The Intelligent Investor: Timeless Lessons and Their Modern Relevance

Reviving value investing teachings by Benjamin Graham in a modern context

Introduction

In the ever-evolving landscape of finance, where technology and rapid information flow dominate, the foundational principles of investing are continually tested against modern complexities. Yet, amidst this dynamic environment, the wisdom of Benjamin Graham, the father of value investing, remains relevant. Graham’s approach, famously detailed in his seminal work The Intelligent Investor, advocates buying stocks when the company’s intrinsic value far exceeds its stock price, a strategy designed to minimize risk and seize undervalued opportunities.

Graham’s methodology emerged in the early to mid-20th century, a period characterized by less efficient markets and significant information asymmetry. I’ve distilled the key takeaways from this cornerstone of value investing in a previous post, and I recommend reading that before continuing with this one.

As we navigate the complexities of the 21st-century stock market, we find that the landscape has transformed dramatically since Graham’s era. The rise of intangible assets, such as intellectual property and brand value, alongside the growth of capital-light, scalable business models, has shifted how we assess a company’s worth. Stock markets have become more efficient, and the once-clear lines defining undervalued stocks have blurred.

Can the core principles of value investing, as laid out by Graham, still guide us toward sound investing decisions in an age dominated by technological innovation and instant access to information?

In this post, I’ll delve into The Intelligent Investor’s enduring teachings and explore their modern relevance. By bridging the gap between timeless wisdom and contemporary practice, I aim to provide thought-provoking ideas to help you navigate the challenges of modern investing while honoring principles that have stood the test of time.

Expanding Mr. Market: Exploring the Cognitive Biases Behind Market Irrationality

While Graham was a pioneer in recognizing the emotional aspects of investing, modern behavioral finance has advanced our understanding of the cognitive biases that drive irrational market behavior. Graham’s Mr. Market allegory highlights the irrationality of investors, and researchers like Daniel Kahneman have shown how biases like loss aversion (the fear of losses outweighing the desire for gains) affect decision-making.

Kahneman’s Thinking, Fast and Slow explores biases such as anchoring and overconfidence, which distort investors’ judgment. While Graham emphasized avoiding emotional decision-making, modern behavioral finance provides deeper insights into how specific biases, such as overconfidence, herding, and confirmation bias, systematically lead investors astray, expanding on the groundwork Graham laid.

Reevaluating the Margin of Safety: Balancing Caution with Accurate Forecasting

Graham coined the term margin of safety in his seminal book Security Analysis (1934), co-authored with David Dodd, and later expanded on the concept in The Intelligent Investor (1949). This principle is a cornerstone of Graham’s value investing philosophy. He famously wrote:

“[…] the function of the margin of safety is, in essence, that of rendering unnecessary an accurate estimate of the future. If the margin is a large one, then it is enough to assume that future earnings will not fall far below those of the past in order for an investor to feel sufficiently protected against the vicissitudes of time.”

The advice is straightforward: buy a stock at a sufficiently low price, and future uncertainties become less concerning.

Before proceeding, let’s revisit the definition of value investing. Value investing is a strategy that involves purchasing stocks that appear undervalued relative to the business’s intrinsic value. Intrinsic value is generally defined as the sum of all future cash flows the company is expected to generate, discounted to their present value. The rationale is that the stock market may not always reflect a company’s true worth, creating opportunities for investors to buy at a discount. This discount is what Graham calls the margin of safety.

While valuing a business based on its historical performance (the past) and current standing (the present) is crucial, I believe it’s equally important to create as accurate a forecast as possible for its potential outcomes over the next five years (the future). After all, a company’s intrinsic value is based on its future cash flows, discounted to the present. Without a well-formed view of the future, it becomes difficult to determine if a true margin of safety exists, or worse, if it’s inaccurate.

In my view, combining solid fundamental analysis with as accurate a forward-looking perspective as possible provides a holistic approach to assessing a company’s intrinsic value today. By evaluating near- to mid-term scenarios, including the company’s future growth rate and how today’s strategic decisions will impact its future, we can refine our valuation. In the modern economy, where innovation moves at an unprecedented pace and information flows constantly, a broad-brush approach to forecasting may cause investors to miss significant opportunities.

In summary, the margin of safety should come from purchasing a stock at a price below its intrinsic value. By doing so, we protect ourselves from the risks of an inaccurate forecast without using the margin of safety as an excuse to avoid thoughtful consideration of a business’s future possibilities.

Diversification Made Simple: Applying Graham’s Principles with Index Funds and ETFs

Graham emphasizes the importance of diversification as a core principle for managing risk and achieving long-term financial success. While he advocated for carefully selecting a diverse portfolio of individual stocks, or purchasing an equal-weighted share of each stock in a reputable index like the Dow Jones Industrial Average (DJIA) during his time, modern financial vehicles such as index funds and Exchange-Traded Funds (ETFs) have made diversification simpler and more accessible for today’s defensive investors. These passive investment options offer broad market exposure at a low cost, aligning well with Graham’s philosophy of reducing risk through owning a wide range of assets. By allowing investors to spread their investments across various sectors and geographies, index funds and ETFs provide a convenient way to implement Graham’s timeless strategy.

Since Jack Bogle, founder of Vanguard, introduced index funds in the 1970s, these tools have provided an easy and efficient way for investors to diversify their portfolios without requiring knowledge of financial markets, reflecting the principles of passive investing that Graham would likely endorse. As Bogle famously wrote in The Little Book of Common Sense Investing:

“Don't look for the needle in the haystack. Just buy the haystack!”

Over, the years, family and friends have sometimes asked me how to invest passively; I’ve always recommended a defensive approach: passive investing for the portion of their portfolios invested in stocks, by buying and holding a globally diversified ETF that tracks a well-regarded index like the MSCI World Index.

I believe that over the long term, regularly applying dollar-cost averaging by investing in an index fund or ETF that tracks a global stock market index is a recipe for building enduring wealth.

The Rise of Intangible Assets: Why Graham’s Approach Needs Modern Adaptation

Graham advocated for investing in companies where the stock price is not far above the company’s tangible assets. As he wrote:

“If he [the investor] is to pay some special attention to the selection of his portfolio, it might be best for him to concentrate on issues selling at a reasonably close approximation to their tangible-asset value - say, at not more than one-third above that figure.”

This selection criterion was effective in an era when physical assets like factories, land, and equipment formed the bulk of a company’s value.

However, in today’s world, this focus on tangible-asset value has become less relevant, especially in sectors like technology, pharmaceuticals, and consumer brands, where intangible assets dominate the balance sheet. Companies in these industries often operate with capital-light business models, relying heavily on intangible assets such as intellectual property, software, patents, copyrights, and brand value, rather than physical assets. The value of these businesses is derived not primarily from their tangible assets but from their innovation, customer networks, and growth potential. As a result, focusing solely on tangible-asset value overlooks the key drivers of success in modern industries. For companies like Google (GOOGL 0.00%↑) , the bulk of their worth lies in their ability to generate future cash flows from intellectual property and digital products, making Graham’s tangible asset-based valuation method less relevant for assessing their true market value and growth potential.

One of the tenets of Terry Smith’s investment philosophy, a renowned U.K. fund manager who has consistently outperformed the market, is his advocacy for investing in companies with substantial intangible assets. In the Fundsmith’s Owner’s Manual he writes:

“[…] intangible assets, which can be very difficult to replicate, no matter how much capital a competitor is willing to spend. Moreover, it’s hard for companies to replicate these intangible assets using borrowed funds, as banks tend to favour the (often illusory) comfort of tangible collateral.”

Net-Net Stocks in Modern Markets: Scarcity and Challenges

The net-net strategy, popularized by Graham, is a value investing approach where investors buy stocks trading below their net working capital. He meant the stock is priced lower than the company’s current assets minus its total liabilities, indicating that it may be significantly undervalued. Graham described this approach clearly:

“The type of bargain issue that can be most readily identified is a common stock that sells for less than the company’s net working capital alone, after deducting all prior obligations. This would mean that the buyer would pay nothing at all for the fixed assets - buildings, machinery, etc., or any good-will items that might exist.”

While this strategy still holds theoretical value, its practical application has become much more challenging in modern markets.

The scarcity of net-net opportunities today is largely due to increased market efficiency, greater investor awareness, and widespread access to financial data, all of which make it difficult for such deep-value stocks to go unnoticed for long. Companies that do trade at such low valuations are often distressed or facing severe operational challenges, making them inherently riskier.

In today’s environment, investors following Graham’s net-net strategy must often search in small, illiquid markets or distressed sectors. Even then, identifying these stocks requires in-depth research to ensure the companies are not fundamentally broken.

Another limitation of the net-net strategy is its lack of focus on a company’s future growth prospects. While the method prioritizes current assets and liabilities, it tends to overlook growth potential, which is a significant driver of long-term value. This emphasis on liquidation value rather than future earnings may cause investors to miss out on companies poised for recovery or expansion.

Graham’s advocacy for investing in cigar butt companies, those more valuable liquidated than in operation, was effective in the aftermath of the Great Depression. However, as markets have evolved, such opportunities have become scarcer, making it increasingly difficult to consistently profit from this strategy. Investors today must carefully weigh the risks before committing to a net-net strategy, as modern markets present fewer reliable opportunities of this kind.

The net-net strategy, a subset of deep value investing, remains a classic example of Graham’s conservative investment principles. You can read more about the limitations of the net-net strategy in modern markets on an excellent How to Apply Benjamin Graham's Net-Net Stock Valuation Strategy post by StableBread.

Graham’s Subtle Approach to Competitive Advantage

A moat refers to a company’s sustainable competitive advantage that protects it from competitors and ensures long-term profitability. Warren Buffett, a protégé of Benjamin Graham and often regarded as one of the best investors in history, frequently uses the term to describe businesses with durable advantages, such as strong brand recognition, network effects, or cost efficiencies. Buffett famously said:

“The most important thing in evaluating businesses is figuring out how big the moat is around the business.”

He also emphasized the importance of this advantage lasting over time, noting:

“A truly great business must have an enduring ‘moat’ that protects excellent returns on invested capital.”

While Graham didn’t use the term moat, he often referred to factors that align with the concept:

Stability of earnings: Graham placed great importance on a company’s ability to maintain steady earnings over long periods. This focus on stability can serve as a proxy for competitive strength, indicating that a company has a reliable business model and can weather various economic conditions.

Financial strength: Companies with low debt, high liquidity, and solid asset bases are favored by Graham because these characteristics help businesses survive economic downturns. A strong financial position acts as a protective moat, shielding the business from risks.

Industry leadership and market position: Although not explicitly labeled as a competitive advantage, Graham encourages investors to look for companies with strong market positions, particularly those that dominate their industries or have unique strengths that protect them from competitors.

“Each company selected should be large, prominent, and conservatively financed. Indefinite as these adjectives must be, their general sense is clear.”

Although Graham didn’t directly discuss moats or competitive advantages in the way Buffett does, the principles he advocates, financial strength, consistent earnings, and industry leadership, align with the modern concept of moats, which Buffett later emphasized as critical to long-term investing success.

Circle of Competence Before The Term Was Coined

Although Graham did not specifically use the term circle of competence, his investment philosophy laid the groundwork for this concept, which was later popularized by Warren Buffett. The circle of competence refers to the idea that investors should focus on industries, businesses, or sectors they understand deeply, rather than venturing into areas outside their expertise. Buffett explains it succinctly:

“What an investor needs is the ability to correctly evaluate selected businesses. Note that word ‘selected’: You don’t have to be an expert on every company, or even many. You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

Graham’s investment principles closely relate to the circle of competence through key ideas:

Understanding what you buy: One of Graham’s core teachings is that investors should only buy stocks they can thoroughly analyze and understand. This aligns closely with the circle of competence, which emphasizes staying within one’s area of expertise to make informed, rational investment decisions.

Margin of safety: Graham’s principle of the margin of safety is indirectly connected to the circle of competence. By focusing on areas where investors have a deep understanding, they are more likely to correctly estimate the intrinsic value of a business and apply a margin of safety to protect themselves from risk.

Avoiding speculation: Graham warned against investing in sectors or companies that are difficult to evaluate or highly speculative. This is in line with the circle of competence, as it limits an investor’s exposure to areas they may not fully comprehend, reducing the likelihood of making uninformed, speculative investments.

While Graham didn’t use the exact term, his teachings advocate for the careful analysis and understanding of businesses, forming the basis of what Buffett later coined as the circle of competence. As Graham stated:

“The enterprising investor may properly embark upon any security [stock] operation for which his training and judgment are adequate and which appears sufficiently promising […]”

Risks of Initial Public Offering (IPO)

An Initial Public Offering (IPO) is the process through which a private company offers shares of its stock to the public for the first time, allowing it to raise capital from public investors. Once the IPO is complete, the company’s shares are listed on a stock exchange and can be freely traded. This transition allows the company to access larger pools of capital but also requires greater transparency and regulatory compliance.

Graham advises caution when dealing with IPOs, viewing them as speculative and often overvalued. He believes IPOs are typically launched during periods of market optimism when prices are inflated, offering more benefits to the sellers than to the buyers. He highlights that new issues are often pushed aggressively by underwriters, which can lead to poor investment decisions by buyers.

“[…] new issues have special salesmanship behind them, which calls therefore for a special degree of sales resistance.”

He explains that IPOs tend to perform poorly after the initial excitement fades, as many are over-hyped and overvalued. Graham also points out that many IPOs introduced during bull markets are highly speculative, leading to significant losses for investors once market conditions normalize.

“The heedlessness of the public and the willingness of selling organizations to sell whatever may be profitably sold can have only one result - price collapse.”

In summary, Graham advises investors to avoid IPOs, given their tendency to be overpriced and speculative. He underscores the importance of resisting sales pressure and being wary of new issues introduced during optimistic market phases.

Jason Zweig, in his commentary on The Intelligent Investor, offers a witty and succinct take that captures both his and Graham’s views on IPOs with great eloquence:

“Weighing the evidence objectively, the intelligent investor should conclude that IPO does not stand only for ‘initial public offering’. More accurately, it is also shorthand for:

It’s Probably Overpriced,

Imaginary Profits Only,

Insiders’ Private Opportunity, or

Idiotic, Prosperous, and Outrageous.”

Cyclical Nature of IPOs Then and Now

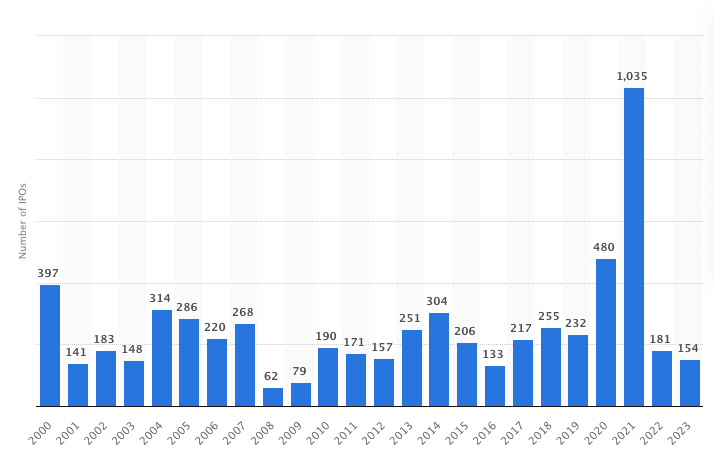

Looking at the number of IPOs in the U.S. between 2000 and 2023, it is clear that Graham's observations remain relevant today. The trend of increased IPO activity during periods of market greed, followed by a sharp decline during periods of fear, is still evident.

For example, between 1997 and 2000, the dotcom bubble fueled a surge in IPOs, peaking at 397 in 2000. This was followed by a dramatic drop in 2001, as the bubble burst. Similarly, the Global Financial Crisis of 2007 and 2008 led to a steep decline in IPO activity, with a notable drop in 2008 and 2009.

More recently, 2020 and 2021 saw a significant surge in IPO numbers. This surge was driven partly due to historically low interest rates and Quantitative Easing (QE) measures introduced by central banks like the Federal Reserve in the U.S., which injected liquidity into the markets and reduced borrowing costs. As a result, companies found favorable conditions to go public, leading to the largest spike in IPOs in over two decades.

Conclusion

While Graham’s investment principles remain a cornerstone of value investing, the modern market presents new complexities and opportunities that require adaptation. Graham’s emphasis on a margin of safety and conservative stock selection has proven timeless, yet today's level-headed investors must also account for the evolving nature of businesses, particularly the rise of intangible assets and innovative business models that dominate sectors like technology.

As we’ve explored, combining Graham's foundational wisdom with a forward-looking approach, including estimating future cash flows and the growth potential of companies, can help investors navigate modern markets more effectively. This intersection of growth and value investing highlights that, in many cases, growth stocks can indeed be value stocks when viewed through the lens of long-term potential.

Whether evaluating the effects of behavioral biases, embracing the simplicity of index funds and ETFs, or understanding the decline of net-net stocks and IPO risks, Graham’s teachings continue to guide investors toward making sound, rational decisions. However, to thrive in today’s economy, investors should adapt these principles to account for new dynamics such as scalability, intangible assets, and rapid innovation.

By applying a balanced approach, rooted in fundamental analysis yet forward-looking enough to capture growth opportunities, today’s investors can honor Graham’s legacy while evolving their strategies to succeed in an era driven by technology and innovation.

I remain deeply committed to fundamental analysis and have drawn inspiration from Graham and other legendary value investors as my mentors. However, I recognize that my investment philosophy will continue to evolve, perhaps significantly, over time. In this post, I’ve shared some reflections after reading The Intelligent Investor, and I hope they inspire critical thinking in your own investment journey. If you haven’t yet read my initial review of the book, you can find it by clicking the link below.