MercadoLibre (MELI): Two Decades of Compounding, A Year of Doubt - Part 2: The Bull Case

Five reasons the same data tells the opposite story: the Amazon playbook in real time, a structural fintech arbitrage, and a moat the market is currently extrapolating against. Part 2 of three

This is the second article of a three parts series. In Part 1, I built the bear case against MercadoLibre, Inc. (MELI 0.00%↑) in five pillars: margins compressing under three-front competition, a credit book growing into a cycle no one has tested it through, macro and geopolitical exposure that is not theoretical, tax and regulatory asymmetry, and a valuation that leaves no cushion for any of those concerns to play out. Each of those bear points is real and worth respecting.

In this part, I lay out the bull case. The bull case is not that the bear’s data is wrong, it is that the same data reads differently when you frame it as deliberate capital deployment rather than deterioration. In Part 3, I bring both sides together, cover the three signposts that will resolve the debate, and share where I land.

The Bull Case in Five Pillars

The bull case rejects the framing that margin compression equals deterioration. It sees the same data and reads it as deliberate capital deployment - the Amazon playbook running in real time, with a fintech flywheel layered on top that no public market competitor has been able to replicate in the region. The five pillars below build the case in sequence: strategic margin compression, the data-driven fintech flywheel, ecosystem lock-in beyond commerce, the merchant flywheel, and a valuation that is more attractive than the headline numbers suggest.

Lower Margins Now to Widen the Moat Later

The bear sees falling margins as deterioration. The bull sees deliberate capital deployment, the playbook that made Amazon one of the great value-creation machines of the modern era.

The Amazon Playbook in Numbers

Amazon’s North America segment is the textbook case: Operating margin compressed from 4.1% in 2019 to a trough of -0.9% in 2022 as the company doubled its fulfillment footprint, expanded Prime, and absorbed pandemic-era overbuild. As that investment cycle matured, the margin profile that emerged was dramatically higher and more durable: 4.2% in 2023, 6.4% in 2024, 6.9% in 2025, and 7.9% in Q1 2026, nearly doubling the pre-pandemic level on a vastly larger revenue base ($104 billion in Q1 2026 vs $53.7 billion in Q4 2019). MELI is executing the same strategy.

It is worth stepping back and naming a fact the debate over a single quarter’s margin tends to obscure: over the two decades Amazon has been expanding internationally, three companies in the world have competed against it head-to-head in retail and won market share leadership in their home region - Coupang (CPNG 0.00%↑) in South Korea, JD.com (JD 0.00%↑) in China, and MercadoLibre in LatAm. Every other competitor that attempted has been bought, marginalized, or pushed into bankruptcy. This is not a quantitative argument; it is an observation about management and execution quality that should anchor how the rest of the bull case is read.

MercadoLibre is consciously trading near-term profits for stronger long-term economics. In the Q4 2025 letter, the company wrote:

“Free shipping has been one of the most important pillars of our value proposition for a decade […] The impact on behavior is clear.”

Those are not the words of a company reacting in panic. Free shipping at scale does three things at once: it retains existing customers who might otherwise defect to Shopee, increases purchasing frequency among loyal users, and spreads fixed logistics costs across a growing volume base, structurally lowering per-unit cost. Volume and efficiency compound in a way that favors the incumbent with the biggest network.

Brazil Cohort Data: The Flywheel in Real Time

The Q1 2026 results provided the cleanest single quarter of evidence yet. Nine months after the Brazil free shipping threshold cut, marketplace cohort behavior is still strengthening:

Brazil items sold +56% YoY, up from +45% Q4 2025, +42% Q3 2025, +26% Q2 2025; “volume growth has doubled in nine months”.

Brazil unique buyer growth +32% YoY, fastest in five years.

Brazil conversion rate +1% YoY, large for a marketplace at MELI’s scale.

Brazil unit shipping cost -17% YoY in local currency, accelerating from -11% Q4 2025, even while absorbing 56% volume growth - scale is improving logistics economics.

Same/next-day shipments 199 million (+39% YoY), accelerating from +29% Q4 2025.

CFO Martin de Los Santos summarized:

“In other words, higher demand is driving lower costs.”

That is the flywheel working in real time. Lower margins now to widen the moat later. Q1 2026 was the first full quarter with Ariel Szarfsztejn as CEO following Marcos Galperin’s transition to Executive Chairman on January 1, 2026 - a strong opening quarter for a new chief executive, and a signal that the deliberate margin compression strategy was endorsed by both the outgoing founder and the incoming operator. At Scottish Mortgage’s Change Drives Growth digital conference in October 2025, just weeks after his appointment was announced, incoming CEO Szarfsztejn framed the moment this way:

“We are in the best moment of our 26 years of life, growing at startup rates while generating value, gaining market share across every single market in e-commerce, and growing triple digits in fintech […] We are doing amazingly well, but the opportunity forward is huge.”

That is the bull case framing in the operator’s own words: growth “while generating value”, market share gains “in every single market”, and a runway that is still ahead. It is exactly the disposition you would want from a CEO about to spend a year compressing margins to widen the moat.

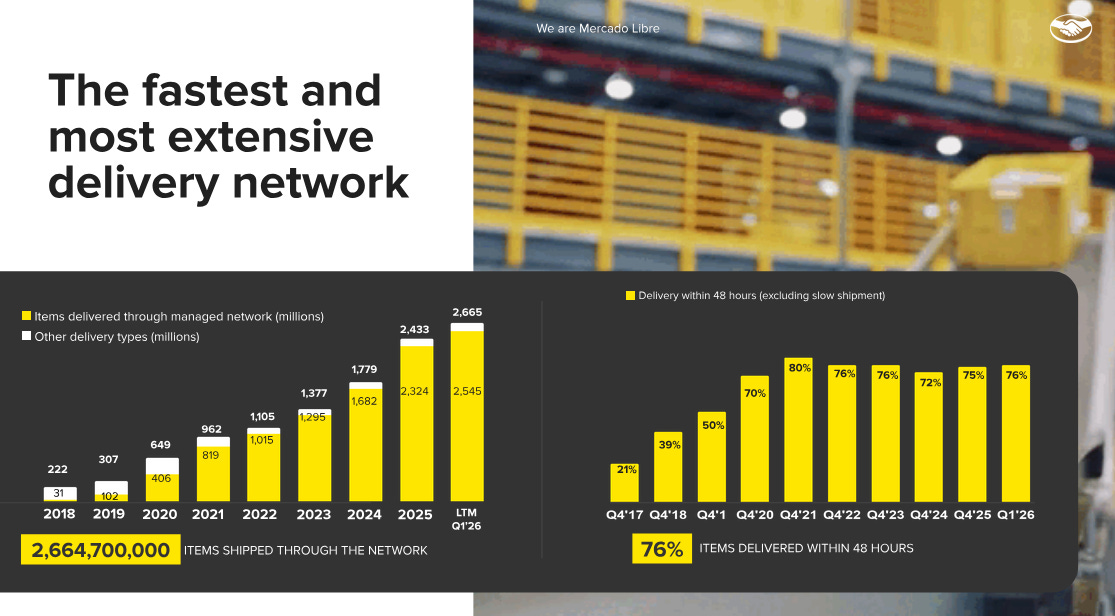

The Logistics Moat: 12x Volume in Seven Years

What makes the “density compounds” argument credible is that this is not a thesis MELI is just starting to test. It is a ten-year operating track record, and one that the incoming CEO led. Szarfsztejn described his own arrival at the company in 2017:

“One of the first things that I realized after I joined was that we needed to develop our logistics arm […] At the time we were 60 people that were reporting to me, and that was the whole logistics team for MercadoLibre. For you to have an idea, today we are like 70,000 people, it’s seven years later.”

Items shipped through the network grew from 222 million in 2018 to 2.67 billion over the TTM ending Q1 2026, a 12x increase in a little over seven years. The share moving through MELI’s managed network (rather than third-party carriers) has risen from 7.2% in 2018 to 95.5% today. Same-day or 48-hour delivery has stepped up from 21% in Q4 2017 to 76% in Q1 2026. The footprint to do this is now over 50 fulfillment centers region-wide as of Q1 2026, up from 30+ in Q2 2025 and roughly 3x Amazon’s combined Brazil + Mexico fulfillment-center footprint (Amazon does not disclose its LatAm fulfillment-center count, but industry estimates put Amazon Brazil in the low-double-digit range and Amazon Mexico at fewer than 10 facilities). This is the physical asset base behind the bull case: 2.7 billion packages a year creates the routing density, fulfillment utilization, and line-haul scale that no LatAm competitor can replicate without spending the better part of a decade and tens of billions of dollars. Shopee leans on third-party carriers and its own SPX Express network in Brazil only; Amazon is building its own LatAm network but is years behind; TikTok Shop has no logistics layer at all. This is the first-mover moat that matters: every package MELI moves makes the next one cheaper, and competitors have to catch up to a moving target while subsidizing their way through unprofitable volumes.

The first-mover advantage is not just being early, it is the compounding of years of network density. The 17% YoY unit cost reduction in Brazil during Q1 2026 is what density compounding looks like in a single data point. The 12x volume increase since 2018 is what it looks like over a cycle. Szarfsztejn made the comparative claim explicitly in the same interview:

“It might be hard to understand for somebody coming from the UK or the US, but our logistics infrastructure today is more developed than Amazon’s logistics infrastructure. So we are operating probably more efficient. We are definitely faster. We are definitely more reliable, and that really gave us a boost in terms of competitive positioning.”

That is a strong claim made on the record by an incoming CEO to a major institutional shareholder. The bear case has to either argue Szarfsztejn is wrong on his own home turf, or accept that MELI’s LatAm logistics network is the deepest first-mover moat in the region.

The architecture behind the claim is worth making concrete because it is the technical reason MELI’s network is hard to copy, not just an executive boast. Amazon’s US logistics is a hub-and-spoke1 system: large fulfillment centers feed a smaller number of regional sortation stations which then distribute outward. That topology works in a market with dense, well-paved last-mile infrastructure. LatAm does not have that. MELI built its managed-logistics arm, branded Mercado Envíos, on a different topology: a mesh of more than 100 cross-docking facilities2 that allow packages to be re-sorted multiple times across regional routes (sellers can also drop merchandise directly into these facilities, bypassing the fulfillment center step entirely), feeding into a network of more than 10,000 Mercado Envíos Places, local convenience stores, pharmacies, and mom-and-pop shops that double as pickup and drop-off points for end customers. Two things make this architecturally superior to a hub-and-spoke system in LatAm specifically. First, theft of unattended doorstep deliveries is structurally higher in the region than in the US and Europe, so customer demand for staffed pickup points is real, not a workaround. Second, the mesh topology routes around the unevenness of last-mile road infrastructure in a way that hub-and-spoke does not. The moat is not the warehouses, it is the 10,000+ pickup points and the 100+ cross-docking nodes that connect them. That is what “more developed than Amazon’s” refers to.

Why Shopee’s Order Volume Lead Doesn’t Translate to GMV

The Shopee threat is also worth re-examining at this point, because the bear case #1 framing - Shopee has more orders in Brazil than MELI - is true but ignores the shape of the competition. Shopee’s order volume leadership comes from the same compulsive purchase, low-ASP (Average Selling Price), gamified-shopping model that disrupted essential commerce in China and Southeast Asia and that Wish, Temu, and AliExpress have all tried to extend into developed markets. The structural ceiling on that model is consumer attrition: cheap, novelty, impulse-driven items disappoint a meaningful share of the time, and consumers who get burned a few times exit the platform for higher-trust alternatives when they want something they actually need. Shopee has skillfully localized its Brazilian seller base, which has lifted the average experience, but the high-intent, essential commerce segment has stayed largely with MELI and Amazon. The order volume number and the GMV number are diverging in Brazil for a reason, and the reason is structural rather than transient.

1P vs 3P: An Accounting Optics Issue, Not a Margin Issue

One mechanical point on the 1P scaling that bear case flags as a gross margin headwind: 1P (first-party, where MELI buys inventory and resells) and 3P (third-party marketplace) economics tend to converge over time once you account for all three profit pools that a transaction generates. On a 3P sale, MELI captures a commission take-rate, a logistics fee, and an advertising attach; on a 1P sale, MELI captures a procurement spread, the same logistics fee, and a similar advertising attach. The accounting looks different - 1P revenue grosses up the top line at the full transaction value while 3P only books the commission - which is why mixing more 1P into the revenue line mechanically compresses the headline gross margin. On the operating margin per dollar of GMV, the two unit economics are roughly equivalent once equilibrium sets in, and the 1P motion gives MELI category-level pricing control in segments where 3P sellers were not aggressive enough on procurement. The bear case framing of “faster 1P scaling weighed on gross margin” is true on the line item; the implied conclusion that the underlying economics deteriorated does not follow.

Cross-Border Trade: Going on Offense Against the Same Asian Sellers Powering Shopee

The bull-side story on free shipping and density is largely defensive: keep low-ASP volume inside the MELI ecosystem rather than ceding it to Shopee, Temu, and the rest of the cross-border discount stack. Cross-border trade (CBT) is the one place where MELI is going on offense against those same Asian supply bases. The Q4 2025 shareholders letter framed it directly:

“Cross-border trade (CBT) is one of our strategic initiatives that gained momentum in 2025 as we ramped up investment. In LatinAmerica, CBT is a c.$10bn market where we have a small share and a large opportunity to expand assortment […] growth accelerated through the year, resulting in 74% FX-neutral GMV growth in Q4’25”

Q1 2026 sustained the trajectory, with management writing in the Q1 2026 shareholders letter that “we have an unmatched competitive advantage to offer to merchants in China and the USA: we are the largest ecommerce platform in the world’s fastest-growing region by sales”. The geographic spread is widening from the original Mexico foothold, per the same Q1 2026 letter:

“Momentum has also spread beyond Mexico, our primary CBT market, with Argentina and the Andean countries contributing more meaningfully to growth. In markets such as Colombia and Peru where the local seller base is not as deep as it is in our largest markets, CBT directly expands the assortment available to buyers.”

The strategic point is that the global cross-border supply base that Shopee and Temu have been pulling LatAm consumers toward is one that MELI can now route through its own marketplace and managed delivery network. The competitive position is asymmetric: Shopee runs cross-border without a domestic logistics arm in most LatAm markets it serves cross-border, while MELI’s Mercado Envíos network already operates on the ground in the destination country. As Chinese sellers migrate from drop-shipping into MELI’s domestic fulfillment via the CBT funnel, what was a competitive threat (Asian supply chasing LatAm demand) becomes a growth lever inside MELI’s own ecosystem. MELI opened its first fulfillment center in China in 2025 to deepen those merchant relationships, signaling that CBT is now treated as core infrastructure rather than a side experiment.

The Fintech Flywheel Is a Real Competitive Advantage

The most powerful aspect of MELI’s business is the integration of Mercado Pago with the marketplace. MercadoLibre writes in the business overview of their SEC filings (10-K and 10-Q):

“Facilitating credit is a key service overlay that enables us to further strengthen the engagement and lock-in rate of our users.”

Credit as Retention, Monetization, and Data

Credit is not an adjacent product, it is a retention tool, a monetization tool, and a data engine. Management made the same point in the Q4 2025 shareholders letter:

“Data from repeated interactions with our ecosystem feeds into our underwriting models. As a result, we have millions of pre-approved users who are offered credit at the marketplace checkout (and elsewhere).”

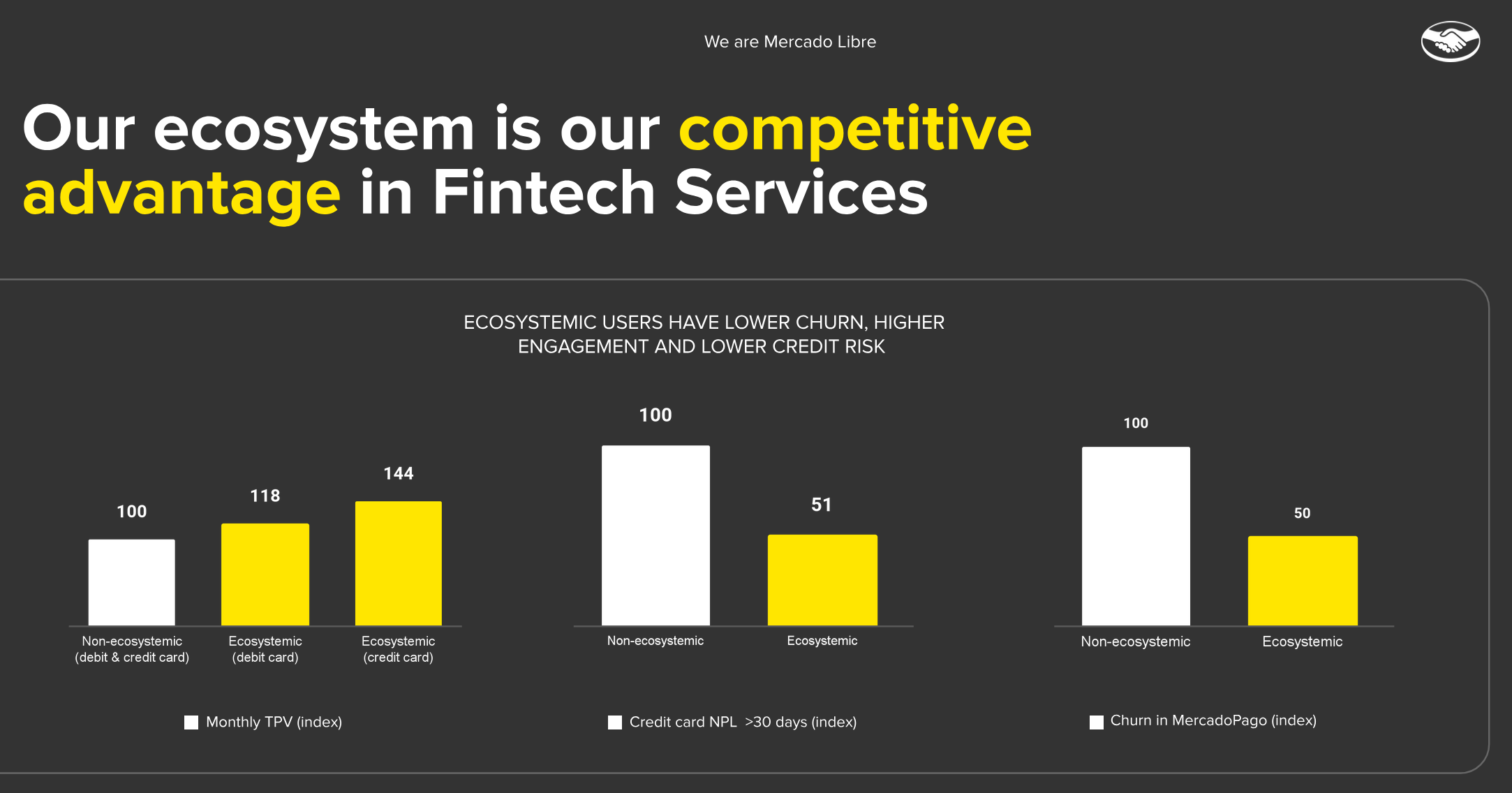

MercadoLibre is not underwriting users in a vacuum, it sees search behavior, purchase history, repayment patterns, merchant activity, wallet usage, and off-platform payments. That does not eliminate credit risk; it does suggest informational advantages over traditional lenders and over weaker competitors, a data flywheel. Amazon cannot replicate this through its Nubank partnership; partnerships do not integrate the way internal capabilities do. Shopee Pay is years behind Mercado Pago in both scale and data richness.

Fintech and commerce reinforce each other. The Q1 2026 cross-sell metric shows that the share of monthly active sellers (MAS) using Mercado Crédito grew from 26.3% in Q1 2025 to 36% in Q1 2026, +9.7% YoY. The clearest visual proof that the integration is doing economic work comes from MELI’s own internal comparison of users who interact with multiple ecosystem products (“ecosystemic”) versus users who use Mercado Pago in isolation (“non-ecosystemic”):

Marketplace sellers using credit transact more, recover working capital faster, and stick to MELI’s surface. In Argentina specifically, a market where the financial system is showing rising delinquency, Fintech President Osvaldo Giménez was direct:

“The 15-90 day NPL [Non-Performing Loans] in Argentina has improved sequentially. When we look at the market, we see that some banks are having worsening NPLs, but that has not been our case.”

In a country running 32.7% inflation, MELI’s underwriting outperformed the local banking system.

Three Structural Dampeners on Credit Risk

On the credit quality concern: the Q1 2026 shareholders letter was direct about how the data flywheel translates into asset quality:

“The credit card’s results in Q1’26 remained strong, and reflect the unique power of our ecosystem as the foundation of our strategy. Our ecosystem generates the demand that enabled us to issue 2.7mn cards and grow the portfolio by 104% YoY to $6.6bn in Q1’26; it also provides the data which makes our underwriting decisions increasingly accurate, contributing to improving asset quality as the credit card’s 15-90 day NPL fell by 80bps YoY.”

Reading this alongside the Q1 2026 results as a whole:

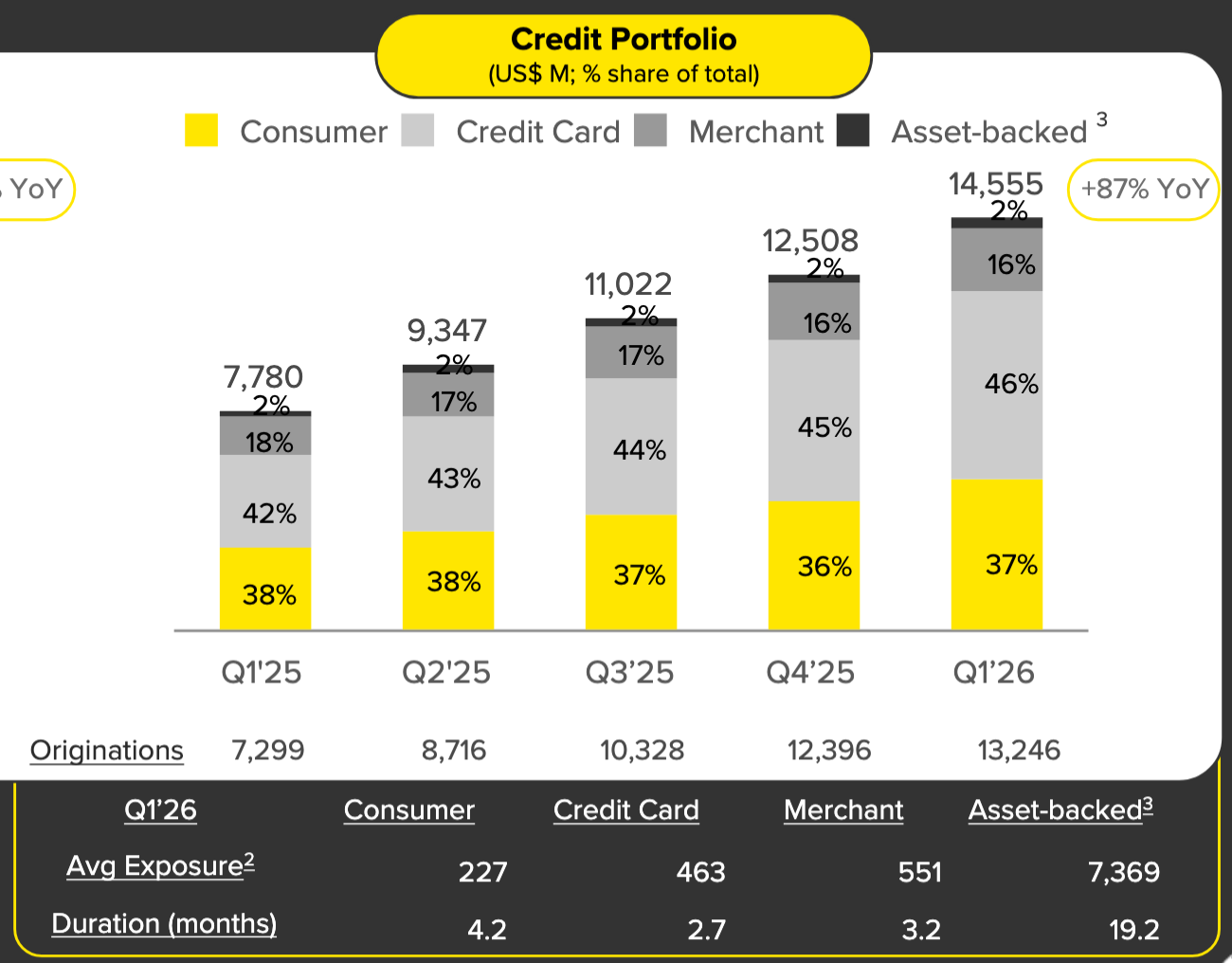

Total 15-90 day NPL 8% in Q1 2026 (vs 8.2% Q1 2025), broadly stable while the book grew +87% YoY.

Credit card 15-90 day NPL fell 0.8% YoY while the credit card book grew +104% YoY.

Provision coverage 103% on >15-day past-due loans, 149% on >90-day, reserved at more than the full face value of every loan currently past due.

Renegotiations fell from 1.6% (year-end 2025) to 1.4%, a leading indicator of hidden credit stress, moving the right way.

Three structural features dampen the bear-side credit cycle concern. First, MELI’s loans are exceptionally short duration even after the deliberate Brazil extension from five to eight months, most consumer loans (ex. asset-backed ones) roll in under a year, which means management gets near-real-time signal on asset quality and can tighten underwriting before losses compound through the book.

Short duration also reduces the CECL front-loading effect discussed in Part 1’s bear case #2, because the “lifetime expected loss” that must be reserved at origination is mechanically smaller when the loan is short. Second, one-third of the input data behind MELI’s underwriting decisions is proprietary first-party data - marketplace purchase history, repayment behavior on prior small loans, wallet activity, off-platform Mercado Pago transactions - that no other LatAm lender has access to. The traditional banks use bureau scores3; MELI uses bureau scores plus a behavioral data layer that does not exist anywhere else in the region. That is a measurable, quantifiable underwriting edge. Third, the LatAm consumer credit pool MELI is lending into is structurally different from a US-subprime analog: LatAm borrowers have spent their adult lives operating under high real interest rates, frequent inflation shocks, periodic currency crises, and an absence of cheap credit. Their financial behavior is calibrated to scarcity, not to the post-2008 low-rate environment that US-subprime risk models implicitly assume. A LatAm $200 working capital loan and a US $200 subprime credit card balance look superficially similar but live in completely different macro regimes, and the LatAm borrower is empirically more resilient through cycles.

How Mercado Pago Actually Builds a Credit Card Cohort

The way MELI builds the credit relationships is itself a risk management feature. New borrowers typically begin with a single-item buy-now-pay-later (BNPL) loan on a marketplace purchase, then graduate to a small credit card limit of a few hundred dollars, with the limit expanded only as repayment behavior accumulates on each prior step. Each loan is, in effect, a paid test of the underwriting model on that specific borrower, and the cohort is widened only after the test passes. This is fundamentally different from the way a traditional bank extends a credit card - typically a single approval decision based on a bureau score, with a four-figure starting limit and very little subsequent behavioral feedback before the next limit increase. The slow-then-fast structure is the reason MELI’s loss rates have so far surprised to the upside as the book has scaled: the underwriting model is being trained on observed payment behavior, not extrapolated from risk-tier mapping.

The Spread That Banks Cannot Compete For

On the lending economics, even after the Q1 2026 NIMAL compression to 17.8%, MELI’s risk-adjusted spread4 remains well above bank comparables - Nubank’s risk-adjusted NIM is 9.5%, Itaú’s implied risk-adjusted margin is 6.1%, Bradesco’s is 3.81%. Widening the lens beyond LatAm makes the gap even starker; JPMorgan Chase (JPM 0.00%↑), the largest US bank by assets, reported a Q1 2026 net yield on average interest-earning assets of 2.5% on $4.1 trillion of average interest-earning assets - that is before netting out credit losses. MELI’s 17.8% NIMAL is 7.1x the largest US money-center bank’s margin. The spread exists precisely because the traditional banking system does not want to operate in these segments - individuals with no credit history (or low credit scores) and SMBs. MELI earns a structural risk premium for doing what others won’t, serving a segment that is underserved by the major financial institutions.

It is worth pausing on why the spread is as wide as it is, because the bear case treats this as a warning sign. The LatAm banking system runs on regulated capital that is intermediated to a relatively narrow band of already-creditworthy borrowers - the four-bank concentration in Brazil (59% of credit operations) is not an accident, it is the visible expression of risk-weighted-asset rules that make it expensive for incumbent banks to extend balance sheet to a borrower without a clean prior credit history. The same regulatory structure that gives Itaú a 6.1% net interest margin (NIM) gives it no way to underwrite a $200 working capital loan to a Brazilian micro-merchant with no formal credit file, because the capital charge5 would consume the spread. Mercado Pago can underwrite the same loan profitably because its informational advantage (purchase history, repayment behavior on prior small loans, wallet activity, marketplace seller data) substitutes for the credit file the regulated bank requires, and because its funding mix is not bound by the same risk-weighted-asset framework that governs regulated banks. The 17.8% NIMAL is therefore not a temporary anomaly that will be competed away, it is the market-clearing price for credit in a segment that regulated banks cannot serve. The risk to watch is that the loss rates rise faster than the spread can absorb them, which is the asset-quality question the Q1 2026 NPL YoY trend is already addressing in MELI’s favor.

The Mix Shift: Fintech as the Eventual Larger Profit Pool

The size of the LatAm risk-adjusted spread, the breadth of the cross-sell flywheel, and the structural under-penetration of credit across MELI’s footprint together suggest a longer-term mix shift: at some point over the next decade, fintech is likely to become a larger share of MELI’s operating profit pool than commerce. The TTM Q1 2026 segment mix is already 43.8% fintech revenue growing 48.2% YoY versus commerce mix at 56.2% growing 37.8% YoY; on a forward operating margin basis, fintech earns more per dollar of incremental revenue than the marketplace does once credit card unit economics are normalized. That does not mean the marketplace stops mattering - it is the access infrastructure for the fintech customer in the first place, but it does mean the steady-state earnings architecture of MELI may end up looking more like a financial services compounder with an e-commerce funnel attached than the inverse.

Disrupting Both Sides of the Balance Sheet

The disruption on the deposit side of Mercado Pago is as important as the lending side, and Szarfsztejn explained the mechanism concretely:

“[…] if you go back a few years, you would basically leave your money in in a bank in Latin America and they would give you zero interest in that money. They would keep the float, the return, unless you put the money in a time deposit, in which case they would give you 60% of the benchmark rate. Back in 2017 […] we said, why don’t we give away our float and we pay our users 100% of the benchmark rate or even more in every single country, and with that we generate a big disruption in the traditional system. Before that in Argentina […] you only had 400,000 people in the whole country using investment products [and] time deposits. Today Mercado Pago has 18 million people receiving interest in their holdings every single day.”

This is the how Mercado Pago assets under management (AUM) is growing 2.7x faster than monthly active users (MAU): MELI gave up its float, the incumbent banks declined to follow, and per Szarfsztejn, a market that had 400,000 retail savers in Argentina now has 18 million on Mercado Pago alone receiving interest on their holdings. The same playbook is replaying in Brazil and Mexico.

Mercado Pago is also moving up the regulatory stack to match the strategic ambition. In September 2024 it filed a full banking license application with Mexico’s Comisión Nacional Bancaria y de Valores (CNBV), with management estimating a 12-24 month approval timeline; Nubank got there first in April 2025, and Mercado Pago is currently in queue alongside local digital fintech, Klar. In May 2025 it filed a parallel application with Argentina’s Central Bank, with the stated goal of building “Argentina’s largest digital bank”. A bank-charter unlocks two structural advantages over the current Payment Institution (IP in Brazil) / Electronic Payment Fund Institution (IFPE in Mexico) status: first, direct deposit-taking (checking accounts, savings, time deposits), which removes Mercado Pago’s dependence on third-party banking partners to fund the loan book and lowers the marginal cost of funding; second, a broader product set including mortgages, commercial loans, and unrestricted investment products. Mercado Pago has not sought to upgrade its Brazilian IP license to a full bank-charter yet - Brazil’s IP framework plus Pix plus Open Finance already gives MELI most of the operational flexibility it needs there, but the Mexico and Argentina filings tell the long-term ambition is institutional, not just fintech.

The practical economics of the bank-charter strategy are more concrete than they first appear when you look at the balance sheet. Per Note 3 of the Q1 2026 10-Q, Mercado Pago already holds $11.5 billion of restricted cash and cash equivalents at central banks and financial regulators across LatAm as of March 31, 2026 - $9.7 billion at the Central Bank of Brazil (held in non-interest-bearing accounts or Brazilian federal government bonds, per the country’s payment institution regulation), $740 million at Mexico’s CNBV, $366 million at Chile’s CMF, $342 million at the Argentine Central Bank, and $24 million at the Central Bank of Uruguay. The bulk of this is segregated to protect Mercado Pago user wallet balances under existing e-money / payment-institution regimes. A bank-charter in Mexico or Argentina would let MELI redeploy a portion of these segregated balances from non-yielding regulator accounts into the bank’s own loan book, earning interest income rather than zero. The “deposit-funding unlock” is therefore sitting on the balance sheet today, locked at central banks across the region, waiting for the regulatory wrapper that would let it work for shareholders rather than just for customer protection.

The wallet sits on top of the deposit relationship and is what makes Mercado Pago feel like a daily-use product rather than a payment app. In addition to the interest-bearing balance, the wallet offers a Mercado Fondo, a money-market fund available in Argentina, Brazil, Chile and Mexico (particularly relevant in high-inflation Argentina, where keeping pesos in cash erodes purchasing power weekly), life and personal-accident insurance distributed in partnership with Prudential in Argentina (since 2022) and credit insurance with MetLife in Brazil (launched 2025), in-app bill-pay, and Meli Dólar (MUSD), MELI’s own USD-pegged stablecoin launched in 2024 that effectively functions as a synthetic dollar account - currently available to users in Brazil, Mexico, and Chile (Argentine regulation has so far blocked launch in MELI’s most-dollar-hungry market). None of this is unique to Mercado Pago - Nubank also offers a digital wallet, yield products, insurance distribution, and a USDC-based crypto-yield product (4% annual return on USDC balances, launched January 2025) through its platform, but Mercado Pago has structural distribution that Nubank does not: every Mercado Libre marketplace user is one tap away from the wallet, and every Mercado Pago acquiring merchant is already in the payments funnel. The competitive battleground in LatAm consumer fintech is increasingly about which wallet captures the daily share of attention of the user, and MELI’s marketplace + acquiring presence gives it a daily-usage hook that Nubank has to win through promotion and brand spend.

Acquiring: Stronger Than the Share Table Suggests

Another leg of the fintech story is the acquiring business - Mercado Pago as a merchant payment processor, the LatAm equivalent of the role Stripe and Block (XYZ 0.00%↑) play in the US. By transaction volume processed, Mercado Pago is not the leader in any single LatAm market - in Brazil specifically, March 2026 data puts Mercado Pago fifth by volume (9% share) behind the three bank-owned acquirers Rede (18%, Itaú), Cielo (17%, Bradesco/Banco do Brasil) and PagBank (17%), as well as Stone (15%). Two structural angles make the position more interesting than the share table suggests. First, on profitability, per an Itaú BBA analyst note, Mercado Pago’s 2024 acquiring profits (R$1.93 billion) overtook both Stone (R$1.9 billion) and PagBank (R$1.78 billion), making it the most profitable pure-fintech acquirer in Brazil. Second, Mercado Pago is the only pure-fintech acquirer operating the same product across Brazil, Mexico, Argentina and Chile - Stone and PagBank are essentially Brazil-only - which means its acquiring TPV of $203.8 billion on a TTM basis in Q1 2026 is unmatched by any standalone-country fintech competitor. Acquiring TPV grew at 41% YoY in Q1 2026, with YoY country-level growth of +26% (Brazil), +46% (Mexico), +55% (Argentina) and +69% (Chile) - Mexico in particular is at an inflection point where cash-to-digital conversion is accelerating and the acquiring market remains structurally under-penetrated relative to Brazil.

The strategic value of acquiring is not just the take-rate on payments processed; it is that every merchant onboarded into the acquiring stack becomes a known counter-party whose transaction history can be used to underwrite Mercado Crédito and target Mercado Ads. The cross-sell flywheel works in two directions: marketplace sellers become acquiring customers because they already use Mercado Pago for marketplace settlement, and acquiring-only merchants (i.e. merchants who use the QR code or card reader outside the marketplace) become candidates for working capital credit and merchant ads. Mexico is also where MELI’s e-commerce-to-fintech hook is currently winning the consumer fintech market share race outright: Nubank, the dominant Brazilian fintech with 135 million users at home, is starting from a near-zero scale base in Mexico, while Mercado Pago has been compounding accounts there from inside an e-commerce app that already has millions of weekly active users. The competitive set in Mexico is structurally weaker than the one MELI faces in Brazil, and the runway is correspondingly longer.

The Marketplace Funnel Is a Channel Nubank Can’t Replicate

A related unit economics point: The cost of acquiring a fintech customer when that customer is already at checkout in the Mercado Libre app and gets offered a pre-approved credit card is effectively zero. The marketplace is doing the acquisition work for free. Nubank, by contrast, has to fund its customer acquisition through performance marketing, referral incentives, and brand advertising - and Nubank is widely recognized as one of the most efficient consumer-financial customer acquisition cost (CAC) operators in the world. MELI’s CAC is structurally lower than the best independent player’s, not because MELI is better at marketing, but because the marketplace funnel is a customer-acquisition channel that no standalone fintech can replicate.

The size of the runway is hard to internalize from the company-level numbers alone. MELI’s investor relations page frames it in terms of structural under-penetration.

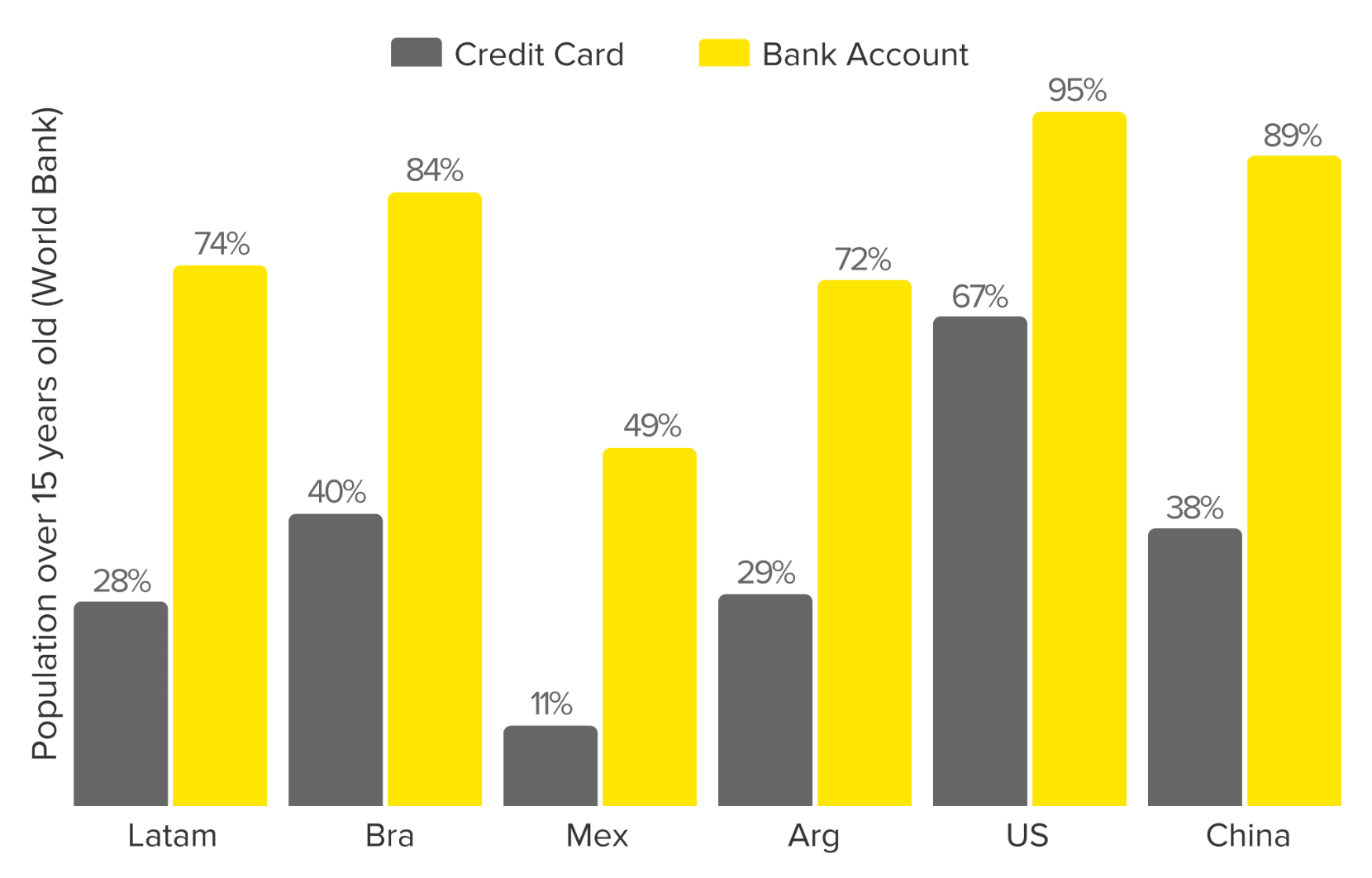

Mexico’s financial inclusion is more than a decade behind Brazil - half the population banked, less than a fifth carrying a credit card. Brazil itself remains four-bank-concentrated, with ~$200 billion parked in low-yielding “poupança” (savings) accounts that are an obvious migration target for Mercado Pago’s yield products. Argentina’s loans-to-GDP ratio sits below 10%, vs more than 50% in Brazil. Three different flavors of under-penetration in the three MELI’s largest markets, and Mercado Pago is the leading fintech by MAUs in two of those three markets.

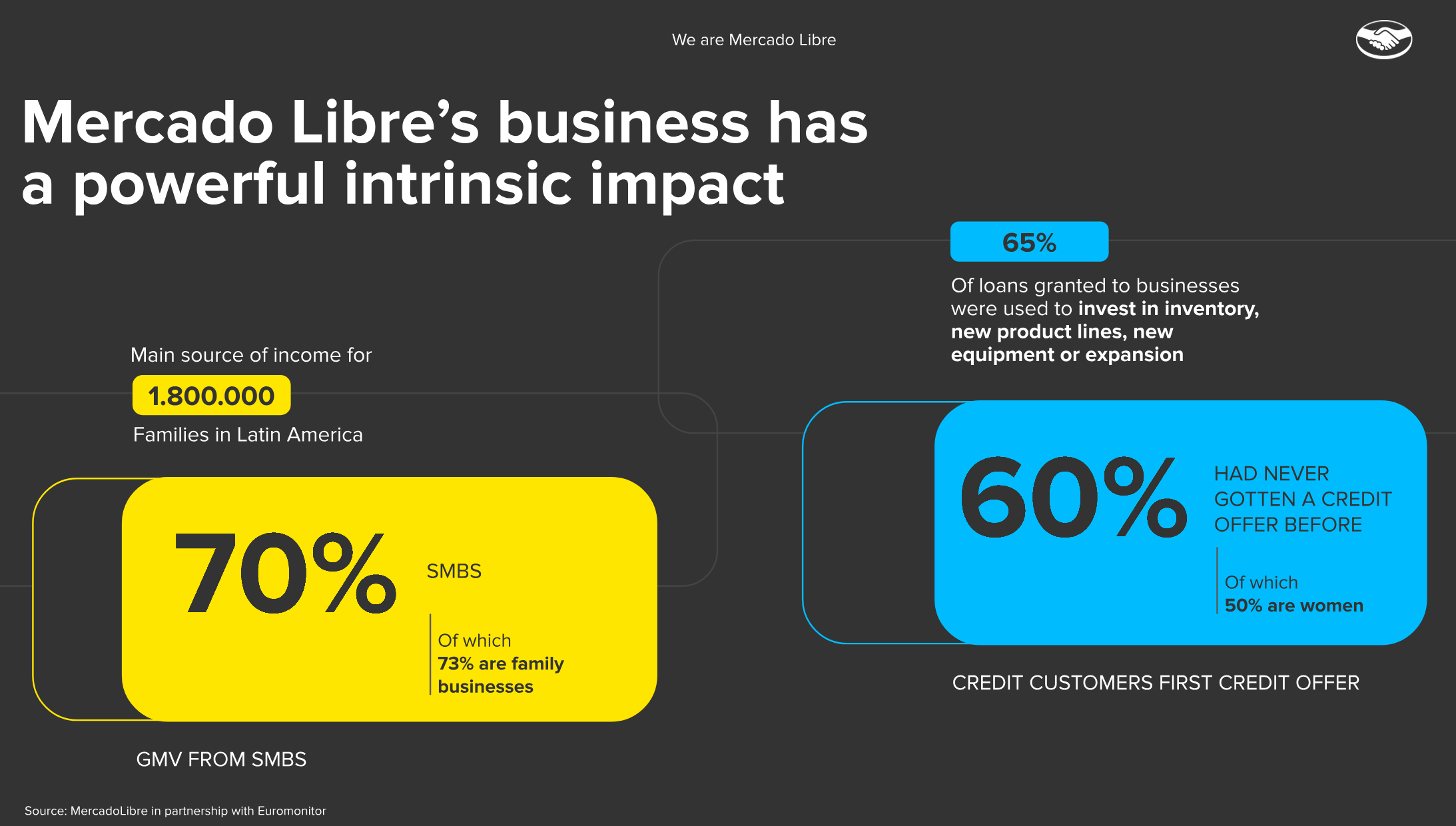

The composition of MELI’s credit book reinforces the same point from a different angle.

70% of GMV runs through SMBs (of which 73% are family businesses) - Mercado Pago credit overwhelmingly extends working capital to merchants who would otherwise rely on informal lending. 60% of MELI’s credit customers had never received a credit offer from any institution before MELI extended one. 65% of business loans were used to invest in inventory, new product lines, or expansion. The bear case is right that lending into populations traditional institutions have avoided is risky; the same fact, read the other way, is the structural reason MELI can earn 17.8% NIMAL while Nubank earns 9.5% and Itaú 6.1%. The bank comparison is mechanical: traditional banks have already captured the borrowers they want; MercadoLibre’s surplus comes from doing what others do not.

Ecosystem Lock-In: Where the Equity Value Compounds

Marketplaces and logistics tend, at equilibrium, to compete their take-rate down toward the cost of running them. The economic profit lives in the layers above - loyalty, advertising, credit - which is exactly where MELI is investing.

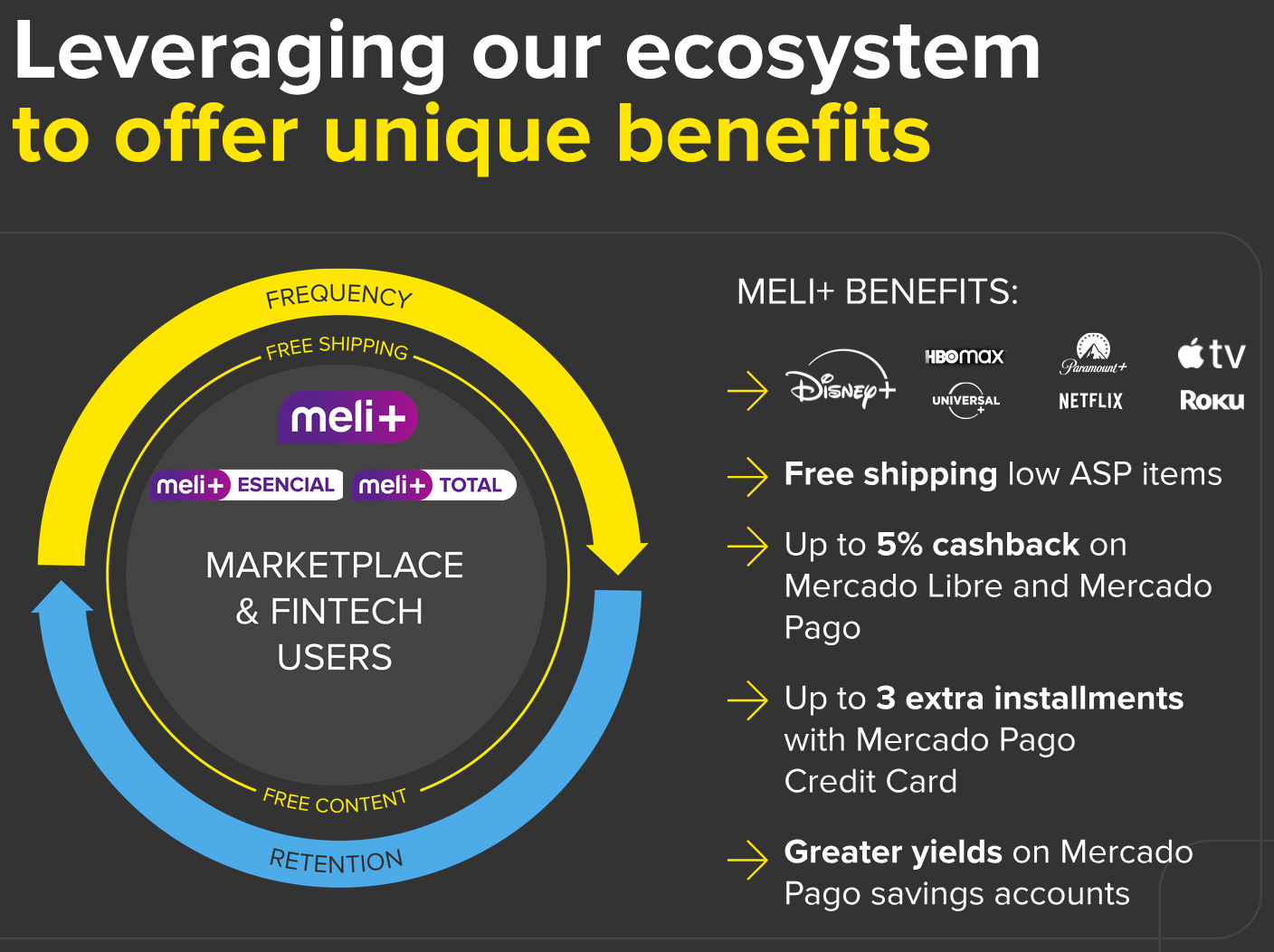

MELI+: Bundling Frequency, Yield, and Content

MELI+, the loyalty program, is a retention mechanism that goes beyond discounts. In Brazil it bundles shipping benefits, cashback, longer installment plans, greater savings yields on Mercado Pago, and entertainment subscriptions including Disney+, Netflix, HBO Max, and Apple TV+. Consumers embedded in this ecosystem are daily users who happen to shop. MELI+ subscribers in Brazil grew 49% from Q3 2025 to Q1 2026.

This is the architecture Amazon spent twenty years building toward with Prime, and it is the reason MELI’s cross-sell flywheel (26.3% → 36% of merchants using Mercado Crédito in twelve months) does not look like a coincidence.

Mercado Ads: Where the Equity Value Compounds

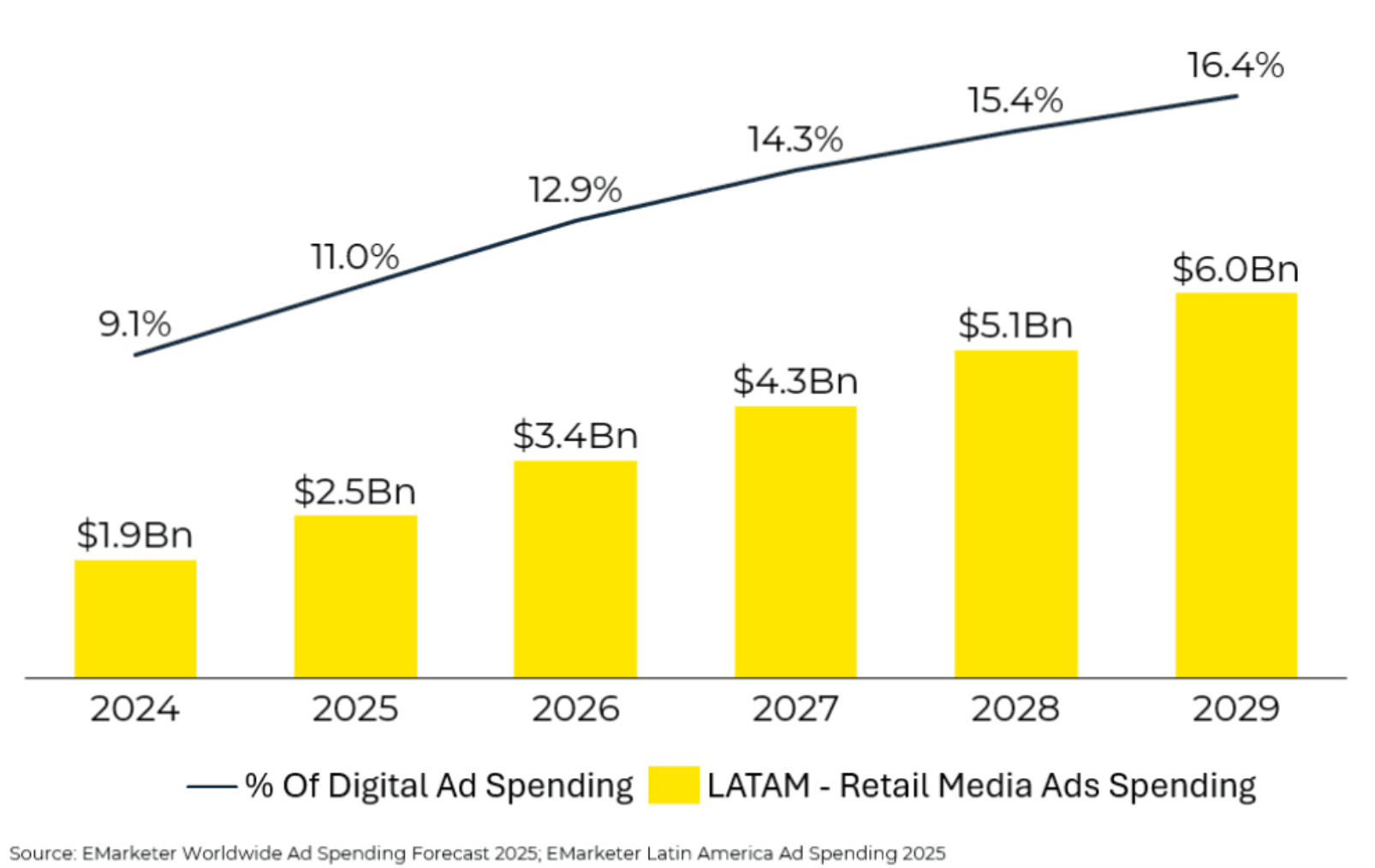

That same ecosystem data feeds a growing advertising business. In mature, competitive e-commerce markets, the marketplace and logistics layers tend over time to compete the gross take-rate down toward something close to the cost of operating them - the marketplace itself does not capture much economic profit at equilibrium. The profits actually live in the layers built on top of the marketplace: the advertising auction that the marketplace’s first-party consumer-behavior data enables, and the credit and payment layer that the marketplace’s transaction flow enables. This is how Amazon’s North American retail segment works. The marketplace and the logistics network are the access infrastructure that earns MELI the right to monetize a customer; the ad layer and the fintech layer are where the equity value compounds. Mercado Ads grew 73% YoY in Q1 2026, ~4x regional ad market growth. LatAm’s digital advertising market is still only ~50% of total ad spend (vs ~75% in the US), and MELI has the largest first-party data set on consumer behavior in the region to offer advertisers unique audience targeting capabilities.

LatAm retail media6 is projected to triple from $1.9 billion in 2024 to $6 billion by 2029. Even at that level, retail media penetration of LatAm’s total digital advertising would reach only 16.4%, below where the global average sat four years earlier in 2025, ~21%. MELI is the leading platform in the regional retail media market today, with a first-party data set no LatAm competitor matches. The 73% growth in Q1 2026 is therefore early-cycle, into a profit pool that is structurally undersized vs the same pool in developed markets.

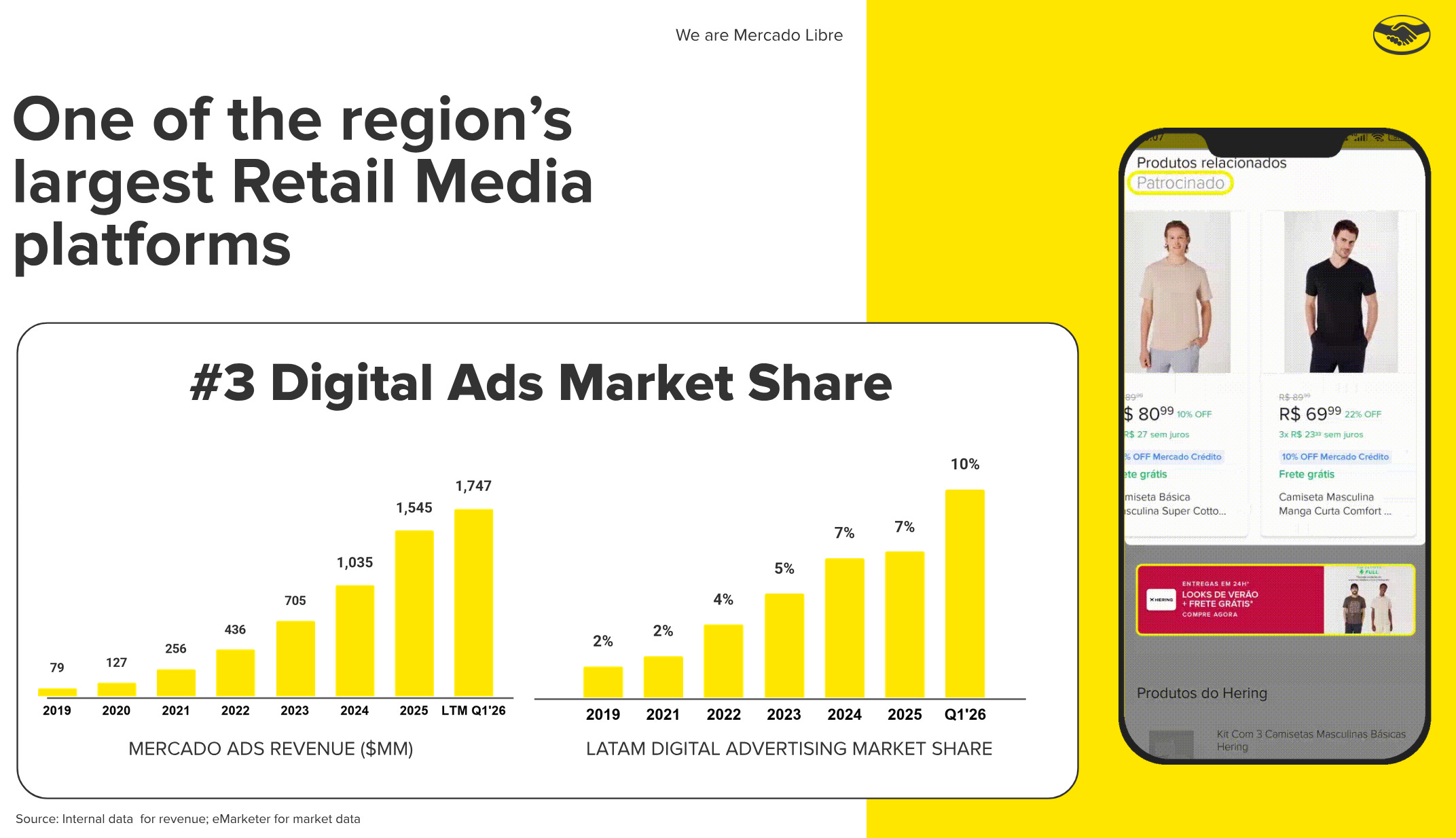

Mercado Ads has gone from $79 million of revenue in 2019 to $1.75 billion over the LTM ending Q1 2026, a 22x increase in less than seven years. MELI’s LatAm digital advertising market share has stepped from 2% (2019) to 10% (Q1 2026), making MELI the #3 platform in the region by digital ad share, behind only Google and Meta. The slope of both bars is what matters: ads are scaling faster than the total marketplace, which is exactly the high-margin-profit-pool transition Amazon executed a decade ago.

Mercado Play: Off-Platform Ad-Tech as Category Expansion

Mercado Play is MELI’s free, ad-supported streaming service inside the Mercado Libre app, a regional analog to Roku Channel that monetizes through ads against licensed content. The more interesting development is off-platform: Mercado Ads has begun powering the LatAm ad-targeting stack inside third-party streaming inventory. Disney+ is running campaigns in LatAm that use Mercado Ads’ first-party consumer data as the audience-targeting layer; similar arrangements have been signed with Google for open web ad placements. The implication is that the target addressable market (TAM) for Mercado Ads is not bounded by impressions on MELI’s own apps; it is the full LatAm digital advertising market, with MELI providing the data-and-targeting layer that streaming platforms and ad networks plug into. That is a category-expansion, not just a category-deepening, story, and it is the kind of asset-light extension that makes the high-margin profit pool more durable than a pure on-platform retail media business would be.

AI productivity is now starting to show up in the operating numbers. Q1 2026 disclosed Claude Cowork rolled out to 31,000 employees; engineer headcount planned flat in 2026; Product and technology contributed +1.4% of positive operating leverage in the Q1 2026 margin. Worth flagging that MELI's own 10-K identifies this productivity layer as a risk as well as an opportunity, noting that:

“AI/ML and cloud computing ecosystem is characterized by high concentration in hardware and infrastructure supply, and our ability to scale certain AI/ML models may depend on the pricing and availability of computing resources provided by a small number of global vendors, which may limit our speed or cost efficiency relative to competitors.”

Applied to the “who captures the surplus” lens one layer down: every AI-driven productivity dollar MELI captures has to be shared with the upstream model and compute providers, and how durable the operating leverage tailwind proves to be will depend partly on pricing dynamics MELI does not control.

The Flywheel That Has Been Spinning Visibly for a Decade

More consumers shopping on the platform makes it easier to attract more merchants. More merchants means more selection. More selection drives more price competition between sellers, which structurally lowers prices for consumers. Lower prices attract yet more buyers. Around the loop it goes. This is the architecture of the business, and the same architecture that made Amazon’s marketplace increasingly defensible over time. The cleanest visualization of where this has already gotten MELI:

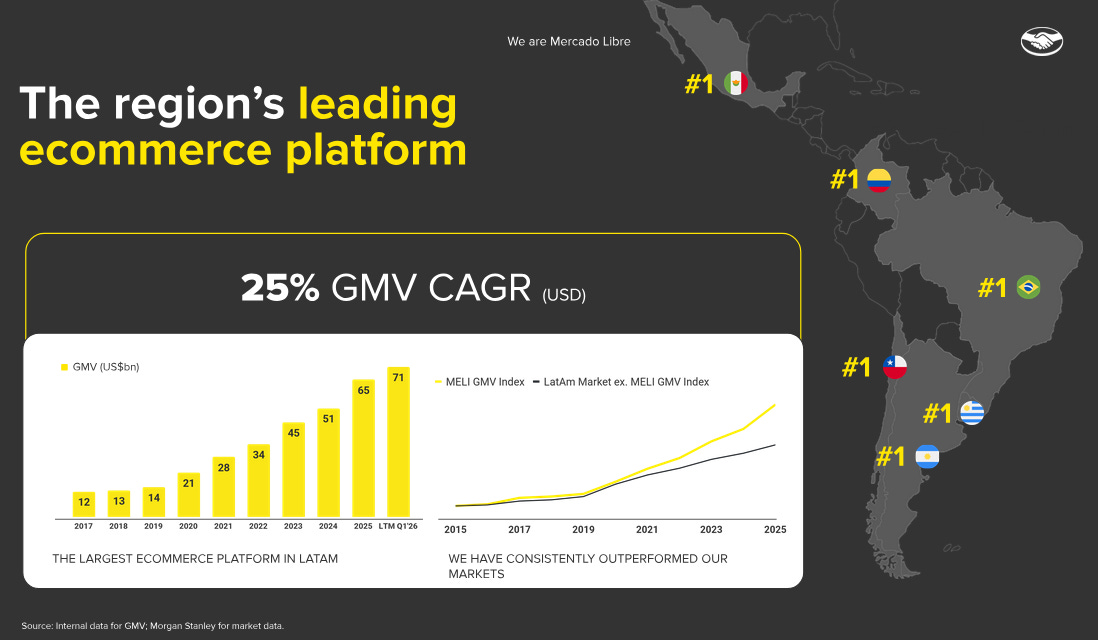

GMV grew from $11.8 billion in 2017 to $70.7 billion over the LTM ending Q1 2026 - a 23.8% CAGR over eight years through a global pandemic, a US rate cycle, two Argentine sovereign restructurings, and the arrival of Shopee, Amazon, and TikTok Shop as serious competitors. MELI’s GMV index has consistently outpaced the LatAm-ex-MELI GMV index since 2019, and MELI is #1 in six markets simultaneously - Brazil, Mexico, Argentina, Chile, Colombia, and Uruguay. No US or Asian competitor holds #1 market share in even half that many LatAm markets. Leadership is not something MELI is fighting for, it is the starting point of every other argument in this section.

The Dying Brazilian Long Tail

Part of what is feeding the GMV CAGR is a structural consolidation in Brazilian e-commerce. Legacy domestic players, Magazine Luiza, Americanas, and the rest of the long tail of Brazilian retailers that attempted to build online businesses in the 2010s, have spent the last several years losing market share and, in Americanas’ case, working through accounting fraud and bankruptcy proceedings. The Brazilian e-commerce market is converging toward a three-player equilibrium of MELI, Shopee, and Amazon, with the long tail acting as a market share donor to all three. MELI’s GMV growth is therefore being fed by two distinct sources at once: organic growth from the expanding e-commerce pie, and inorganic share gains from the dying long tail. Both are real, and only the first one will moderate when LatAm e-commerce penetration eventually catches up to developed market levels.

Argentina: a Clean Demonstration of MELI’s Unit Economics

Worth noting on the geographic split: Argentina, the smallest of MELI’s big three markets, is also its most profitable. The bear-side macro and FX concerns documented in Part 1’s bear case #3 are real, but the same competitive vacuum that lets Argentina’s macro volatility hit MELI’s USD reported earnings is what gives MELI uncontested pricing power and unit economics there. There is no serious local e-commerce challenger, Amazon does not operate at scale in the country, and Shopee withdrew its local operations entirely in September 2022. The Shopee retreat is worth dwelling on because it speaks to the broader LatAm competitive picture: in the same month, parent company Sea Limited (SE 0.00%↑) also shut Shopee’s local operations in Chile, Colombia, and Mexico, retreating to a cross-border-only model in those three markets and pulling out of Argentina without leaving even a cross-border footprint. The decision was driven by Sea’s pivot to profitability after a $1.6 billion 2022 net loss; in CEO Forrest Li’s framing, the move was about exiting “low-ROI geographies” to focus capital on Southeast Asia, Taiwan, and Brazil. The signal embedded in that retreat is that Shopee’s Singapore-headquartered model could not make the unit economics work in any LatAm market except its single biggest target. The bull-side reading of Argentina specifically is that it is the cleanest demonstration of what MELI’s unit economics look like in a market with no competition, which is the path Brazil and Mexico are building toward as their respective competitive landscapes settle.

The Flywheel Is Spinning Faster, Not Slower

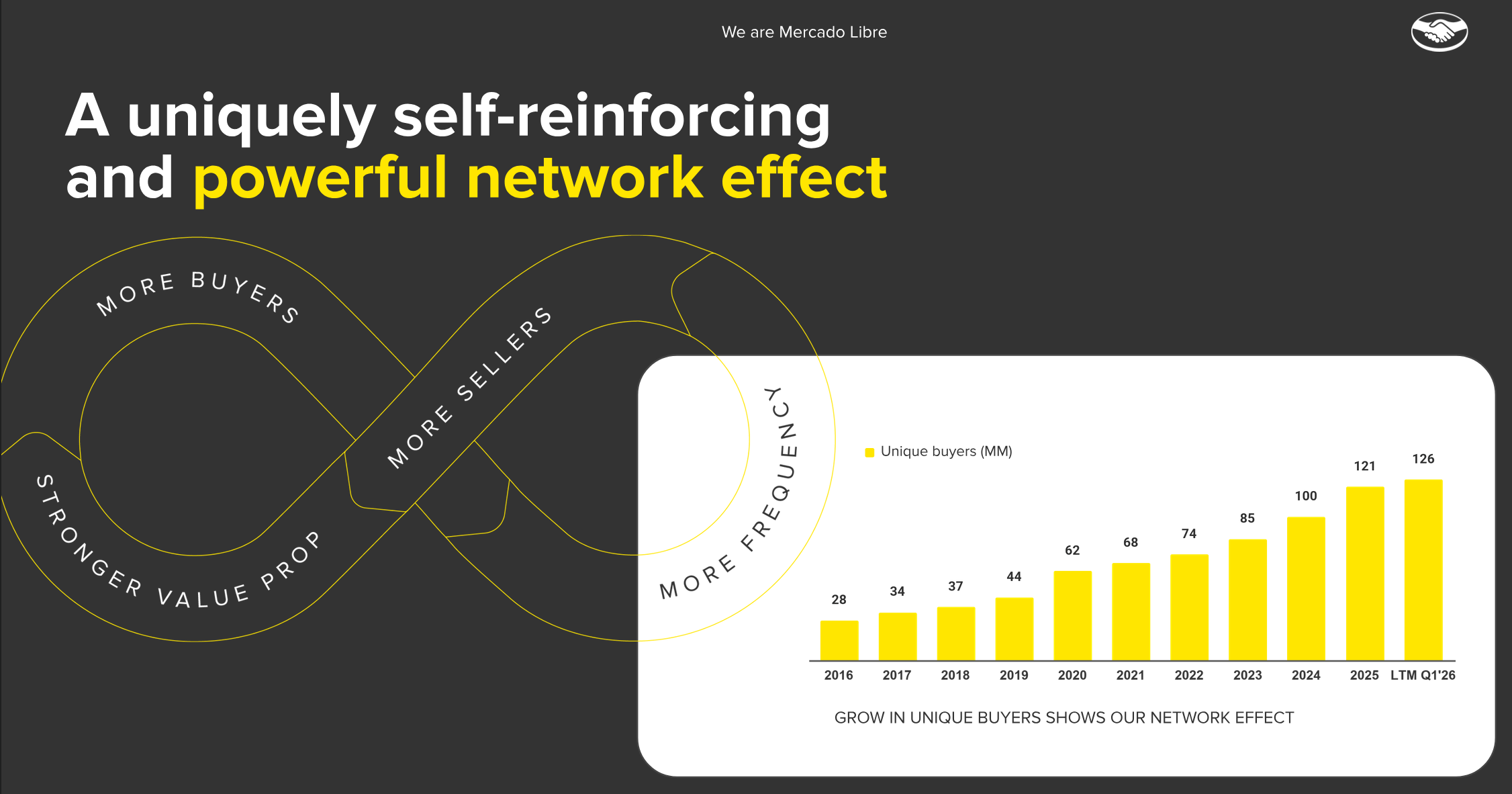

The Q1 2026 numbers say the flywheel is spinning faster: 84.1 million unique active buyers on the marketplace (+26% YoY) and 82.9 million fintech monthly active users (+29% YoY) with leading net promoter score (NPS) in Brazil, Mexico, Argentina and Chile. AUM in Mercado Pago grew 77% YoY to $19.9 billion, growing 2.7x faster than MAU, the signature of deepening engagement, not just user acquisition.

Unique buyers grew from 28 million in 2016 to 126 million in LTM Q1 2026 - 4.5x in ten years, or 16.2% CAGR through the same period that the bear case rightly notes that Shopee, Amazon, and TikTok Shop entered the region. User growth alone understates what is happening: buyers shopping across three or more product categories has grown 130% from 2022 to Q1 2026, and average quarterly items purchased per buyer has stepped from 4.4 in 2019 to 9 in 2025 - more than doubling per-buyer frequency on a buyer base that itself nearly tripled over the same window. Engagement deepening at this rate is what compounds the unit economics, and it is why the Q1 2026 +56% YoY items sold acceleration in Brazil is not a one-quarter anomaly, it is the visible tip of a six-year frequency curve.

The single cleanest evidence that the network effect is still strengthening rather than weakening under competitive attack is the simultaneous direction of two Brazil metrics: items sold growth has accelerated from +26% YoY in Q2 2025 to +56% in Q1 2026 while unit shipping cost has decelerated in the negative direction (from -11% YoY to -17%) - i.e. the buyer base, the per-buyer frequency, and the unit economics are all moving in MELI’s favor through exactly the period when Shopee, Amazon, and TikTok Shop have intensified their attack. Network effects that are weakening under competitive pressure look like decelerating user growth or rising customer acquisition cost; MELI shows neither.

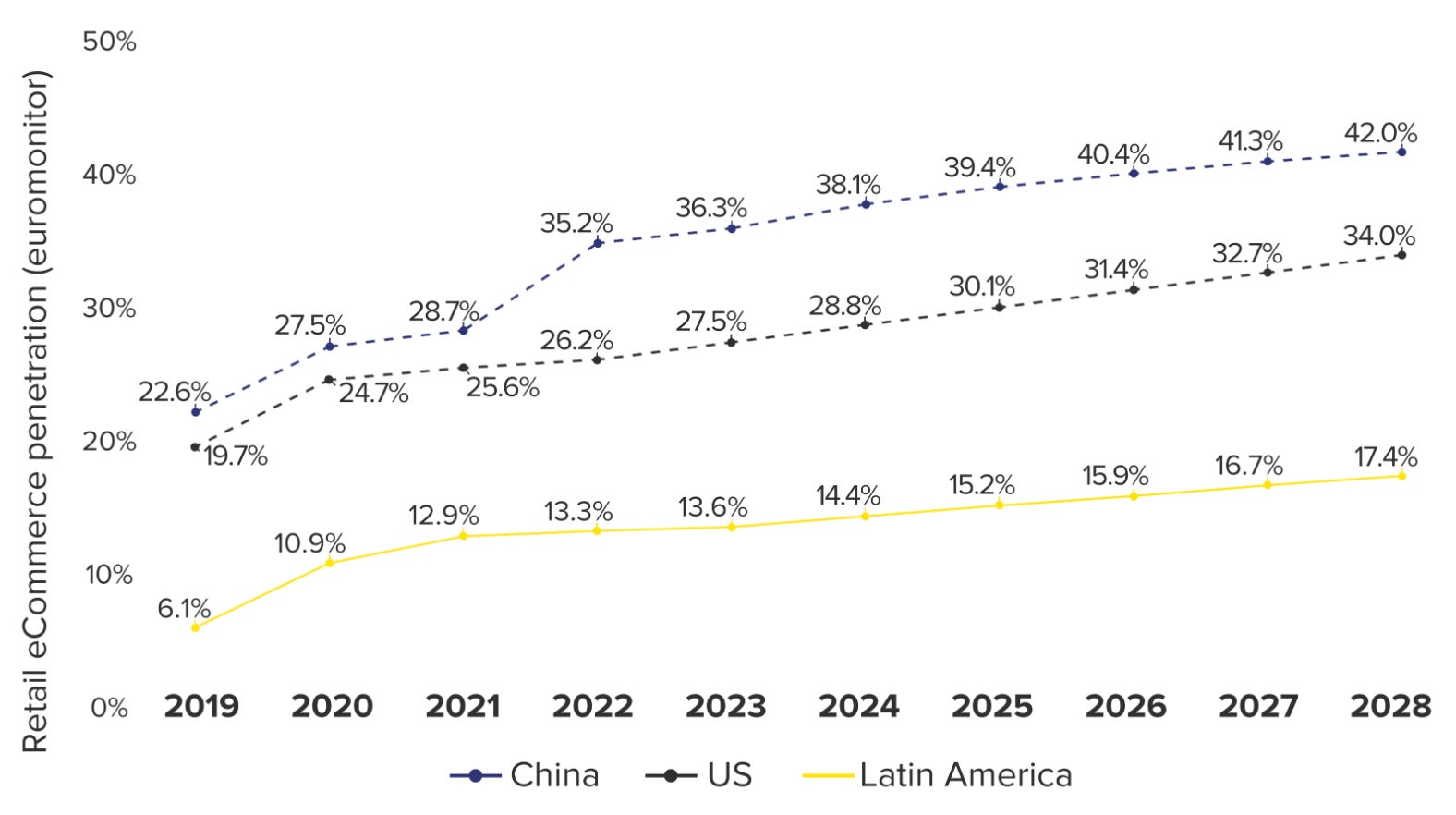

MELI today reaches ~24% of the LatAm buyer population; e-commerce in the United States and China run buyer base penetration in the 60-70% range. The runway has two compounding axes: more of the wallet (e-commerce share of retail rises) and more wallets (more of the population becomes a MELI buyer). Both are visible in the Q1 2026 numbers - items per buyer accelerating +56% YoY, and the buyer base growing +26% YoY.

LatAm e-commerce penetration sits around 15% of total retail today (per ECDB and Ant International), half the United States, and roughly where the US was almost a decade ago. Third-party forecasts cited by MELI project the regional e-commerce market to grow from $151 billion in 2023 to $232 billion by 2028 (+54%). Even after Shopee, Amazon and TikTok Shop have built market share, the pie is growing faster than the share war is settling, and MELI’s merchant + buyer + logistics + credit + ad combination is the most complete LatAm-native stack going after the conversion.

The Market Is Pricing the Bear Case; The Chart Says Pricing the Bull One Is Cheaper

I value MELI on owner’s earnings, not P/AFCF or GAAP P/E, which is distorted by reinvestment, and the accounting treatment of the credit book. Applied to Q1 2026 (full build in my Q1 2026 results article), normalized owner’s earnings annualize to approximately $6.1 billion on a TTM basis. On a ~$80 billion market cap, MELI trades at ~13x normalized owner’s earnings, a modest multiple for a business compounding revenue above 30% for 29 consecutive quarters and accelerating to 49% growth in Q1 2026.

The ROIC Recovery the Market Is Extrapolating Against

On the ROIC concern that Part 1 lays out, the historical record is the strongest single rebuttal the bull case has, and it is worth laying out here because it bears directly on whether the current multiple is reasonable. The same ROIC chart referenced in Part 1’s bear case #5 covers the only meaningful ROIC observation window for the modern business, from December 2018 forward, and it tells a very specific story:

MELI ran negative ROIC for two full years (a trough of -14.4% at year-end 2019 and -14.2% in mid-2020) as Mercado Envíos was being built out and the company was absorbing the full P&L hit of shipping subsidies and fulfillment center spend. By Q1 2023 ROIC had crossed back through 20%, between Q3 2023 and Q1 2024 it was running consistently in the low-30s, and by mid-2024 it peaked at 34%. The shape of the recovery from the 2018-2020 trough into the 2022-2024 peak is the most economically valuable data point on the chart: 48% of ROIC expansion in four years on the same logistics infrastructure that Szarfsztejn now describes as “more developed than Amazon’s”. The current compression cycle is real and worth respecting; what it is not is unprecedented.

The shallower 2024 mid-cycle ROIC dip from 34% to 23.4% in late 2024 is a closer-in version of the same pattern, driven by the early stages of credit card book scaling and free shipping threshold reset. ROIC then briefly re-accelerated to 28.4% before the current step-down through 26.8% → 23.1% → 20.8% → 19.2% → 16.7% Q1 2026 - the five-quarter compression that anchors the bear case. The latest reading still sits above the eight-year cycle average of 12.5%; the bear point is the direction of travel, the bull point is the level. Both readings are correct.

That historical record does not make the current cycle a sure thing. The current investment program is wider than either prior one (credit, 1P, and logistics all reinvesting simultaneously), and the asset base it is being applied to is materially larger. The pattern of “deliberate ROIC compression followed by recovery to a higher level than the prior peak” is the dominant pattern in MELI’s history, not the exception, and the chart shows it twice in eight years. At ~13x normalized owner’s earnings, the market is currently extrapolating the compression line straight through to zero and pricing in none of the recovery pattern that the same chart documents. That is the asymmetry the bull case rests on.

Graham taught me that price is what you pay and value is what you get. On an owner’s earnings basis, the market is currently paying for the bear case and ignoring the bull one.

Coming Next: Where I Land

I have built the bear case in Part 1 and the bull case above. Both readings of MELI’s results are internally consistent; both extrapolate the same numbers in defensible but opposite directions. Part 3 brings them together: where the bear and bull arguments actually disagree, the three signposts that will resolve the debate over the next years, and where I currently land on the stock, including what I have been doing with my position.

Hub-and-spoke logistics network is a distribution model in which goods flow from a small number of large, centralized hubs (fulfillment centers and regional sortation facilities) outward through a tree-like topology to local delivery stations and then to end customers. The model is efficient when last-mile road infrastructure is uniform and dense, because volume can be concentrated at each hub level to drive economies of scale; it is the architecture Amazon, FedEx, and UPS use in the United States. Its weakness in markets with uneven road infrastructure or fragmented population density is that every package must travel through a small number of bottleneck nodes, and a disruption at any hub cascades through the entire downstream network.

Mesh logistics network with cross-docking facilities is an alternative topology in which goods flow through a larger number of smaller intermediate facilities that can route packages flexibly across multiple paths rather than through a single hub. A cross-docking facility is one of those intermediate nodes, a warehouse where inbound trucks unload merchandise that is immediately re-sorted onto outbound trucks heading to different regional destinations, typically within hours and with minimal or no storage in between. The architecture trades off the per-node economies of scale of a hub-and-spoke model for redundancy, route flexibility, and resilience to last-mile infrastructure unevenness, which is why it tends to be the preferred topology in markets where roads, population density, and fulfillment-center economics are more variable than in mature developed-market geographies.

Bureau score is a numeric creditworthiness rating produced by a credit bureau (Experian, Equifax, TransUnion in the US; Serasa, Boa Vista, SPC in Brazil) based on a borrower’s reported credit history - open and closed accounts, payment timeliness, outstanding balances, credit utilization, length of credit history, and recent credit inquiries. The score is the single most widely used input in traditional bank underwriting; FICO in the US (300-850 range) and Serasa Score in Brazil (0-1000 range) are the best-known examples. Its core weakness, particularly in underbanked markets, is that it requires a meaningful prior credit history to produce a meaningful score; borrowers with no formal credit file are either rated as high-risk by default or rejected outright, regardless of their actual repayment behavior.

Spread (in lending) is the difference between the interest income a lender earns on its loans and what it pays to fund them, after absorbing credit losses - i.e. what is left over to cover operating costs and earn a return on equity. Net interest margin after losses (NIMAL) is the most common single-line measure of it.

Capital charge is the amount of regulatory equity capital a bank is required to set aside against a given loan to absorb potential losses. Under Basel rules, every loan is assigned a risk weight based on borrower creditworthiness - a loan to a borrower with no formal credit file can carry a risk weight of 100% or more, versus 20-50% for a prime corporate borrower, and the bank must hold roughly 8-12% of that risk-weighted amount as equity. That equity has a cost, and the income the loan generates has to clear that cost before the bank earns any economic profit. On a small, high-risk-weighted loan, the cost of holding the required equity often exceeds the interest the loan would generate which is why regulated banks structurally cannot serve the segment Mercado Pago lends into profitably.

Digital advertising is the full universe of paid online ads (search, social, display, video, audio). Retail media is the subset served on e-commerce platforms themselves, monetizing the platform’s first-party purchase data. Global retail media is ~21% of digital ad spend (2025) and is the fastest-growing slice; LatAm sits at 9.1% (2024) and is forecast to reach 16.4% by 2029 - i.e. the regional pie is converging toward developed-market norms, and Mercado Ads is the incumbent best positioned to capture that convergence.

Excellent piece. The mesh vs hub-and-spoke logistics comparison was a great detail and really highlights why MercadoLibre's home-market advantage is so hard to compete with. Looking forward to Part 3.

Excellent analysis!