Alphabet Inc. (Google) Takes Both Sides Of Its Balance Sheet To Market

Self-fund, borrow, or dilute. Alphabet just walked through all three to fund upwards of $190 billion AI build-out

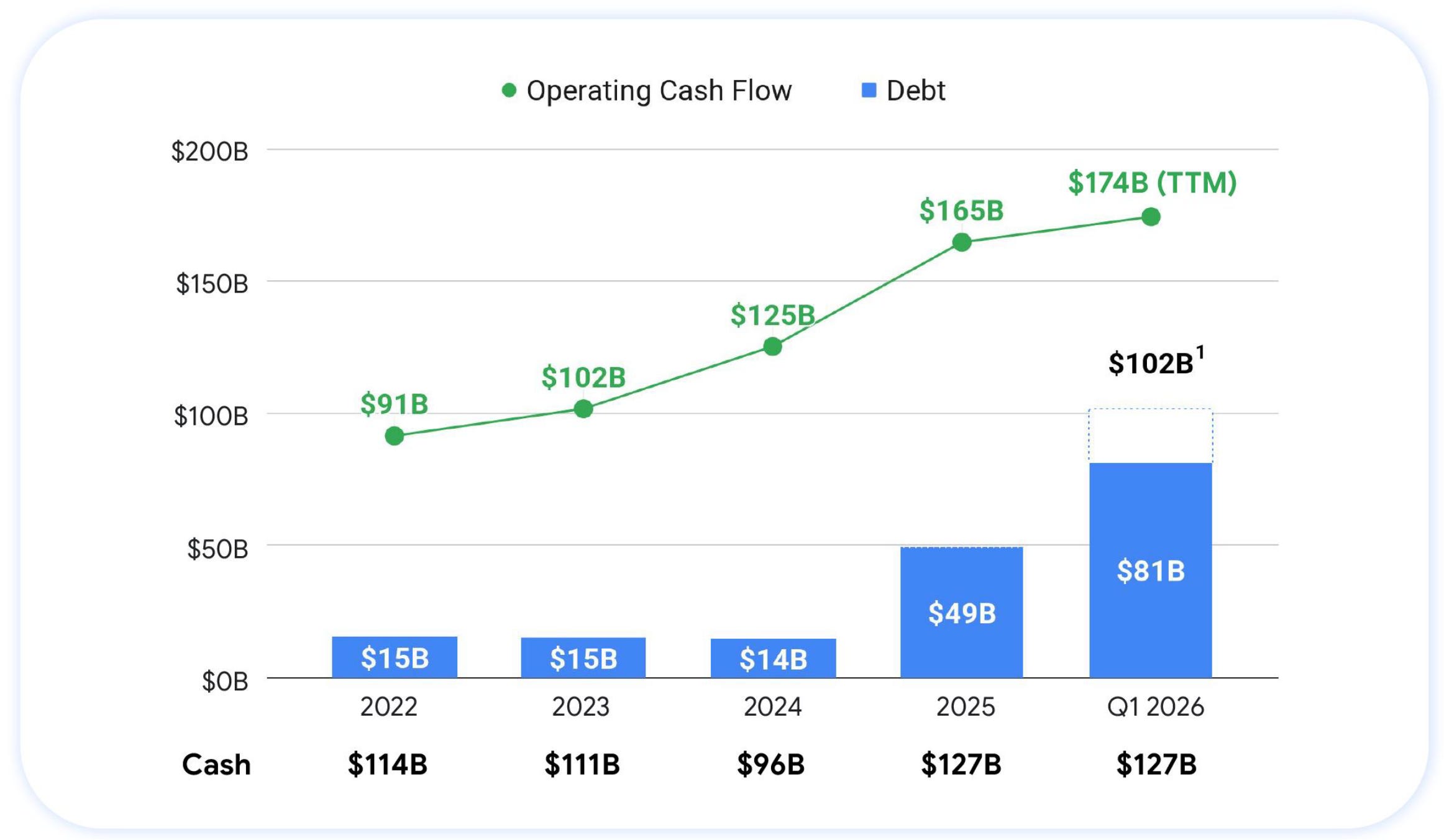

In eighteen months, Alphabet’s (GOOGL 0.00%↑) balance sheet has gone from $12 billion of long-term debt, essentially unleveraged, to over $102 billion of total debt across six currencies, including a 100-year Sterling note maturing in 2126. Then, in the first week of June 2026, it did something no company of this profitability has ever done: it went to the equity market, pricing an $84.75 billion raise, upsized from a planned $80 billion as demand poured in, anchored by a $10 billion Berkshire Hathaway private placement. The sequencing is the story. Alphabet term-funded the AI build-out in the bond market first, while credit was cheap and long, and took the equity window ahead of the OpenAI and Anthropic raises, absorbing a finite pool of AI-allocable capital before its competitors can reach it. All-in dilution: 2% of shares outstanding for capital equal to about half a year of CapEx. The shift from capital-light advertising monopoly to capital-heavy AI infrastructure platform is complete, and the balance sheet has become a competitive weapon.

One frame to hold before the numbers. Any company racing to build AI compute can pay for it only three ways: spend the cash it already generates, borrow it, or sell a piece of itself. For a business like this, the third is supposed to be the last resort - Alphabet holds $126.8 billion of cash, threw off $174 billion of operating cash flow (OCF) over the past year, and borrows more cheaply than almost any company alive. Companies in that position buy their own stock back; they do not sell it, because equity is the most expensive money there is, a permanent claim on every future dollar of profit. That Alphabet sold $84.75 billion of stock in two days, about the same amount of the largest IPO in history (SpaceX’s ~$85.7 billion) raised, is the tell. The build-out has simply grown large enough to need all three doors at once; this article walks through each.

Two Decades Of Near-Zero Debt

For most of Google’s life as a public company, and Alphabet’s, after the 2015 reorganization, the balance sheet looked like a software company’s. Cash piled up faster than the business could redeploy it; capital returns came through buybacks and, eventually, dividends. Going into 2025, long-term debt was $12 billion at face value1 ($10.9 billion carrying2), from just two vintages3: $2 billion of 2016 notes at 2% and $10 billion of 2020 notes at 0.45-2.25% (Note 6. Debt, of the 2025 10-K). Against $95.7 billion of cash and marketable securities at year-end 2024, debt was 11% of its cash and securities. The bond market was a non-factor. That posture has now ended.

The Debt Book: From $12B To $102B

Fast forward from year-end 2024 to Q1 2026 and Note 6 of the Q1 2026 10-Q lays out the long-term notes4. The June 3 investor presentation (slide deck) added the post-quarter issuance that takes total debt to ~$102 billion.

Coupon: stated annual rate on face value.

Effective rate: cost of the debt, reflecting proceeds received net of discount and issuance costs.

Face value: principal repayable at maturity, before discount and costs.

¹ Foreign-currency notes; carrying value moves with FX.

² Issued after Q1 2026; per the June 3 “Robust Financial Foundation” slide (€9 billion + C$8.5 billion + ¥576.5 billion ≈ $20 billion). USD equivalents approximate; coupons and maturities will appear in the Q2 2026 10-Q.

The legacy book is the top two rows and little else - at sub-2.25% coupons, a zero-rate relic; everything beneath was raised in barely a year, $69.3 billion of new face value at materially higher coupons. The Q1 2026 tranche was the largest quarter in the company’s history and the widest on currency - $20 billion in dollars (4.8% weighted coupon), £5.5 billion in sterling (5.31%, out to 2126), and CHF3.1 billion in Swiss francs (1.06%, the cheapest term money Alphabet has ever locked); and May’s ~$20 billion add-on stretched the reach again into Canadian dollars and Japanese yen, the fifth and sixth funding currencies. Much of that foreign-currency debt also doubles as a net investment hedge ($19.6 billion designated at Q1), dampening FX volatility rather than merely chasing cheaper coupons. The maturities run 2026 to 2126, weighted to the long end by design - only $2 billion falls due this year, the rest pushed out to match the depreciable life of the assets it funds.

The buffer behind the long-term debt is intact - a $25 billion commercial paper program undrawn, $11.7 billion of credit facilities with $1.2 billion used. The proceeds trace cleanly to capital allocation: the 2025 notes funded the $70 billion buyback, the Q1 2026 notes the Wiz ($29.5 billion) and Intersect ($5.9 billion) closes.

Rolled forward across the balance-sheet dates, the build looks like this:

Fair value of notes (Level 2): estimated market value of the notes, derived from observable market prices of comparable instruments; sits below face value when prevailing rates have risen since issuance.

¹ Net proceeds from the two underwritten offerings plus the Berkshire Hathaway private placement: ~$17.8 billion of common stock + ~$16.6 billion of mandatory convertible preferred + $10 billion from Berkshire ≈ $44.4 billion.

² Illustrative pro-forma net cash, laying the June raises onto the Q1 balance sheet: $49.3 billion Q1 net cash + ~$44.4 billion equity proceeds (the ~$19.6 billion May debt adds equally to cash and debt, so it nets out) ≈ ~$93.7 billion. Assumes proceeds simply add to the Q1 cash balance; actual cash will be drawn down by subsequent CapEx and M&A.

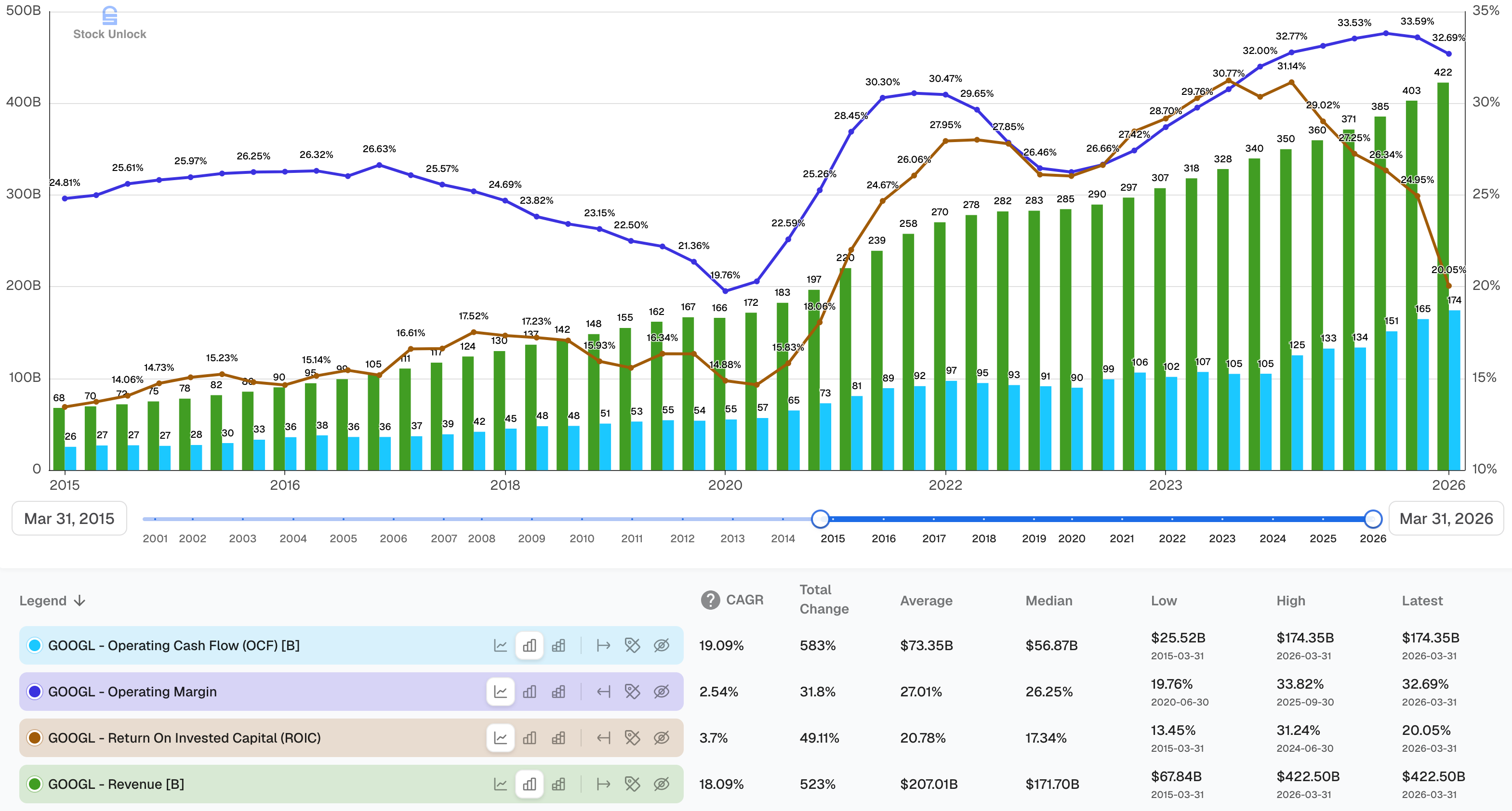

Per the investor presentation’s “Robust Financial Foundation” chart, operating cash flow nearly doubled from $91 billion (2022) to $174 billion, but annual CapEx ran from $31 billion to a guided $180-190 billion - a more-than-sixfold jump, “six times larger than 2022 and double last year’s”, as CEO Sundar Pichai put it. The internal engine grew; the opportunity grew faster.

Liquidity, Headroom And The Commitments Iceberg

Alongside the notes, as of Q1 2026, Alphabet keeps substantial unfunded liquidity: $11.7 billion of credit facilities ($1.2 billion drawn), a $25 billion commercial paper program ($0 outstanding), and $126.8 billion of cash and marketable securities - flat with year-end 2025 despite $33.6 billion of acquisition cash and $35.7 billion of CapEx in the quarter. This is not a balance sheet under stress.

It is also being “funded” off the supplier side: the cash flow supplemental shows $24.1 billion of property and equipment sitting unpaid in payables and accruals at quarter-end, against $11.4 billion a year earlier - effectively “interest-free vendor financing” of the CapEx ramp. Operating lease liabilities barely moved, ~$12.7-13 billion: Alphabet is owning and finance-leasing its capacity, not renting it.

The fuller picture sits in the commitments footnotes, where the off-balance-sheet obligations have grown faster than the debt. Note 5 (Variable Interest Entities5) shows future funding commitments jumping from $1.1 billion at year-end 2025 to $40.7 billion at March 31, 2026 - driven by the March commitment to a $40 billion private company investment, $10 billion firm and $30 billion contingent on milestones through 2030. The 10-Q does not name the company; Bloomberg reported it as Anthropic, with Alphabet investing $10 billion at a $350 billion valuation and up to $30 billion more tied to milestones - an arm’s-length stake in a direct Gemini competitor and Google Cloud customer at once. The 10-Q also shows $332.4 billion of purchase commitments ($138 billion short-term), chiefly technical infrastructure supply agreements and energy contracts, plus $9 billion of financial guarantees6 and $28.4 billion of credit-derivative backstops7 supporting third-party data-center and power entities.

None of this is debt; all of it is a claim on future cash flow. The forward obligation profile is the $102 billion of bonds plus ~$410.5 billion of committed and contingent claims ($332.4 billion of purchase commitments, $40.7 billion of VIE funding commitments, and $37.4 billion of guarantees and backstops), the context in which the June equity raise stops looking surprising and starts looking arithmetically necessary.

June 2026: The Equity Side Activates

On June 3, 2026, alongside the investor presentation laying out the rationale, Alphabet priced an $84.75 billion equity capital raise “to expand AI infrastructure and compute” - upsized from a previously announced $80 billion target after demand poured in. To my knowledge, this is the largest equity raise ever completed by a public company, ahead of Petrobras’s (PBR 0.00%↑) $70 billion 2010 share sale.

The structure has four parts, and the structure matters more than the headline:

$18 billion of underwritten common stock (upsized from $15 billion), closing June 4; ~$17.8 billion net.

$16.75 billion of 6.25% mandatory convertible preferred (upsized from $15 billion), sold as depositary shares listing on Nasdaq as GOOGM and GOOGN, converting into common around May 15, 2029; ~$16.6 billion net.

A $10 billion private placement to Berkshire Hathaway, adding to the position Berkshire has built since Q3 2025.

A $40 billion at-the-market (ATM)8 program starting Q3 2026, of which $30 billion is earmarked to fund employee RSU tax obligations on a “sell-to-cover” basis (more on this later).

Proceeds go to general corporate purposes, including CapEx, against 2026 guidance of $180-190 billion and 2027 “significantly higher”. The investor presentation framed the equity raise as one of three funding legs: $174 billion of TTM operating cash flow, debt (covered above), and “today’s equity offering”.

The Spend Is Pulled By Demand, Not Pushed By Hope

The justification for spending above operating cash flow is that demand is running ahead of capacity, not the other way around. Pichai has been explicit that the binding constraint is compute, not customers: “The top question is definitely around capacity”, he said in February 2026, citing power, land, and supply-chain limits, with Google turning away cloud workloads it cannot yet serve. The investor presentation put it plainly - demand for Alphabet’s AI products and services is “meaningfully exceeding our available supply”. That is the line between expansion financing and deficit financing: Alphabet is raising because the opportunity outran the cash engine, not because the business is weakening. The contractual evidence sits in the footnotes - a $462 billion Cloud backlog, roughly half to convert within 24 months, and the $40.7 billion committed into the Anthropic-linked VIE.

Whether that capital earns its return comes down to the moat. A neocloud can rent GPUs; almost no one else owns the whole stack - TPUs, network, security, Gemini, and distribution across billion-user products - which lets Alphabet drive inference costs down (Gemini serving costs fell 78% in 2025) and monetize the same compute across Search, Cloud and subscriptions at once. That integration is why a 20%+ ROIC can survive a fast-growing capital base: the returns are defended by more than being first to spend.

Debt First, Equity Second: The Sequencing Is The Strategy

Here is why I am bullish on the move rather than alarmed by it. A company funding a multi-hundred-billion-dollar investment cycle has two external capital markets, and they deplete at different rates. Alphabet worked them in the correct order.

It went to the bond market first, and went long. A century bond is less a financing decision than a statement about duration: Alphabet locked in the price of money for the entire depreciable life of several generations of data-centers, while spreads were tight and before AI issuance from every hyperscaler and neocloud could saturate demand. Stacking another $80+ billion of bonds on top would have pushed total debt toward $180 billion, pressured the credit rating, and leaned on a market already tiring of AI paper.

Then it turned to the equity market, before its competitors could. In the coming months the private AI complex comes to market in size - OpenAI and Anthropic each discussing to raise ~$100 billion - and it is not only the AI labs: the other hyperscalers are pushing CapEx past their own cash flow too, with Meta’s (META 0.00%↑) shares falling 7% in early June on a mere rumor it might issue equity. The pool of capital willing to fund AI is enormous but finite, and Alphabet jumped the queue - every dollar into GOOGL, GOOG, GOOGM and GOOGN this month is a dollar no longer waiting for competitors’ roadshow. The strike is twofold: it funds the build-out on the best terms available and raises the cost of capital for everyone trying to out-build it. Alphabet did not need equity to survive; the private labs must raise or stop training their models. They will reach the window partially drained, facing a profitable alternative that has compounded revenue 18.1% and OCF 19.1% for a decade, accelerating to 31% last year. That asymmetry - raising opportunistically versus out of necessity - compounds over a capital cycle.

Warren Buffett described the ideal business during the 2003 Berkshire Hathaway annual meeting:

“The ideal business is one that earns very high returns on capital and could keep using lots of capital at those high returns. I mean that becomes a compounding machine.”

For two decades Alphabet was only the first half of that sentence - spectacular returns, more cash than it could redeploy, hence the buybacks. The AI cycle flipped the equation: for the first time, Alphabet has more high-conviction reinvestment opportunity than internally generated cash. A business crossing that threshold should raise external capital.

One caveat on reading the $10 billion Berkshire anchor as a Buffett blessing: this is Greg Abel’s Berkshire - Buffett handed over as CEO at the end of 2025 - and a tech compounder at a decade-high multiple is more the successor regime’s style than old Berkshire’s cash-hoarding caution. The framework still applies; the vote of confidence is today’s Berkshire’s, not Buffett’s personally.

Management’s Own Framing: ROIC, Prudent Leverage, And A “Proactive” Move

During the investor presentation, Ashkenazi opened by promising to explain “how our capital investments are informed by our view of ROIC9”. Three points in her remarks matter for this thesis.

First, the leverage philosophy. Ashkenazi framed prudent leverage, robust liquidity and access to multiple funding sources as a deliberate, strategic component of Alphabet’s long-term plan - explicitly tied to “the scale and capital intensity of the current opportunity”. On capital allocation - the part of management quality I weight most heavily - she stressed a framework that “prioritizes investments in organic growth, while balancing strategic M&A, investments, and capital return to shareholders”. Organic growth first, buybacks second: that is the honest answer to anyone asking why the $69.5 billion still available under the April 2025 buyback authorization (Note 11) sits idle, and it frames the multi-currency note program and the equity raise as one integrated strategy, not two improvisations. On timing, management called the raise “a strategic proactive move to optimize our financial flexibility” - proactive, not reactive; the company’s own word for reaching the markets ahead of need.

The ROIC framing deserves its own line, because it is the discipline I most want attached to a $180+ billion CapEx guide. Ashkenazi tied the spend explicitly to returns: the Q1 results, she said, are “proof points of our relentless focus on ROIC including our efficiency efforts, a robust resource allocation framework, and a strategic commitment to balancing near-term returns with investments in future innovation”. The efficiency behind that claim is concrete - Pichai noted Alphabet “reduced Gemini serving costs by 78%” in 2025, and Ashkenazi flagged a further 30%+ cut in the cost of core AI responses since Gemini 3. Cheaper inference is what turns a capital-intensity story into an ROIC story; it is the mechanism by which heavy CapEx can earn its keep rather than merely depreciate. For the segment-level economics underneath this - Cloud’s margin inflection, the $462 billion backlog, Services at a 45.3% operating margin - see my Q1 2026 results write-up.

The Share Dilution Math

“Dilution” is the word doing the emotional work in the bearish takes, so let us put numbers on it. Against 12,116 million shares outstanding at March 31, 2026: the underwritten common adds ~50.9 million shares, the Berkshire placement ~28.6 million, the converts ~38-47 million in 2029 depending on the stock, and the $40 billion ATM ~113 million over time. All in: ~230-240 million shares, ~1.9% of the share count, for $84.75 billion of gross proceeds - half a year of CapEx, or about $7 per existing share.

The ATM is not new dilution in economic substance. The RSU program already dilutes shareholders every quarter; until now, Alphabet settled employees’ vesting taxes in cash - $5.5 billion in Q1 2026 alone, per the cash flow statement, tracking toward ~$30 billion for the year. The new mechanism issues shares for equivalent proceeds instead of draining cash. The dilution was always there, buried in the financing section; the ATM moves it onto the share count where everyone can see it, and frees $30 billion a year for the build-out. Optically worse, economically identical.

The preferred is cheap three-year money. The 6.25% dividend on $16.75 billion costs ~$1 billion a year through May 2029, payable in cash or stock. Notice that Alphabet’s three-year convert carries almost exactly the same coupon as its 100-year sterling bond (6.125%). A market that charges the same for three years of equity-linked paper as for a century of unsecured credit is not a market worried about this company.

The issuance is the value-accretive side of a cycle that began with buybacks. Alphabet spent years repurchasing stock far below $350 - borrowing sub-5% to do some of it - and is now issuing at a decade-high valuation of 25.9x P/OCF versus an 18.4x ten-year average (28x forward P/E). Issuing equity only pays when the stock is expensive, and Alphabet’s plainly is - the instructive contrast is Meta, at 12.1x P/OCF, for which a raise at these levels would torch shareholder value. Buy low, sell high applies to a company’s own shares too - retire equity when it is cheap, issue it when it is dear, fund the gap with century-length fixed-rate debt: that is owner-operator behavior, the inverse of issuing cheap stock to fund expensive promises.

The honest counterweight: the per-share compounding tailwind from share-count reduction has not just paused (zero Q1 repurchases, the $69.5 billion remaining under the April 2025 buyback authorization sitting unused), it has temporarily inverted. That puts a clock on the deployment: the AI capital must produce OCF growth meaningfully above the 2% dilution drag, or the exercise subtracts per-share value. At the current 31.5% TTM OCF growth, it clears that bar by a factor of fifteen.

The Bear Case, And What Would Change My Mind

The skeptics are not crazy, and three of their arguments deserve a hearing. First, no moat: critics argue every lab is building similar models on similar data, so AI will not be winner-take-all the way Search was, and Google is overspending into a commoditizing market. Second, bubble: a cash-rich company selling equity near all-time highs to fund CapEx - weeks before OpenAI, and Anthropic come to raise - looks to some like late-cycle exit liquidity. Third, dilution at the top: if the AI returns disappoint, issuing 2% of the company will read as value destruction in hindsight.

My responses, briefly. On the moat, the LLM isn’t the differentiated product — the integrated stack and contracted backlog are. On the bubble, the test is whether OCF keeps compounding faster than the share count and the debt; at 31.5% it is, for now. On dilution at the top: issuing at a decade-high multiple is exactly when equity is cheap to sell. All three collapse into one question - is the AI demand durable? That, not the leverage, is where the risk lives: $102 billion of debt against $174 billion of TTM OCF is trivial coverage, and Q1 interest expense of $533 million was under 1% of operating income. What would actually change my mind:

Persistent OCF deceleration - single-digit OCF growth against a $102 billion debt stack, a drifting share count, and an accruing preferred dividend compounds the wrong way per share.

Expansion financing revealed as deficit financing - if Cloud backlog conversion slips, Cloud margins reverse below 20%, or 2027’s “significantly higher” CapEx arrives without commensurate revenue, then what I have characterized as funding contracted demand was funding hope, and the raise was dilution at the top.

A material useful-life adjustment - per the December article on AI-chip useful lives, shortening server lives from 6 back toward 4 years would compress FCF even as OCF holds. Not a thesis killer alone, but it tightens the loop.

Final Thoughts

Two years ago, the question on Alphabet was whether AI would break the cash-generation engine. It is not breaking - OCF is compounding faster than revenue. The question has moved to the capital structure: whether it can keep up with the deployment opportunity without a structural shift toward worse per-share economics. The evidence so far supports the deployment, and it is hard to fault the order of operations: debt while credit was cheap and long, equity while the stock was dear; both capital markets reached before the private AI complex needs them.

Face value is the principal repayable at maturity, before discount, issuance costs, or FX adjustments.

Carrying value is the debt's balance-sheet value: face principal minus unamortized discount and issuance costs (FX-adjusted for foreign-currency notes).

Vintages are the issuance years of the notes; each batch locks in the rates prevailing when it was sold.

A note is a bond - a debt security under which Alphabet borrows a fixed sum from investors and repays it at a set maturity, paying interest along the way. Debt issuance is the act of selling a new batch of such notes to raise cash.

Variable Interest Entity (VIE): a separate company Alphabet doesn't fully own but is tied to financially (here, funding commitments and leases for data-center and energy projects), which accounting rules may require it to disclose or consolidate even without majority ownership.

Financial guarantee: a promise to cover a third party’s debt or lease payment if that party defaults, a contingent liability that costs nothing unless the default happens.

Credit-derivative backstop: a contract under which Alphabet absorbs the credit risk on a third party’s obligation (e.g. a data-center operator’s financing), effectively insuring the lender; the $28.4 billion is the notional exposure, not an expected loss.

An at-the-market (ATM) program lets a company drip-feed newly issued shares directly into the open market over time, at prevailing prices and through a broker, rather than selling a single discounted block in an underwritten deal - flexible and low-cost, but with proceeds and dilution that accrue gradually rather than landing on one date.

Return On Invested Capital (ROIC) measures how much after-tax operating profit a business generates per dollar of capital invested in the business. The standard formula is ROIC = NOPAT / Invested Capital, where NOPAT (net operating profit after tax) is operating income multiplied by (1 minus the effective tax rate) and Invested Capital is total equity (book value) plus interest-bearing debt minus cash and cash equivalents. ROIC consistently above the company’s cost of capital (typically 8-10% for a mature business) is the signature of a business that should reinvest aggressively. ROIC trending down toward or below the cost of capital is the signature of a business that is destroying value through reinvestment, regardless of how fast revenue is growing.