MercadoLibre (MELI): Two Decades of Compounding, A Year of Doubt - Part 1: The Bear Case

Five reasons the LatAm compounder may be in structural trouble: competition, credit, macro, regulation, valuation. The opening installment of a three-part series

MercadoLibre, Inc. (MELI 0.00%↑) posted its fastest revenue growth in four years in Q1 2026 (+49% YoY) and the stock fell 13% on the day, extending a 40% twelve-month drawdown. The bear case is that competition (Shopee, Amazon, TikTok Shop) is permanently resetting the margin structure, that the credit book is growing into a cycle no one has tested it through, and that ROIC has halved from a 34% peak in mid-2024 to 16.7% TTM at Q1 2026. The bull case is that the margin compression is deliberate reinvestment into a logistics network the incoming CEO calls “more developed than Amazon’s”, that the fintech flywheel is a structural arbitrage between regulated bank funding costs and under-banked-borrower demand, and that my estimate of owner’s earnings of ~$6.1 billion annualized puts the company at 13x on an ~$80 billion market cap. The three signposts that will resolve the debate are Brazil unit shipping cost (currently -17% YoY and accelerating), credit card 15-90 day NPL direction (currently improving), and NIMAL stabilization above 15% (currently 17.8%, trending down). I have been adding to the position on weakness and intend to continue.

“Invert, always invert: Turn a situation or problem upside down. Look at it backwards. What happens if all our plans go wrong? Where don’t we want to go, and how do you get there?”

— Charlie Munger, former vice-chairman, Berkshire Hathaway

When a company posts the fastest revenue growth in four years and the stock falls 13% on the day of the announcement, the analytical exercise has to run in both directions. Charlie Munger’s framework, borrowed from the 19th century mathematician Carl Gustav Jacob Jacobi, is the right one: don’t just build the case for owning the stock; build the case against owning it as forcefully as you can, then look at the same disclosure through both lenses and see what survives.

How This Series Is Structured

That is the exercise I am running across three parts of this series. Doing it well requires more space than a single article can hold, so I have split the work into three pieces published over the next weeks:

Part 1 (this article) lays out the bear case against MercadoLibre in five pillars: structural margin pressure, credit book risk, macro and geopolitical exposure, tax and regulatory asymmetry, and a valuation that leaves no cushion for any of those concerns to play out.

Part 2 lays out the bull case in five pillars: strategic margin compression as deliberate moat construction, the data-driven fintech flywheel, ecosystem lock-in beyond commerce, the merchant flywheel, and a valuation that is more attractive than the headline numbers suggest.

Part 3 brings both sides together - where the bear and bull cases actually disagree, the three signposts that will resolve the debate, and where I land on the stock.

For the underlying “who captures the surplus” framing that informs how I read the bear/bull trade-off, see my Q1 2026 results article.

The Business Context

MercadoLibre has earned the label “the Amazon of Latin America”, but that shorthand is too narrow. The business is an ecosystem spanning e-commerce, logistics, payments, credit, advertising, and subscriptions. The Q4 2025 results delivered $8.8 billion of consolidated revenue (+45% YoY) and full-year 2025 revenue growth of 39%. The Q1 2026 results escalated the same dynamic in both directions: revenue accelerated to +49% YoY (the fastest pace since Q2 2022) while operating margin compressed to 6.9% (down from 10.1% in Q4 2025). The stock is down ~40% over twelve months.

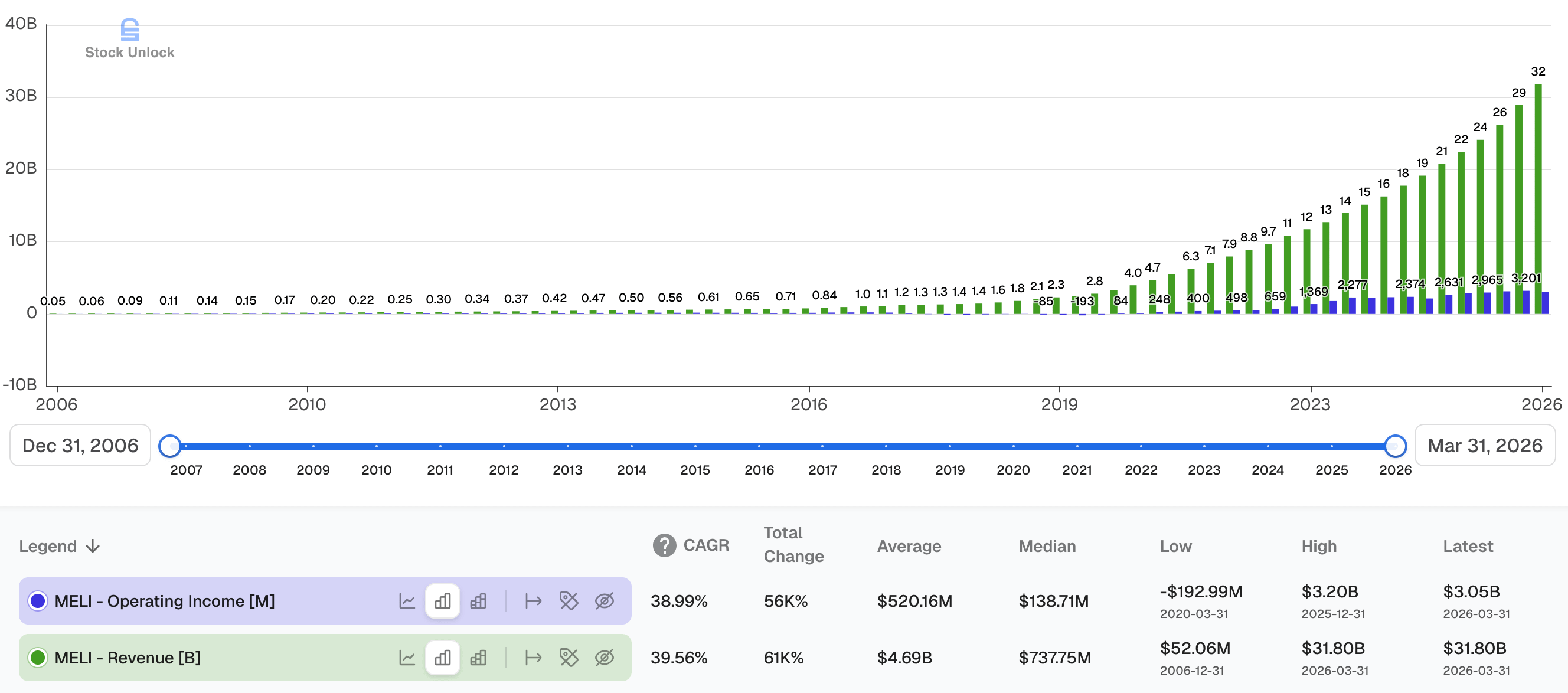

The current debate sits inside a much longer track record. MELI has compounded revenue at a 39.6% CAGR for nineteen consecutive years - from $52.1 million in 2006 to $31.8 billion TTM at Q1 2026, a 610x increase. Operating income compounded at a similar 39% CAGR over the same window, from $5.4 million to $3.05 billion TTM, and along the way it has been through two distinct investment cycles that briefly took it negative, the 2018-2020 Mercado Envíos buildout was the deeper one, before recovering to new highs each time. The Q4 2025 operating income peak of $3.2 billion was the most recent high; Q1 2026’s $3.05 billion is the slight dip that the rest of this series is about.

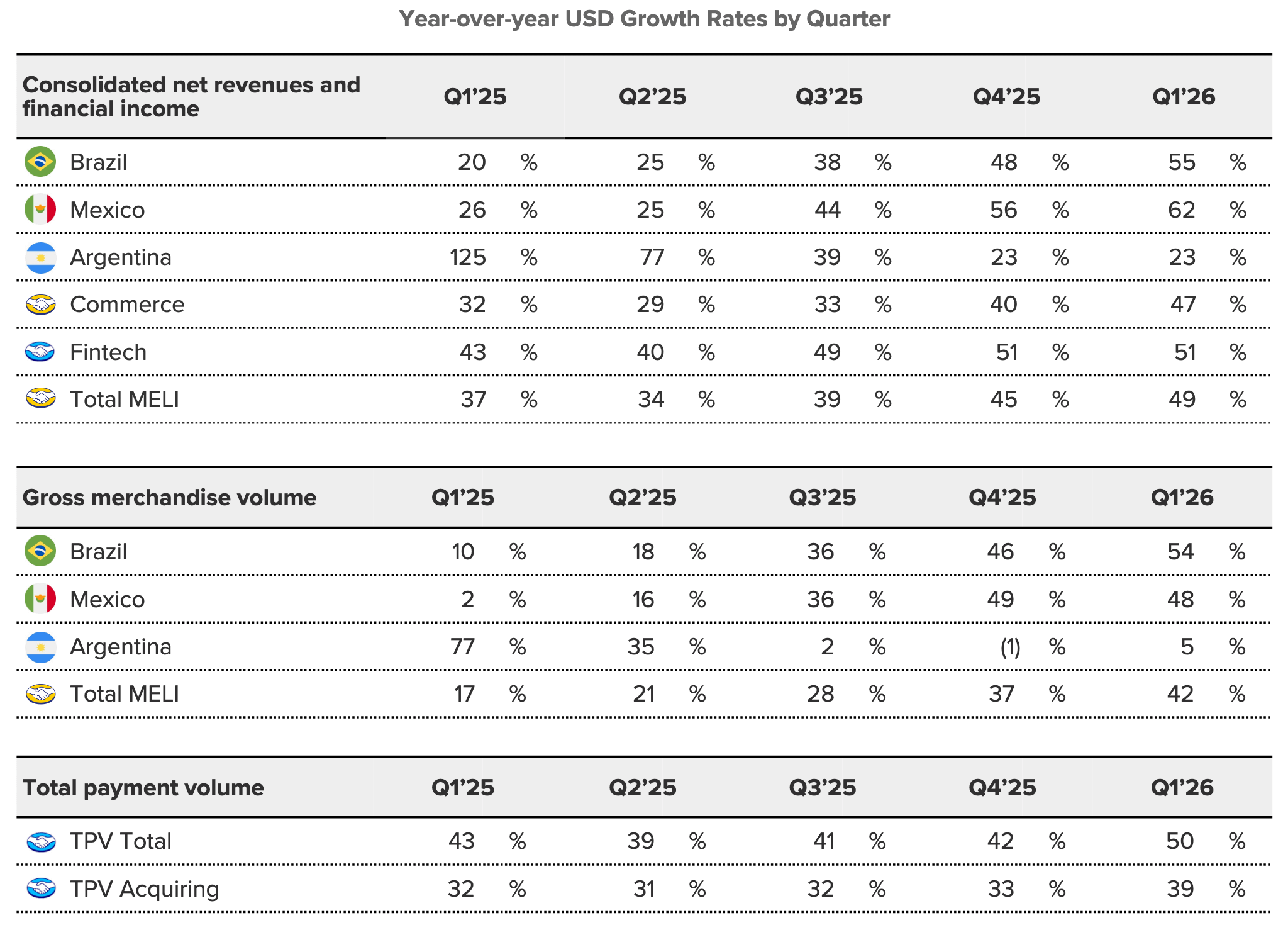

The growth side of that story is structural and broad-based. Both segments (commerce and fintech) and both major markets (Brazil and Mexico) have accelerated for five consecutive quarters:

The investment debate is whether today’s investments are defensive spending to protect the franchise or offensive spending to widen it, and whether the operating margin compression that has accompanied the revenue acceleration is the cost of standing still or the cost of widening the moat.

The Bear Case in Five Pillars

The bear case is that what management calls “investing” is increasingly indistinguishable from “defending”. Competition has intensified across every layer of MELI’s stack at the same time the credit book has grown into a meaningful share of the business, and the operating margin compression since Q4 2024 may be the price of standing still rather than the cost of widening the moat. The five pillars below build the case in sequence: structural margin pressure, credit book risk, macro and geopolitical exposure, tax and regulatory asymmetry, and a valuation that leaves no cushion for any of those concerns to play out.

Margins From 13% to 7% And Maybe There’s No Coming Back

MELI’s operating margin has fallen from 12-14% range a couple of years ago to 6.9% in Q1 2026, the lowest since 2022, and 9.6% Last Twelve Months (LTM). Operating income declined 19.9% YoY to $611 million; provisions for doubtful accounts more than doubled YoY to $1.24 billion and alone drove 3.9% of the 6% of YoY margin compression. Gross margin fell 3% to 43.7% as the lower Brazil free shipping threshold (R$79 → R$19) and faster 1P (first-party, where MELI buys inventory and resells) scaling weighed.

The culprit is competition, and it is not transient. Shopee did not exist as a Brazilian retailer before 2019. Today it leads Brazil by order volume and has been profitable for several quarters on an adjusted EBITDA basis. Shopee has also raised its Brazilian take-rate from the 0-5% range it used to seed the platform to ~15%, broadly aligned with MELI today, which removes the implicit “we are more expensive than Shopee, so they cannot threaten our high-end” defense. Amazon launched Amazon Now (15-minute grocery delivery) in Brazil with Rappi in March 2026 and partnered with Nubank in November 2025 to integrate NuPay installment financing, two areas where MELI has historically differentiated itself. TikTok Shop launched in Brazil in May 2025, with Banco Santander projecting it could reach ~9% of Brazilian e-commerce by 2028.

The Innovator’s Dilemma Trap

There is also a strategic dimension to MELI's response to competition. Clayton Christensen’s standard prescription for an incumbent facing a low-end disrupter is to vacate the contested segment and move upmarket where margin still exists; defending the low end is the move textbook strategy says ends in margin erosion you cannot recover from. MELI did the opposite when it cut the Brazil free shipping threshold from R$79 to R$19: it chose to fight in Shopee’s profit pool rather than concede it, on the reasonable theory that letting Shopee habituate the Brazilian consumer would have built a foothold inside MELI’s customer base. That may be the right strategic call, but the bear point is that the choice itself - competing in a structurally lower-margin tier MELI did not need to be in - locks in a permanently different unit economics profile from the pre-2024 era, regardless of how well execution goes from here.

No One Is Making Money in Brazilian E-Commerce

In addition, there is a real argument that no participant is actually making sustainable economic profit in Brazilian e-commerce - Shopee’s Brazil profit doesn’t include a share of head-office costs - only direct Brazil expenses are counted, Amazon’s Brazil P&L is opaque, and MELI’s own Brazil margins have stepped down materially as Shopee scaled into a credible #2 in the market.

Brazil direct contribution (DC) margin fell from 17.6% in Q1 2025 to 8.2% in Q1 2026, with absolute quarterly DC dollars declining 28% YoY from $542 million to $389 million even as revenue grew 55% to $4.8 billion. DC is MELI’s segment-level profitability measure (country revenue minus local operating expenses and depreciation, before any allocation of corporate or shared costs) which means the deterioration is in country-level unit economics, not in how MELI assigns headquarters overhead. On a TTM basis through Q1 2026, Brazil DC margin sits at 11.4%, less than half its 2023 peak near 25%.

Amazon’s Restraint Is Doing the Heavy Lifting

There is a deeper structural concern: the only thing keeping the Brazilian and Mexican margin environment from being meaningfully worse for MELI is that Amazon has chosen not to compete harder. Amazon’s South America CapEx is rationed against AWS, North American retail, and other higher-ROI uses globally - Amazon’s $200 billion 2026 CapEx budget overwhelmingly funds AWS and domestic robotics, not LatAm fulfillment. If that ranking ever reorders, Amazon could plausibly commit $20 billion of capital to Mexico and Brazil and stay there for a decade, the way it has stayed in losing businesses elsewhere when it wanted to. The probability of that reordering is not high, and the MELI marketplace’s margin structure currently rests on the assumption that Amazon’s internal capital-allocation discipline holds. The bull case has no answer to this beyond pointing out that the assumption has held for two decades.

Were Pre-Competition Margins Structural, Or Just the Spoils of No Rivals?

The bear’s question is fair: were MELI’s pre-competition margins a function of structural advantages, or the spoils of operating without serious rivals? If the latter, margin compression is permanent. On the Q1 2026 shareholders letter, CFO Martin de Los Santos went further than ever before:

“We have the ability to dial margins up or down as circumstances and opportunities evolve – Q1’26 reflects where we have chosen to set the dial, and we do not anticipate this changing materially in the near term.”

Q2 2026 faces an additional headwind: targeted Brazilian seller take-rate reductions implemented late in Q1 will hit Q2 P&L for the first time.

Read more sharply, the dial framing is itself half true: management may choose how aggressively to invest above the floor in any quarter, but competition (Shopee on low-ASP, Amazon on premium fulfillment, TikTok Shop on discovery, Nubank on deposit economics) increasingly sets the floor itself. The 6.9% Q1 2026 operating margin is therefore “discretionary” only above the minimum the competitive system already imposes.

Mercado Ads Cuts the Other Way in a Downturn

There is a related vulnerability: Mercado Ads is a high-margin profit pool in MELI’s stack and one of the strongest single data points in the bull case (+73% YoY in Q1 2026). The 10-K explicitly flags that “if we are unable to compete effectively for advertising spend, or if our merchants reduce advertising spend, our business and results of operations could be materially harmed”. Ad budgets are among the first line items merchants cut in a downturn, and MELI’s advertisers are largely the same LatAm small and medium businesses (SMBs) whose credit quality and consumer demand the bear case is already questioning. If a Brazilian or Mexican recession hits, the advertising profit pool compresses while credit losses rise while take-rates are absorbing seller incentives, three margin pressures stacking at once on a 6.9% operating margin base.

The bear summary: MELI is fighting a two-front war: Shopee on low-ASP (Average Selling Price) volume and Amazon on premium fulfillment + financing, while investing into a third front (discovery shopping) to contrast TikTok Shop, and the margin structure may never return to what it once was.

The Credit Book No One Has Seen Through a Recession

Mercado Pago has extended credit at a breathtaking pace. The portfolio reached $12.5 billion (+90% YoY) in Q4 2025 and accelerated to $14.6 billion (+87% YoY) in Q1 2026, the largest nominal quarterly increase ever. Credit card mix has shifted up to 46% of the credit portfolio, from 42% in Q1 2025; Brazil consumer loan duration was deliberately extended from 5 to 8 months. Net Interest Margin After Losses (NIMAL)1 fell sharply to 17.8% in Q1 2026, from 23.3% in Q4 2025, a 5.5% step-down in risk-adjusted lending profitability.

CECL: How Fast Growth Distorts the P&L

An accounting point cuts in both directions and is worth flagging. Under CECL (Current Expected Credit Loss)2 accounting, a lender is required to recognize the entire lifetime expected loss of a loan at the moment of origination, not over the years the loan actually lives. When a book is growing +87% YoY, a non-trivial share of the provisions step-up (+106.3% YoY to $1.24 billion in Q1 2026) is the mechanical front-loading of expected losses on loans that have not yet defaulted, not deterioration in the underwriting model. That is the bull-friendly reading of the line item. The bear-friendly reading is the mirror image: if book growth ever slows, the provision line will mechanically improve and create a one-time margin pop that is not really a sustainable improvement in unit economics. Both readings are correct; the practical implication is that the +106.3% YoY provisions number cannot be read at face value in either direction, and a non-trivial portion of the operating margin compression the bear case notes is artifact rather than signal.

LatAm has some of the highest consumer non-performing loan (NPL) rates in the world (per World Bank Group). The Q4 2025 shareholders letter notes “less than 20% of Mexicans and only 40% of Argentines have a credit card” - the greenfield opportunity bulls cite, but also the risk of extending credit into populations traditional institutions have avoided. Legendary investor Howard Marks has written repeatedly about a recurring pattern in credit markets: when new lending products grow faster than the underwriting models that govern them, defaults tend to surprise on the downside when the cycle turns. In his April 2026 memo What’s Going on in Private Credit?, he describes managers who “accepted too much money and invested it too fast, applying standards that were too low and setting the scene for a correction”. The bear concern about MELI’s credit book is a variation on the same theme: credit book growth (+87% YoY) is running ahead of the period over which any new underwriting model can be properly tested.

We will not know the true quality of this credit book until it faces a recession or significant macro shock. If credit defaults spike materially, the market may re-rate MELI not as a growth compounder but as a consumer lender in frontier markets, and banks command very different price multiples from leading aggregators. Net debt / adjusted EBITDA rose to 1.46x in Q1 2026, from 0.83x in Q1 2025, still investment-grade but a meaningful change in the corporate financial profile.

Off-Balance-Sheet Commitments and Interchange Risk

The headline credit portfolio number also understates the true exposure: the Q1 2026 10-Q discloses $11.9 billion of off-balance-sheet unused agreed loan commitment on the credit card portfolio at March 31, 2026, up from $9 billion at year-end 2025, a 32.2% step-up in three months in credit lines MELI has extended but not yet drawn. The reported credit book grew 87% YoY; the committed credit footprint is growing faster still.

The credit card economics are also exposed to a layer of regulation outside MELI’s control. The 2025 10-K flags reliance on “banks and investment funds that acquire Mercado Pago’s receivables and payment processors to fund transactions, and changes to card association fees, rules or practices”. Visa and Mastercard interchange rates have been actively contested in Brazil and Mexico - the Brazilian Central Bank has periodically pressed for lower interchange caps, and any 0.5%+ reduction would compress the credit card unit economics that underpin part of the bull case at exactly the moment the credit card mix is highest (46% of the credit book in Q1 2026, up from 42% YoY). The credit card business has gone from a small option-value layer to “as pivotal for Mercado Pago as the launch of our managed logistics network was for our marketplace ten years ago”, MELI’s own framing in the Q1 2026 shareholders letter, which means interchange regulation has gone from a peripheral risk to a central one.

Mercado Pago is the #2 consumer fintech in Brazil - the company does not publish a Brazil-specific MAU figure, so I estimate Brazilian users in the 50 million range against Nubank’s reported 135 million - Nubank has the household name, the longer onboarding head start, and ~60% of Brazilian adults as account holders. The bull case for fintech leans heavily on the cross-sell and acquiring angles where MELI's ecosystem advantages compound; that is the right argument, but it should not obscure that on raw consumer-fintech’s market share, MELI is competing from behind in the market that contributes roughly half of consolidated revenue.

Pix: The Slow Squeeze on Payment Take-Rates

Pix, the Brazilian Central Bank’s instant payments system launched in November 2020, is the second regulatory force eroding the payment layer of Mercado Pago’s economics. Pix transactions are free for consumers and very low-cost for merchants. It has scaled to roughly 80 billion transactions a year by 2025, accounting for more than half of all payment transactions in Brazil. Mercado Pago’s response - like that of every other Brazilian fintech - has been to build value-added services on top of Pix rather than compete on the payment itself, which is the right strategic choice and is also an admission that the payment processing take-rate on Brazilian transactions is on a long, slow path toward zero. The bull case rests on the value-added layer (credit, AUM, ads, ecosystem cross-sell) capturing the surplus that the payment fee no longer can; the bear reading is that this is a treadmill where every basis point of payment fee compression has to be recaptured elsewhere, which sets a structural ceiling on the unit economics of the Brazilian fintech business that did not exist six years ago. Mexico has not yet launched a Pix equivalent at scale, but the Brazilian template is the obvious regulatory blueprint other LatAm central banks will study.

Credit Is Not Logistics

There is a hidden assumption in the bull-side framing of credit that is worth naming: that the “density compounds” mechanic that makes logistics get cheaper at scale also applies to credit. It does not. Logistics improves with scale almost automatically - more packages spread fixed costs, route density improves, the marginal package gets cheaper than the average. Credit improves only if underwriting accuracy, funding costs, repayment behavior, and cohort seasoning improve faster than provisions burn through the P&L. That is not the same compounding mechanism; it is a much higher burden of proof, and the +87% YoY credit book growth raises the burden rather than lowering it.

Becoming a Regulated Bank Cuts Both Ways

One more layer worth flagging: the banking licenses Mercado Pago has applied for in Mexico (filed September 2024) and Argentina (announced May 2025) cut both ways. A full bank-charter unlocks deposit funding and a broader product set, which Part 2 develops as a bull-side ambition. The bear-side concession the bull case has to make is that bank regulation introduces Basel-style capital adequacy requirements3 that Mercado Pago does not currently carry on its loan book, and that is a meaningful change from the present regulatory posture. To be precise, Mercado Pago is already a regulator-supervised entity in every country it operates in (an authorized Payment Institution in Brazil since 2018, an IFPE in Mexico, e-money issuer in Chile, payment institution in Argentina and Uruguay), and per Note 3 of the Q1 2026 10-Q it already holds $11.5 billion of restricted cash at central banks across the region to back user wallet balances. That is segregated-customer-funds regulation, not risk-weighted-asset capital against the loan book; the two are different regimes that apply to different parts of the balance sheet. Today, the structural arbitrage argument the bull case relies on depends partly on the fact that Mercado Pago’s lending activity is not bound by the same risk-weighted-asset framework that gives Itaú a 6.1% net interest margin on its credit book. The moment Mercado Pago becomes a regulated bank in Mexico and Argentina, that lending-side exemption disappears on those balance sheets - meaning the very NIMAL the bull case anchors on may compress because the regulator forces MELI to hold real equity capital against the credit book. There is also a price multiple dimension: a regulated bank with deposit-taking and Basel capital ratios is, optically, easier for the market to compare against Itaú or Bradesco than against a platform compounder, which is the precise re-rating concern the credit book section above already flagged. The bank-charter strategy is rationally defensible, and Nubank has already proven the path to a full bank in Brazil, but it accelerates the bear case the moment when MELI has to defend itself as a bank rather than as a fintech.

Macro and Geopolitical Risk Is Not Theoretical

MELI lost its entire Venezuelan operations in 2017 and took a $85.8 million write-down due to political instability. That is a reminder that the markets MELI operates in are not merely volatile, they can be existential. Brazil, Argentina, and Mexico each carry unique risks. Argentina has lurched between currency crises, peso devaluations, and capital controls for most of two decades.

The Q1 2026 10-Q makes the Argentine exposure concrete. Argentina’s average inter-annual inflation rate is at 32.7%. The Argentine peso’s average exchange rate against the USD weakened 34.1% YoY in the quarter, which mechanically explains why Argentina’s reported USD revenue growth of +22.9% looks weaker than the underlying local currency business. In addition, $342 million of MELI cash sits restricted at the Argentine Central Bank as a mandatory guarantee; liquidity that cannot be freely deployed elsewhere in the business. Currency depreciation erodes the USD value of locally-reported earnings; high inflation distorts revenue figures, complicates credit underwriting, and erodes consumer purchasing power all at once.

In fairness to the bulls, this is the bear point MELI has chosen to address head-on in its investor materials:

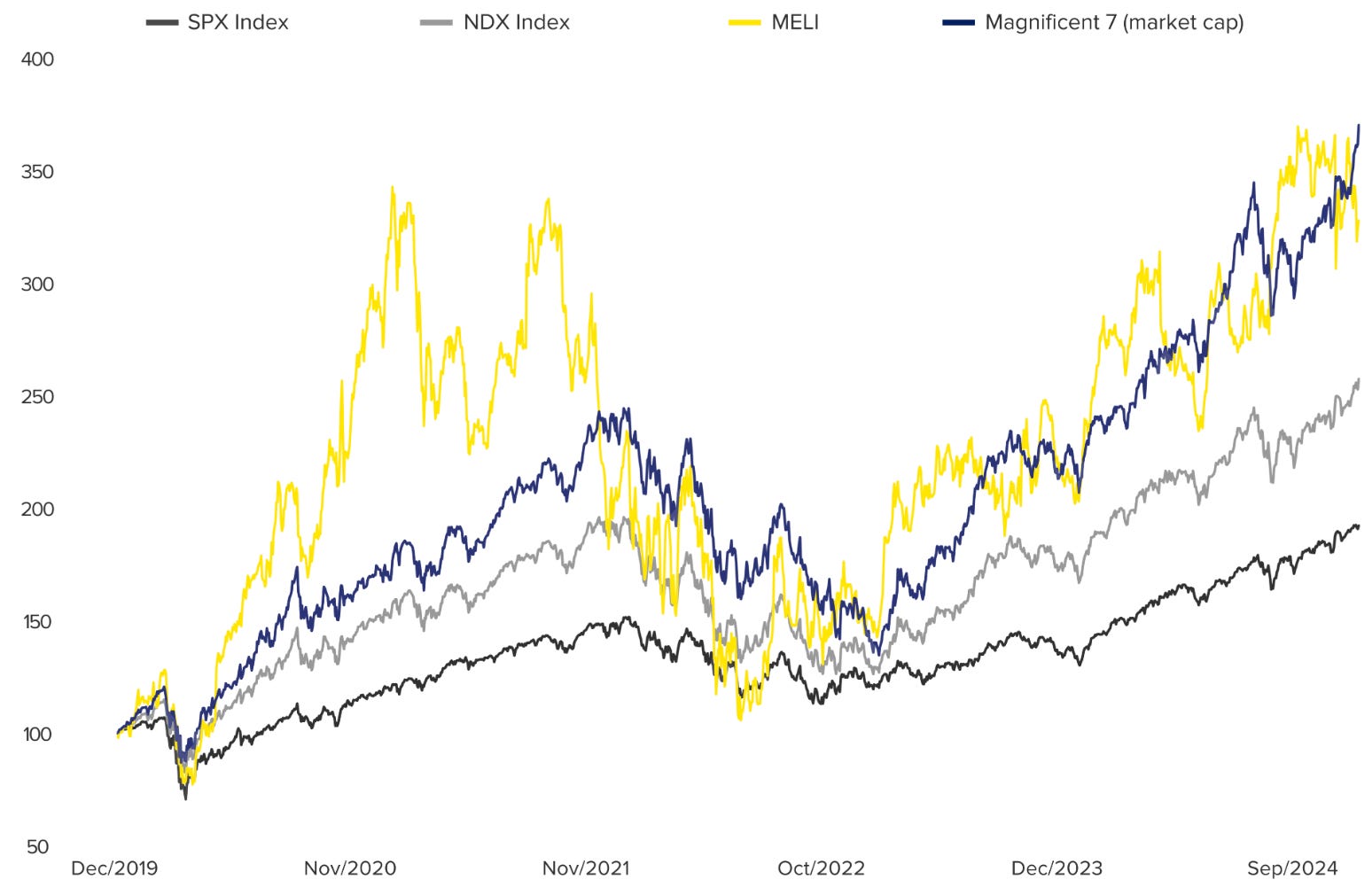

Between 2019 and 2024, MELI shareholders have earned a total return similar to that of the Magnificent 7, through a period that included an Argentine sovereign debt restructuring, the steepest peso devaluation in modern history, Brazilian rate cycles oscillating between 2% and 13.8%, a Mexican election cycle, and the global rate normalization. The bear point on FX and macro is real and the 10-Q numbers above are not in dispute. The historical answer is that MELI has compounded fast enough to overwhelm the FX drag, which is the company’s own response to the question of whether the LatAm-FX bear case is a reason to discount the business rather than a permanent reality to live with.

Regulation Cuts Both Ways, Mostly Against MELI

A subtle bear point sits in the tax and regulatory disclosures themselves. The Q1 2026 effective tax rate fell from 30% YoY to 27.9%, with management noting that this benefit came from a Brazil income tax reform passed on December 26, 2025 that increases deferred tax assets in Q1 2026 and incrementally raises the cash tax rate beginning in April 2026. Q1 helped the P&L; Q2 onward will hurt it. Provision for contingencies stepped up from $23 million Q1 2025 to $39 million Q1 2026 (+70% YoY), small in absolute terms but a leading indicator of regulatory and legal friction increasing across MELI’s jurisdictions.

The 2025 10-K is also direct about a structural disadvantage: MELI’s Mercado Libre and Mercado Pago mobile apps depend on distribution through Apple’s App Store and Google Play, “typically subject to commissions ranging from 15% to 30% of the transaction value”, with anti-steering restrictions and limited access to NFC functionality for tap-to-pay. MELI itself flags that this “may also place us at a competitive disadvantage in connection with digital ecosystems that are vertically integrated and do not incur similar distribution or payment processing fees” - the very competitors (Apple Pay, Google Pay, and adjacent platforms) that MELI competes against in fintech do not pay the toll MELI does. Recent EU and Brazilian enforcement actions may erode that asymmetry over time, but the timing and magnitude are not in MELI’s control.

In fairness, regulation cuts both ways and not every regulatory move runs against MELI. A recent Brazilian rule change shifted the tax collection obligation in e-commerce from the seller registration layer to the transaction layer, meaning marketplaces are now responsible for remitting tax at the point of sale rather than relying on sellers to be registered businesses and self-report. MELI is largely unaffected because its sellers already operate under registered business numbers (CNPJ) and were paying tax under the prior regime; the rule materially hits competitors that allowed individual, unregistered sellers - most notably Shopee, where a meaningful share of the Brazilian seller base appears to have been on the platform precisely because of the lighter tax treatment. The point is not that regulation is on MELI’s side, it is not, as the tax reform and app-store-fee discussion above shows, but that the regulatory environment is asymmetric in both directions, and MELI’s compliance-heavy operating model occasionally turns into a competitive edge when the rules tighten on lower-compliance entrants.

ROIC Has Halved in Seven Quarters. The Multiple Hasn’t

GAAP earnings are distorted by one-time items, and heavy reinvestment that obscures true cash generation. Reported adjusted free cash flow was -$56 million in Q1 2026, seasonally negative and dominated by the $1.95 billion step-up in loans receivable. With margins compressed and the credit book absorbing capital, the current 57x price-to-LTM adjusted FCF (P/AFCF) multiple demands an optimistic set of assumptions. For a business simultaneously navigating competitive pressure, credit cycle risk, and geopolitical volatility, paying a full price leaves very little room for error.

The deeper concern under the headline price multiple is return on invested capital (ROIC)4. The shape of the curve is unambiguous:

MELI’s ROIC has compressed from a 34% peak in Q2 2024 to 16.7% TTM at Q1 2026, less than half the peak and the fifth consecutive quarterly step-down. The denominator is rising for two reasons: the credit book has grown +87% YoY and absorbs balance sheet capital, and the logistics and fulfillment buildout (over $1.3 billion of CapEx in 2025, up from $860 million in 2024) is expanding the asset base ahead of the operating leverage it is meant to produce. The bull thesis - that density compounds in logistics and the data flywheel compounds in fintech - has to show up as a re-acceleration of ROIC eventually. So far it has not; the line keeps stepping down. This is the metric that ultimately decides whether the reinvestment is creating value or just rebuilding the moat at par. The current cycle is also wider in scope than any prior reinvestment phase in MELI’s history: the credit book expansion, 1P scaling, logistics buildout, and AI productivity reinvestment are all happening simultaneously on a much larger asset base than in any earlier cycle, in a region with materially intensified competition. If ROIC keeps stepping down toward the average of 12.5% as the credit book continues to grow and CapEx remains elevated, the “reinvestment is value-creating” argument has to be re-underwritten on weaker terms regardless of how strong the operating margin recovery turns out to be.

There is also a quieter assumption embedded in any owner’s earnings valuation (which I develop in Part 2) that deserves to be flagged on the bear side: the multiple implicitly assumes the investment intensity moderates at some point in the foreseeable future, freeing the cash flow that the multiple is being applied to. The simultaneous 1P/logistics/credit cycle currently underway does not look like a program that is about to wind down. If the reinvestment cycle extends another two or three years rather than one, the cash flow positive valuation snapshot the multiple is anchored to keeps sliding into the future, and the multiple effectively re-rates without the stock having to move.

Coming Next: The Bull Case

Each of the five bear points above is real and worth respecting. None of them is a strawman, and none of them dissolves under scrutiny. Each also has a bull-side counter that reads the same data differently. Part 2 of this series builds the bull case in five pillars: strategic margin compression as deliberate moat construction, the data-driven fintech flywheel, ecosystem lock-in beyond commerce, the merchant flywheel most bears overlook, and a valuation that is more attractive than the headline numbers suggest.

Net Interest Margin After Losses (NIMAL) is MELI’s measure of the spread between credit revenues and the combined cost of provisions for doubtful accounts and funding, expressed as a percentage of the average loan portfolio. It is structurally lower for credit cards (because the full expected lifetime loss must be provisioned up-front when each card is issued) and improves as cohorts season.

Current Expected Credit Loss (CECL) is the US accounting standard, in force since 2020, that governs how lenders recognize loan losses on the income statement. Under the prior “incurred loss” model, a lender booked a provision only when a specific loan showed evidence of impairment, which tended to lag the actual credit cycle. CECL replaced that with a forward-looking model: at the moment a loan is originated, the lender must estimate the entire expected loss over the life of the loan, using historical loss data, current conditions, and reasonable forecasts, and book that full lifetime expected loss as a provision immediately. The mechanical consequence is that a fast-growing loan book generates an outsized provision expense even if underwriting quality is stable or improving, because every newly originated loan brings its full lifetime loss reserve with it on day one. Short-duration loans soften this effect (less lifetime to reserve for); credit cards amplify it.

Basel-style capital adequacy requirements are the international banking-regulation standards that govern how much equity capital a regulated bank must hold against the loans and other assets on its balance sheet. The mechanic is risk-weighted: each asset is assigned a risk weight based on borrower creditworthiness and loan type - a mortgage to a prime borrower might carry a 35% risk weight, an unsecured loan to a thin-file consumer 100% or more - and the bank must hold 8-13% of those risk-weighted assets as Common Equity Tier 1 (CET1) capital, plus additional buffers for systemically important institutions. The constraint is binding: a bank cannot keep growing its loan book once it bumps into its CET1 ratio without either retaining more earnings, issuing new shares, or shedding assets. For a fintech transitioning to a full bank charter, the practical consequence is that the same loan that earned a wide spread on a payment-institution balance sheet (where no such capital charge applies) now consumes shareholder equity at the regulated rate, which is why traditional LatAm banks like Itaú clear narrower net interest margins than Mercado Pago does today on the same kind of borrower.

Return On Invested Capital (ROIC) measures how much after-tax operating profit a business generates per dollar of capital invested in the business. The standard formula is ROIC = NOPAT / Invested Capital, where NOPAT (net operating profit after tax) is operating income multiplied by (1 minus the effective tax rate) and Invested Capital is total equity (book value) plus interest-bearing debt minus cash and cash equivalents. The intuition is simple: a business that earns $15 of after-tax operating profit on $100 of capital deployed (15% ROIC) is creating more shareholder value per dollar reinvested than one that earns $5 (5% ROIC). ROIC consistently above the company’s cost of capital (typically 8-10% for a mature business) is the signature of a business that should reinvest aggressively. ROIC trending down toward or below the cost of capital is the signature of a business that is destroying value through reinvestment, regardless of how fast revenue is growing.

Well written. Thanks for so clearly articulating the bear case. Much appreciated.