Constellation Software (CSU.TO) Q1 2026 Results: The Market Feared AI; Constellation Deployed $1.6 Billion

Why record capital deployment, an unchanged bonus plan, and broad insider buying are the disciplined-acquirer playbook running exactly as designed

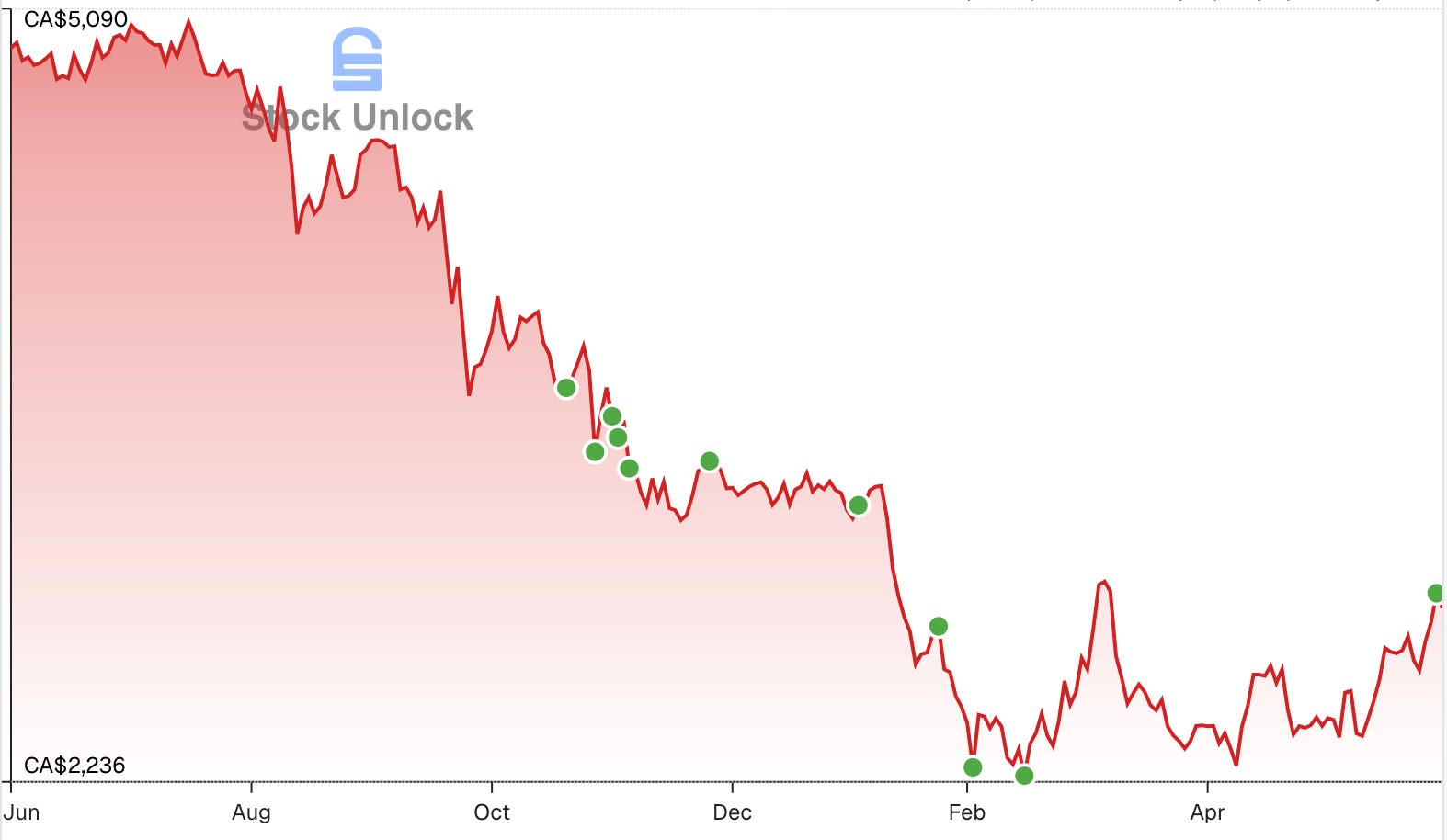

Constellation Software, Inc. (CSU.TO) posted Q1 2026 results (press release) on May 12, 2026 and the results were strong. The market had spent the prior year pricing CSU as if AI were about to hollow out vertical market software (VMS). The stock fell from C$5,060 in June 2025 to a C$2,196 low in January 2026 - its deepest drawdown ever, more than 50% peak-to-trough - on two fears I covered in my previous CSU article on February 2026: the “SaaSpocalypse” and Mark Leonard’s September 2025 succession.

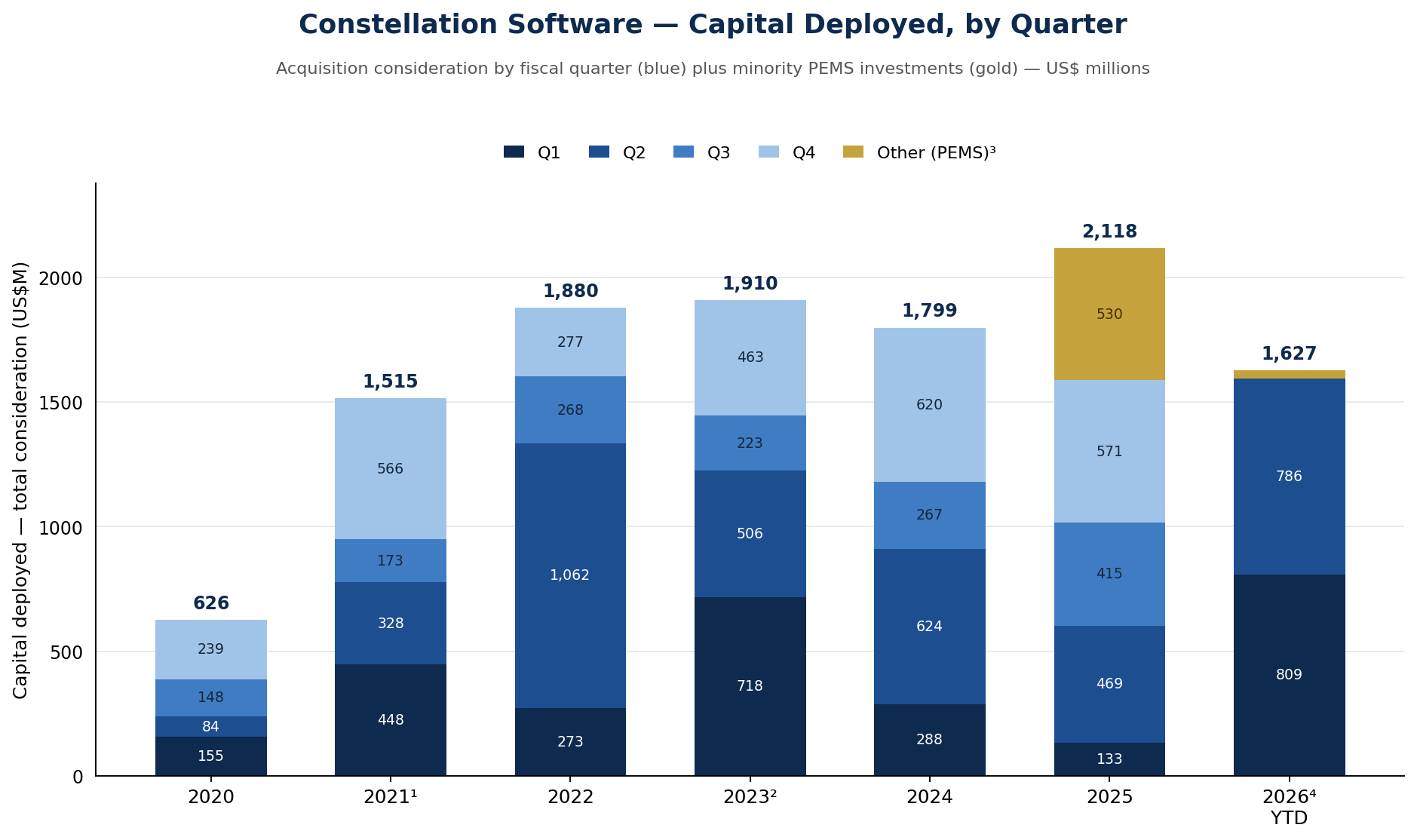

Q1 2026 is the first clean quarter to test that fear against the cash, and the cash did not cooperate with the bears. Against Q1 2025, free cash flow available to shareholders (FCFA2S)1 rose 44% to a record $733 million and operating cash flow rose 9% to $897 million; against Q4 2025, revenue was flat ($3,181 million vs $3,177 million) while management stepped up capital deployment to $809 million, with another $786 million already committed for Q2. This is the quarter the model is built for: when public software multiples crack, a disciplined acquirer’s job is to get more capital out at better prices, which is exactly what happened.

Q1 2026 Highlights

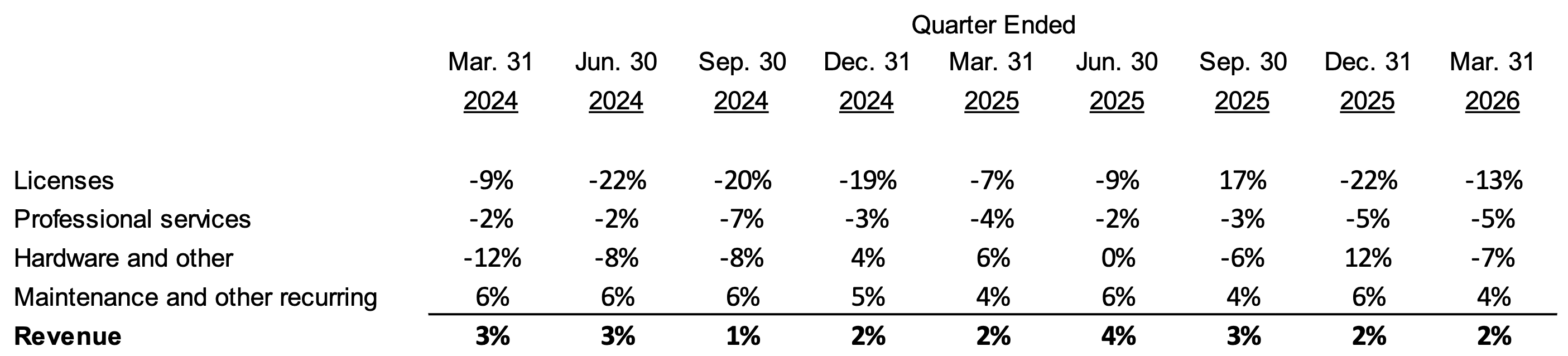

Quarterly revenue $3,181 million, +19.9% YoY / flat QoQ; recurring maintenance $2,444 million (77% of revenue), +9% organic.

Record Q1 cash flow: FCFA2S $733 million (+44% YoY, +73.3% QoQ); OCF $897 million (+9% YoY, +13.8% QoQ); TTM FCFA2S $1,905 million (+23.7% YoY).

Deployment stepped up: $809 million of acquisitions in Q1 (vs $571 million in Q4 2025), plus $786 million committed for Q2; $1.6 billion in motion year to date (YTD).

Private prices held: Constellation’s low-end acquisition costs didn’t fall with public stocks, even as its own share price was cut in half.

Owner behaviour: bonus plan unchanged, managers still buying CSU in the open market; the CFO called the sell-off “a great buying opportunity”.

Fortress balance sheet: net debt fell QoQ to $979 million (from $1,043 million), about half the annualized FCFA2S.

Q1 2026 Lowlights

Organic revenue growth is soft: 6% reported organic is just 2% FX-neutral. Flat YoY and QoQ; the headline is an FX effect.

Margins slipped (expenses 76% of revenue, +1% YoY): the Q1 acquisition cohort ran at negative margin, plus payroll-tax seasonality and R&D/S&M/G&A step-ups.

Organic laggards: Lumine (-2% FX-neutral) and Altera (-13%) shrank; Synchronoss adds dilutive, low-margin revenue to the mix.

Scorecard drift: as minority PEMS2 stakes grow, FCFA2S captures less of the economics; management may change the headline metric.

Big deals still pricey: large-deal competition is “still fierce”, high-end private valuations only “plateauing”.

Maintenance Is the Number Leonard Told Us To Watch

I weight the maintenance line because it is the test founder and former President Mark Leonard taught CSU shareholders to apply. In the 2015 President’s Letter:

“One of the concerns with acquisitive companies is that some of them grow revenues and adjusted earnings but impair the underlying value of their intangible assets. In essence what purports to be a return on capital is really a return of capital […] as long as the [Maintenance] base is growing organically, the value of the business is growing and our shareholders are getting a return on capital, not of capital.”

It is trivial to manufacture revenue by buying businesses; the honest question is whether what you already own is still alive. Organic maintenance growth is the “lie detector”, and Q1 passes: maintenance grew 4% organically currency-neutral (9% reported), inside the 4-6% band it has held for years.

The base is compounding under its own power, so the cash CSU harvests is a return on capital, not of it. That is why the soft +2% consolidated organic figure doesn’t worry me.

Three Sub-Fleets: Who’s Pulling, Who’s Dragging

Constellation discloses supplemental figures for its listed subsidiaries Topicus (TOI.V) and Lumine (LMN.V), and for Altera (the 2022 Allscripts hospital carve-out):

Topicus is the organic standout; Lumine shrank while it is digesting the Synchronoss acquisition; Altera remains the problem child at -13%, the clearest case of an acquisition not yet earning its keep. None of this is alarming - Altera is ~5% of revenue, and grinding up underperformers is the part of the disciplined framework, but it is a fair counter-weight to the “everything compounds” framing.

The Real Headline: Deploying Into The Fear

Constellation closed $809 million of acquisitions in Q1, up from $571 million in Q4 2025, and has already committed a further $786 million for Q2 - nearly $1.6 billion across two-dozen-plus verticals. The largest was Synchronoss (via Lumine, Feb 13, $309 million; quarterly pro-forma accretion: $22 million revenue and a $2 million loss in its stub).

Put the $809 million in historical context and the picture sharpens: it is the most Constellation has ever deployed in a first quarter, and Q1 has historically been its quietest window (2025’s was a meager $133 million). The whole of 2026 is already running hot - the $786 million committed for Q2, with the quarter barely half over, is on its own larger than most prior full-year second quarters. This is the acquisition engine throttling up exactly as public market fear peaks: the behaviour you want from a serial compounder when its inputs get cheap.

¹ Q1 2021 - the Topicus.com B.V. quarter is not split into cash/deferred/share in the press release; the $448 million total includes Topicus share/unit consideration.

² Q1 2023 - includes $222 million of share-based consideration (CSI Special Shares for WideOrbit, via Lumine). The four quarterly headlines sum to $1,910 million versus CSI’s reported full-year acquisitions of $2,609 million: the $699 million gap being additional WideOrbit/Lumine share consideration.

³ Other (PEMS) - Permanent Engaged Minority Shareholder investments (minority equity stakes), shown as annual net figures; the 2025 block is the $530 million Asseco Poland (ACP.WA) stake. The Sabre (SABR 0.00%↑) PEMS stake is disclosed but not quantified in the filings.

⁴ 2026 YTD: Q2 is partial ($786 million completed or committed Apr 1-May 12, 2026); the gold sliver is the $32 million Q1 “purchases of investments” line.

With public software stock prices cratering, are private sellers cheaper? Chief Investment Officer Bernard Anzarouth addressed the question during the earnings call:

“At the high end, we could see it maybe plateau a little bit, if not declining slightly, but at the low end where we play, with most of our acquisitions, not at all.”

President Mark Miller added:

“There’s a real disconnect between the SaaSpocalypse publicly traded stuff and private markets.”

The panic that handed me a 50%-off high-quality compounder did not lower the prices CSU pays for the small businesses it buys.

When asked about bonus plan at Constellation, CFO Jamal Baksh replied:

“So we haven’t made any changes to the plan. Me personally, I’d say this is a great buying opportunity […] We still buy shares in the market, same way we always have.”

Hearing the CFO call his own falling shares a buy confirms my valuation. It isn’t just talk, the insider filings corroborate it.

Through the depths of the sell-off, with the stock languishing around CA$2,385 (less than half its 2024-2025 peaks), a broad sweep of insiders bought CSU on the open market. That is the bonus plan working as designed: Constellation requires senior staff to take a portion of their cash bonuses and buy CSU in the open market, then hold for years, so the same fear that compressed the price multiple turned management’s own pay into a purchase at lower prices. It lands cleanly because Constellation is non-dilutive, the share count is unchanged at 21.2 million since Q1 2007, there is no buyback program and no stock-based compensation, so every insider purchase is real cash in, not optics. One insider, Barry Symons, sold CA$35.2 million on March 27, a single large sale that can reflect diversification or tax as easily as a view on value, but the weight of the activity runs one way, alongside the M&A.

The Cost Of Buying: Margins

Buying a pile of underperformers in one quarter has a cost. Expenses rose to 76% of revenue, +1% YoY. Baksh:

“[…] the Q1 cohort of acquisitions themselves were actually a negative margin for the quarter, which we totally plan to improve them, and it’s a typical thing where we improve margins over time, but it was a bit of a bigger drag this quarter than previous quarters.”

Three forces: the unoptimized new businesses (Synchronoss and the cohort); CSU’s perennial Q1 payroll-tax spike on March bonuses; and a real investment step-up: R&D staff +18% ($459 million), sales & marketing +26% ($210 million), G&A +33% ($361 million). It is the predictable shape of an acquisitive quarter, not a structural crack. It is why FCFA2S is where the quality shows this period.

The AI Question Answered Like An Operator

Asked to sort the portfolio into “AI-safe” and “AI-exposed” buckets, Miller refused the tidy taxonomy. He said:

“It’s a beauty-is-in-the-eye-of-the-beholder situation […] it depends on the addressable market size of that niche and how defensible it is and how close they [business leaders] are to their customers.”

On where the real threat lives: “Where you’re gonna get attacked by AI […] is going to be maybe where you least expect it”, noting the highest-risk “high churn, high attrition” profile “isn’t a large percentage of our recurring revenues”. On the moat in plain words:

“Rarely we lose customers on pricing because the switching is painful […] Where you lose customers is when the competitor can provide something much different than you can provide that the customer really needs.”

Miller frames AI as offense - “an opportunity to do more for customers” - consistent with Leonard’s view that AI augments rather than replaces. Honest, not dismissive: diffuse AI exposure across hundreds of sticky niches, plus a culture that pushes the adaptation call down to each leader, is the strategy.

Balance Sheet And a Quiet Change To The Scorecard

A fortress dressed as a leveraged company: cash $3,010 million against $3,990 million of debt, net debt of $979 million - down from $1,043 million at year-end and roughly half of TTM FCFA2S. Recourse debt at the parent is $1,480 million (investment-grade, revolver3 undrawn); the rest sits non-recourse inside Topicus and Lumine, while they hold $1,095 million of cash on the balance sheet. The negative working-capital float grew: deferred revenue jumped $676 million (+30.5%) QoQ to $2,891 million.

The forward signpost came on minority equity investments: Constellation’s PEMS strategy of selective, long-term, engaged minority stakes (such as its position in Asseco Poland or Sabre, where CSU now holds a board seat) that complement the acquisition model. Baksh confirmed the hurdle rate is unchanged and flagged that FCFA2S “doesn’t pick up anything” from these, and that management may disclose an “economic net income” measure to capture CSU’s share of investee cash flows. The yardstick may evolve from FCFA2S - I will be monitoring as PEMS scale.

The strategy also reframes the succession story. On March 27, 2026, Constellation announced its founder and former President Mark Leonard, who stepped down as President in September 2025, will not stand for re-election to the board, ending his term after the May 15 Annual General Meeting (AGM). He stays on as an advisor, with a stated focus on the PEMS strategy. After last year’s succession scare, that is about the gentlest possible exit: the operating philosophy is institutionalized under Mark Miller, and the one capital allocation area still being built out keeps its architect close.

Valuation: How Cheap is CSU Stock?

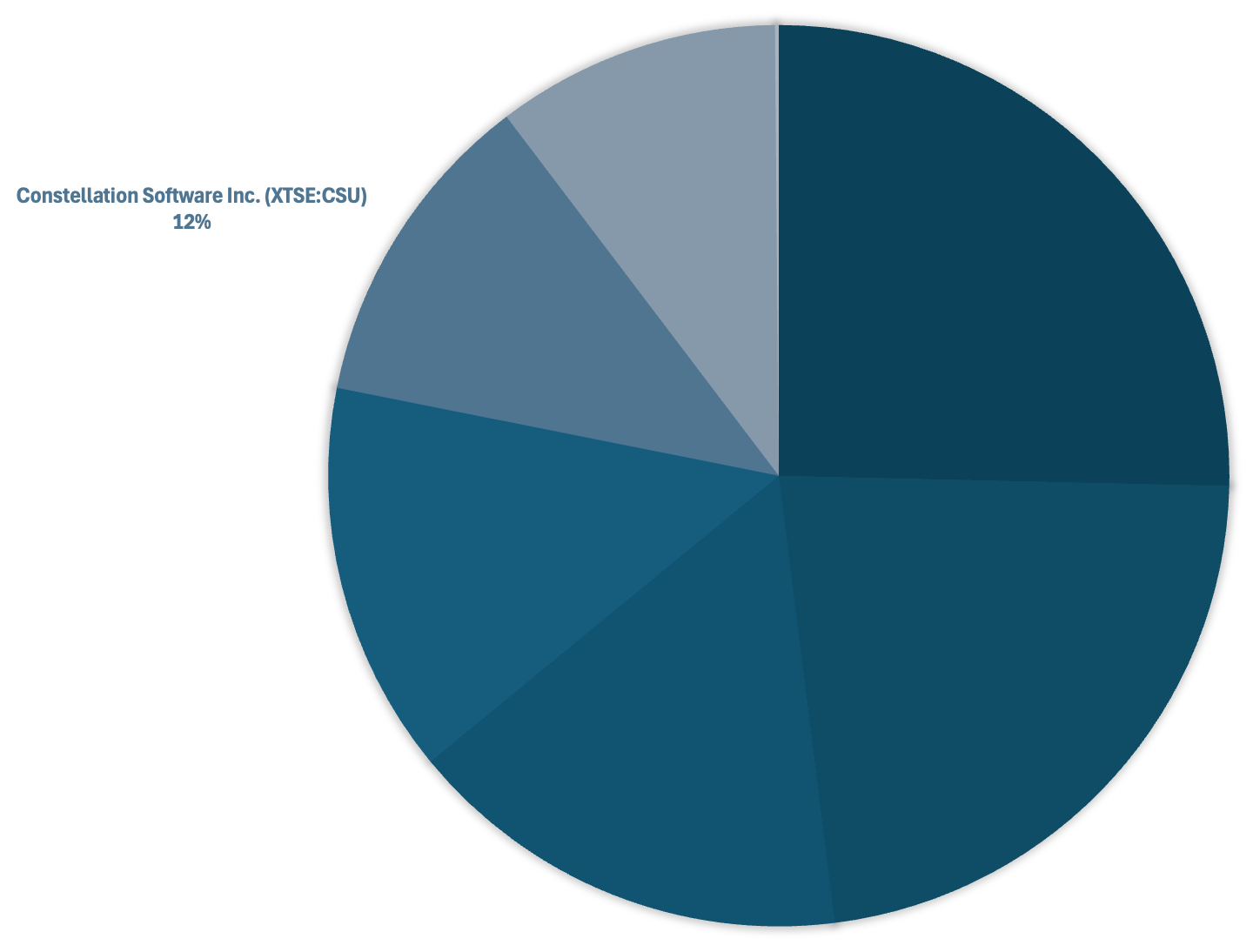

I built the position from October 2025 into the AI panic and Leonard-succession wobble, adding throughout the pullback and taking it from 8% in February to 12% of my portfolio.

My thesis was never that AI is harmless to software companies as a whole; it is that the market applied one lurid narrative to a federation of hundreds of niche businesses and handed me a 30%-off entry price in October 2025 from its peak on one of the best capital allocators of the last two decades. I value CSU as it asks to be valued - on cash to owners (FCFA2S), not amortization-distorted income.

At June 1, 2026’s price of C$2,931.96 (≈ US$2,118.24 at 1.38 USD/CAD), 21.192 million shares give a market cap of US$44.9 billion - 23.6x TTM FCFA2S ($1.9 billion) and 16.4x TTM free cash flow ($2.7 billion). For a business compounding FCFA2S at 17.1% yearly between 2018 and 2025, deploying every dollar above a 20%+ hurdle, issuing no stock, and run by managers paid in cash bonuses used to buy their own shares, the price multiple is undemanding; well below the low-30s it commanded at the 2024 peak, and implying a forward return above my 10% hurdle if the business keeps converting cash into more cash. I won’t pretend a precise intrinsic value; the point is simple - a below-average multiple for an above-average compounder.

Final Thoughts

The public fear that halved CSU stock never reached the private market where the business buys; the recurring base still grows organically; FCFA2S hit record highs; and management met cheaper valuations the only sane way: by deploying more, faster, while calling its stock a buy.

What would change my mind: FX-neutral organic growth turning persistently negative (2% is fine; sub-zero means the base is eroding); cash conversion deteriorating, with FCFA2S substantially lagging revenue growth; disclosure quality slipping as PEMs grow; and evidence AI is graduating customers out of the mission-critical core. None is flashing today. The opposite is: a great business on sale, buying more of what made it great.

My conviction is unchanged; the temporary stock price discount is a gift.

Free Cash Flow Available To Shareholders (FCFA2S), Constellation’s non-IFRS measure: operating cash flow less debt and lease interest, lease repayments, the IRGA revaluation charge, and CapEx, plus interest and dividends received, then net of the minority-interest share. It approximates the uncommitted cash owners could take out before any acquisitions, investments, or debt repayments.

Permanent Engaged Minority Shareholder (PEMS) strategy: Constellation’s new capital deployment initiative designed to buy influential non-controlling minority stakes in larger public software companies, held to the same return hurdle as its buyouts.

Revolving credit facility: a committed bank line a company can draw down, repay, and redraw as needed (like a corporate credit card). Constellation’s is a $1,085 million unsecured facility, undrawn at quarter-end. It’s available borrowing capacity, not debt currently owed.