Constellation Software (CSU.TO): AI "Software Is Dead" Headlines, Compounding Still Alive

A framework for underwriting CSU when the market treats software as a single risk bucket

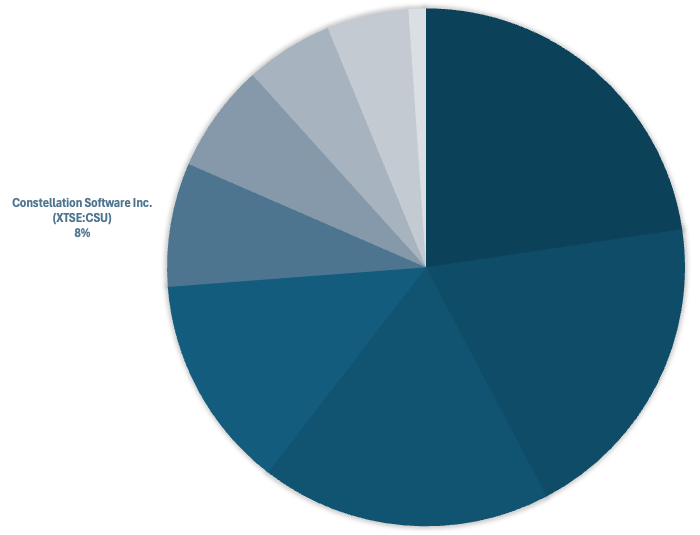

I started building a position in Constellation Software (CSU.TO) in October 2025; it’s now 8% of my portfolio. That size is a bet on a reinvestment system: cash flow turned into more cash flow, repeatedly, without needing perfect forecasts.

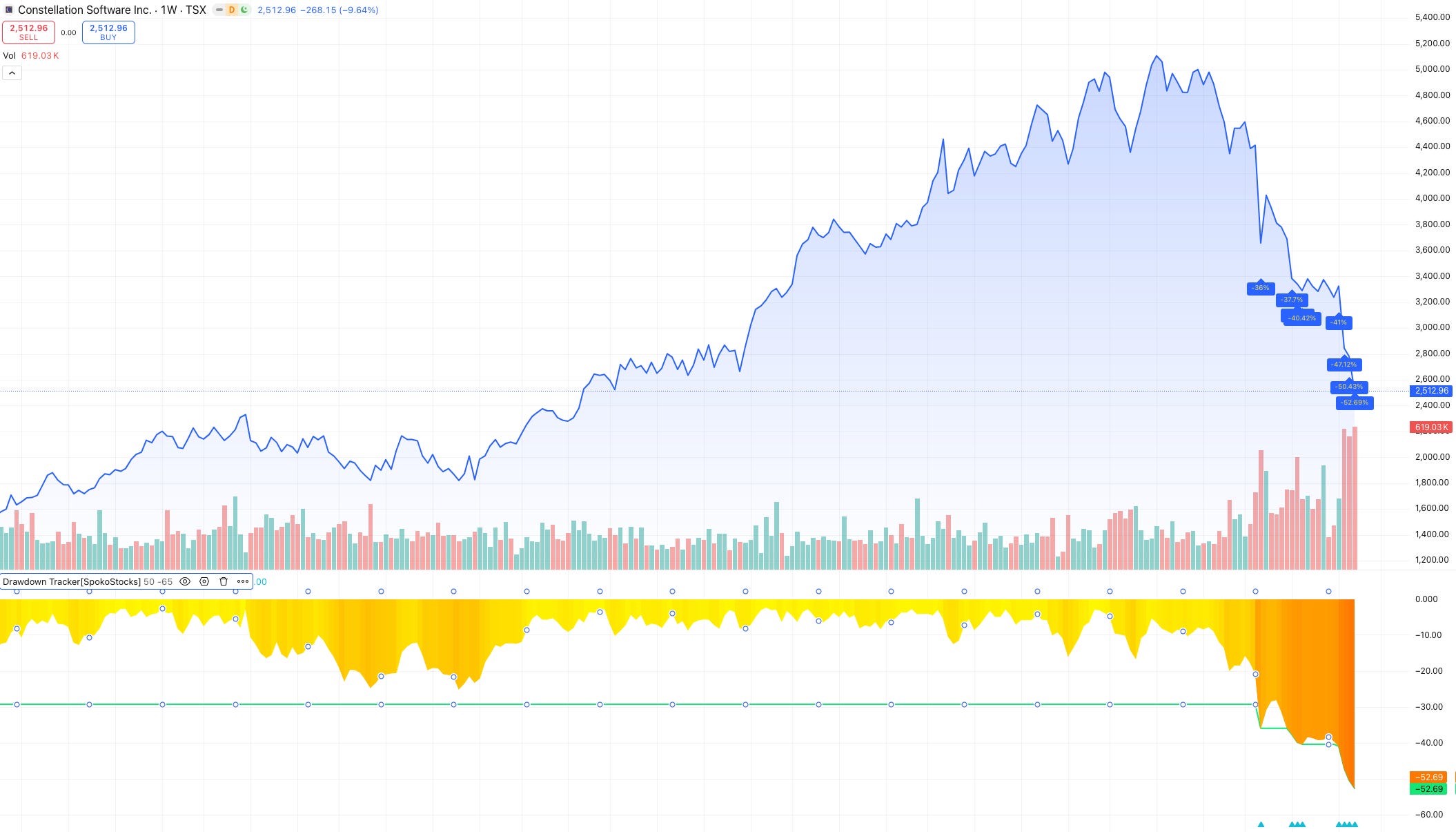

Over the past year, fears that AI will commoditize software triggered indiscriminate selling, as if “software” were a single risk bucket. That misses what CSU actually owns. The irony is that this has been one of the sharpest sentiment drawdowns the stock has experienced, even as the underlying machine has kept compounding. When price and fundamentals diverge this hard, it’s usually not because the business suddenly broke. It’s because narratives moved faster than cash flows.

AI may lower the cost of writing code, but it doesn’t erase operational risk, switching costs, or the decades of workflow knowledge embedded in vertical market software (VMS). The thesis breaks if deal discipline erodes at scale, or if AI turns costs variable faster than CSU can price and route around it.

A Decentralized Reinvestment Flywheel

Most companies face a reinvestment problem: as they scale, high-return opportunities shrink and surplus cash gets misallocated on vanity projects, empire-building, or buybacks done at elevated share prices. Constellation solved that by industrializing reinvestment inside a decentralized structure. The model is simple:

Acquire mission-critical vertical market software (VMS) businesses.

Harvest their steady cash flows.

Reinvest those cash flows into more acquisitions.

Repeat.

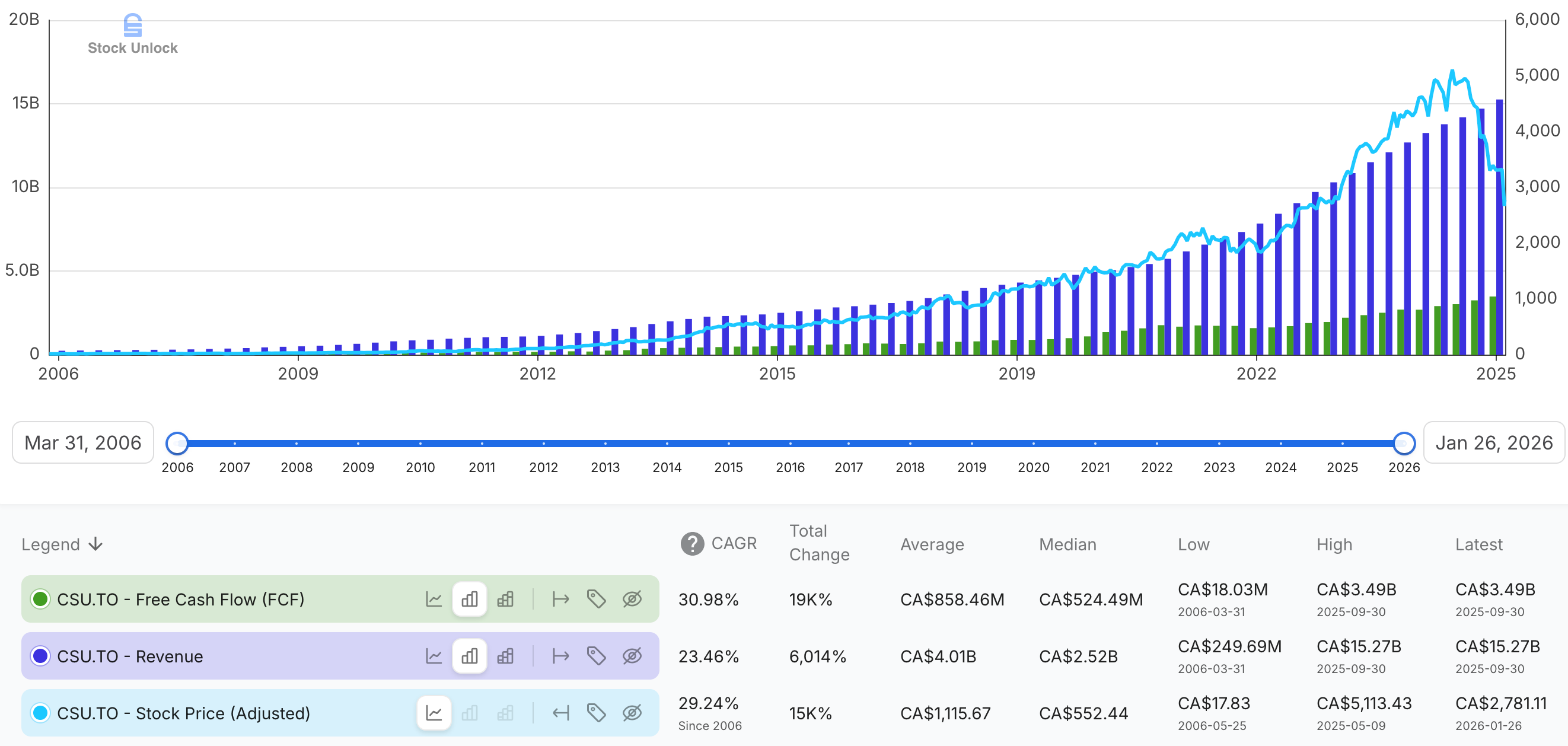

That loop, done with discipline, has produced one of the most exceptional long-term records in public markets: since CSU’s 2006 IPO, it has compounded at 29.3% annually, turning a $10,000 investment into more than $1,600,000 in less than 20 years. CSU has become a textbook example of the serial acquirer model.

The past matters here not because I’m extrapolating a straight line, but because process is the product. CSU’s playbook has been tested across cycles and thousands of acquisition decisions: buy resilient, sticky, cash-generative businesses; stay disciplined on price; avoid “integration” that destroys what made the asset valuable; and fund the next cycle largely from internal cash flow rather than external capital. Because CSU is a perpetual owner, founders can sell without feeling like they’re handing their life’s work to a financial engineer planning to flip it in three years.

There’s another layer that matters just as much as discipline: sourcing. At the holding company level, the business looks easy to copy in theory. Anyone with a checkbook can buy small software companies. In practice, the hard part is distribution in M&A: finding thousands of niche targets, building credibility, and staying top-of-mind for years until a founder is ready to sell. CSU’s edge isn’t that competitors can’t write checks. It’s that CSU has built an acquisition pipeline, a reputation for stewardship, and an operating model that sellers trust.

On September 25, 2025 succession headlines, the market panicked when Mark Leonard stepped down as President and Mark Miller was appointed. Leonard shaped the culture, but CSU was built to outlast any one person. Authority is cascaded down across operating groups and business units. The company’s real intellectual property isn’t the code-base; it’s a culture of aligned incentives, acquisition discipline, and capital allocation rigor. That human-capital moat doesn’t show up neatly on a balance sheet, but it’s the reason the system scales at all.

The Fortress Economics: VMS is Not “Software” in The Generic Sense

To understand why Constellation compounds1, start with what it buys.

Horizontal software can be excellent, but it often sits closer to the surface: generalized tools for broad workflows like CRMs, productivity suites, and collaboration tools, with more direct competition and lower switching friction. Vertical market software (VMS) is different. It’s built for a specific industry - think municipal billing, utilities, dispatch systems, library systems, niche healthcare workflows, other unglamorous back-office or operational systems, with edge cases that only appear after years in production. It’s the difference between software that helps you operate and software you operate through.

The total addressable market is smaller, but the product is embedded and the switching costs are higher. Customers are conservative because failure isn’t an inconvenience; it’s downtime, compliance risk, and career risk. In many verticals, these systems are customized, integrated, implemented, and supported over years. In plenty of cases the “product” includes professional services, onboarding, and ongoing fixes. In some corners, legacy on-premise deployments and entrenched workflows make replacement even more painful. The moat is as much implementation and accountability as it is source code.

These niches also have a structural defense: many are too small to justify venture capital attention. If the prize is modest, rational competitors don’t spend years burning cash for a limited payoff. That’s how CSU ends up owning hundreds of “tiny monopolies” in boring corners of the economy - boring in narrative, excellent in economics.

Many of these businesses are not organic growth machines. Organic growth can be modest because the market is mature and the vendor already dominates it. Pricing may rise gradually and churn is often driven by customer failures rather than competitive losses. The genius is not “these assets grow fast”. The genius is “these assets produce cash reliably”, and CSU has an engine to redeploy that cash into the next purchase.

What Breaks The Thesis

Owning CSU responsibly means being explicit about what can change.

Deal discipline at scale. Scale is a constraint. As CSU grows, it must find larger deals, broaden the opportunity set, or accept lower incremental returns. During an investor update call in mid-September 2025, management has been candid about being “opportunity constrained” and they’ve been equally clear that sitting on cash is not the plan. The risk is straightforward: scale pressure slowly pushes the organization into higher prices, larger checks, or categories with weaker economics, and the return profile of the loop degrades over time. This is also why deal size matters. The historic “bread and butter” has been many small acquisitions. But as free cash flow grows, funding the same pace with only tiny deals becomes harder. One way to extend the runway is occasional larger acquisitions (sometimes supported by measured leverage). That can be rational if hurdle rates hold. It’s dangerous if larger deal size becomes a justification for lower standards.

Low-switching-cost pockets and “graduation risk”. Not every niche is equally mission-critical. CSU has long acknowledged that large, sophisticated customers can leave, sometimes to SAP implementations or proprietary builds. AI increases the stakes because it lowers the perceived friction of “build vs. buy” and can shift the bargaining line over who does customization work. The risk concentrates at the top end and in less critical niches, where switching costs are genuinely lower and buyer sophistication is higher. This is portfolio risk, not an existential one, but it matters if it spreads. Leonard also flagged that some categories are more exposed than others - customer service software, for example, is already seeing more pressure - so the key is not pretending every corner of CSU’s portfolio has identical switching costs.

Variable-cost pressure and centralization creep: AI introduces a new cost structure. Software has historically had high incremental margins; AI can add a usage-based COGS element (model access, compute, inference). Today’s AI usage is heavily subsidized by model providers competing for market share. Over time, those providers may try to recapture that investment through pricing, and vendors like CSU may find a larger slice of their value captured upstream. CSU can route around this, through pricing, model selection, selective on-premise inference, and disciplined productization, but it’s a real economic variable. Separately, AI may require shared infrastructure (security guardrails, common platforms). Some centralization is rational. The execution risk is cultural: if centralization spreads beyond what’s necessary, it can dull the autonomy and accountability that make the system work.

The Trust Moat vs. The AI Scare

“It’s difficult to say whether programming is facing a renaissance or a recession”

— Mark Leonard

The loudest bear case is that AI will let customers code their own software, making CSU’s portfolio obsolete. It sounds plausible until you think about incentives and accountability.

Reliability beats sexiness. Many CSU end-markets are places where probabilistic failure is unacceptable. Utilities, municipal systems, and operational workflows don’t get swapped lightly for “AI-first” tools that might mishandle edge cases. In these niches, trust is the product.

The economics don’t reward switching. For many customers, software is a small line item relative to revenue, often under 1%. Cutting the bill in half often moves margins by basis points, while the downside is asymmetric: downtime, compliance/security exposure, and reputational risk for the buyer. CSU isn’t seeing customers “vibe code” their way out of core systems at scale; most want to run their businesses, not own software maintenance for the next decade.

AI makes code easier to produce, not consequences easier to own. The real question isn’t “can AI write code?” It’s “who is accountable when it breaks?” What’s sticky in VMS isn’t just customer data. It’s decades of accumulated workflow knowledge: business rules, exceptions, integrations, and the lived reality of operations, embedded into systems customers rely on daily. A newcomer can write a cleaner UI. That’s not the same as installing, integrating, servicing, and standing behind a system that runs payroll, billing, dispatch, or compliance.

This is why many VMS businesses settle into tiny monopolies or duopolies with low churn. The threat isn’t that AI can write code. The threat is whether AI can erase switching costs and operational risk. That’s a much higher bar.

How CSU Can Use AI Without Betting The Company

The sensible base case is augmentation. Leonard framed it with intellectual honesty the call by reminding investors how often “replacement” forecasts miss: “Geoff [Hinton] wasn’t wrong […] Where he was wrong was that the technology would replace people. Instead, it’s augmented people”. Applied to software, the honest answer is uncertainty: AI could raise throughput (getting more done with the same teams) dramatically, but it can also raise long-run maintenance costs if it encourages more code, more complexity, and less coherence.

“It’s really easy to get excited about 10x improvements in programmer productivity […] You may end up with higher lifetime cost of the code base. And similarly, you have to take into account the efficiency of the code that the AI produces.”

— Mark Leonard

That’s exactly the kind of second-order thinking I want from a perpetual owner of mission-critical software.

CSU’s operating posture fits its culture. It’s not a centralized moonshot. It’s hundreds of business units testing AI where it’s useful - testing, documentation, internal tooling, selective refactoring - while keeping a tight leash on customer-facing reliability. Management has pointed to concrete areas like better unit testing and security improvements (including vulnerability detection), while acknowledging real constraints: huge legacy code-bases can exceed today’s practical context windows, and “rewrite everything” still leaves you with a system you must maintain.

The adoption path stays conservative because CSU’s customers are conservative. Many prefer their vendor to embed AI into systems that already work, rather than rip-and-replace core infrastructure. The practical playbook is simple and unglamorous: spend time with customers, find high-ROI pain points, and ship changes that reduce regret.

The Opportunity in The Noise: AI Fear Can Feed The Flywheel

One thing I respect about CSU is its temperament. There’s enormous incentive right now for CEOs to sell a sweeping AI story. Reality is messier. CSU’s willingness to say “we don’t know yet” may be bad for a one-day stock move, but it’s the right stance for a perpetual owner trying to compound for decades.

The market is missing a key point: Constellation is a buyer of small software businesses, not a seller of hype. When fear rises - AI fear, succession headlines, generalized “software is dead” narratives - valuations in the small-software ecosystem can soften. That isn’t automatically bad for CSU. It can be fuel. If anxious sellers accept lower multiples, CSU gets to deploy capital at better prospective returns. That aligns with the system: high hurdle rates, low tolerance for overpaying, and a long runway of reinvestment. While the market debates software’s terminal value, CSU can keep buying durable cash flows at prices that improve the math of compounding.

Final Thoughts: Don’t Stop the Snowball

Constellation is a filter for the portfolio. It filters out the temptation to chase whatever is loud this quarter and forces attention back to what actually compounds: mission-critical systems, entrenched workflows, and cash flows reinvested with discipline.

At an 8% weighting, my conviction isn’t that CSU will never change. It will. My conviction is that the system is built to adapt without breaking: resilient niche businesses throwing off cash, that cash funding more acquisitions, and a culture designed to preserve what makes the acquired businesses valuable.

If the market wants to treat software as one undifferentiated AI loser, fine. CSU lives in the part of software where trust is the product and switching is the risk. When that gets mispriced, volatility isn’t a signal to panic. It’s the market offering a better entry point into a compounding machine.

Compounding is the process where returns earned in one period are reinvested and generate additional returns in future periods, so growth builds on top of prior growth (returns on returns). See also my earlier piece on compounders.

AI not erasing operational risk is a crucial insight. Thanks.

https://canadiancapitalcompounder.substack.com/p/who-am-i-and-my-400000-bet-on-constellation?r=8pnzfk&utm_campaign=post&utm_medium=web

Fat Pitch, Bucket not the thimble, whatever you want to call it, these opportunities are rare, and when they come, it is worth swinging big.