, distribution, data, customer relationships, and adjacent profit pools that reinforce one another. That kind of positioning is harder to disrupt than the market often assumes, and it helps explain why these businesses continue to strengthen even when the narrative around them turns negative.

Another lesson is that portfolio construction is not just about finding attractive ideas. It is about ranking them honestly. Selling PDD while remaining constructive on China made that point very clear to me. A theme can remain intact while a specific stock no longer deserves scarce room in the portfolio. The same applies more broadly: every holding has to compete for capital, and some simply stop clearing the bar.

I was also reminded that capital allocation quality matters more than neat short-term optics. The businesses I grew more confident in during 2025 were not the ones maximizing near-term margins or smoothing reported earnings, but the ones willing to absorb accounting noise, heavier investment, or temporary margin pressure when those choices appeared economically rational. Over time, I care much more about whether management is creating value than whether the quarterly numbers look tidy.

And sometimes, a weakening thesis does not break all at once. It erodes. That was the lesson of Evolution AB. What began as a case for patience eventually became a case for redeployment, as the path to reacceleration became less visible and more dependent on external normalization rather than controllable execution. That is not a comfortable realization, but it is an important one.

If I had to reduce 2025 to one sentence, it would be this: I am becoming less interested in owning what merely looks attractive, and more focused on owning what I can underwrite with conviction through volatility. That shift began in 2024. In 2025, it became more deliberate, and more real.

Final Thoughts

2025 was not my strongest year in reported return terms. It was a meaningful year in a way that matters more to me: the portfolio became clearer, stronger, and more aligned with how I want to invest.

I added more aggressively when the market gave me better prices. I upgraded the portfolio into businesses where my conviction is higher. I sold positions that no longer cleared the bar and I was reminded, again, that volatility is only useful if it helps me own better businesses, not just feel worse while doing nothing.

That is the real progression from 2024 to 2025. Last year, I transformed the portfolio. This year, I clarified what it is supposed to be.

A concentrated portfolio is not a collection of interesting ideas. It is a ranking of conviction, renewed over and over again. In 2025, I raise that standard.

Money-weighted return (MWRR), also known as internal rate of return (IRR), measures the annualized return on a portfolio while accounting for the timing and size of cash flows such as contributions and withdrawals. Unlike time-weighted return (TWRR), it reflects the actual return earned on the capital I had invested, so I use IRR as my primary performance metric.

The MSCI All Country World Index (ACWI) captures large and mid cap representation across Developed Markets (DM) and Emerging Markets (EM) countries. The index covers approximately 85% of the global investable equity opportunity set.