MercadoLibre (MELI) Q4 2025 Results: Paying for Growth on Purpose

44.6% growth, 5-6 points of margin traded for scale, speed, and fintech penetration

“We prioritize investments that are most synergistic with our ecosystem and either deepen existing moats or create new ones. All of our investments are required to demonstrate a clear path to positive direct contribution under conservative assumptions”

— MercadoLibre Q4 2025 Shareholder Letter

MercadoLibre, Inc. (MELI 0.00%↑) posted another blockbuster quarter - Q4 2025 revenue up 44.6% to $8.8 billion and FY 2025 up 39%, but the stock fell 8% as margins compressed. Management explicitly chose to “buy” growth by reinvesting 5-6 points of operating margin into free shipping, logistics, credit cards, cross-border, and 1P, and the operating KPIs (frequency, logistics efficiency, Mercado Pago engagement, and disciplined credit metrics) suggest those investments are working. I bought the dip with MELI now 13% of my portfolio because I see temporary margin pressure as moat-widening, not a weakening business.

MercadoLibre: The Commerce + Fintech Flywheels

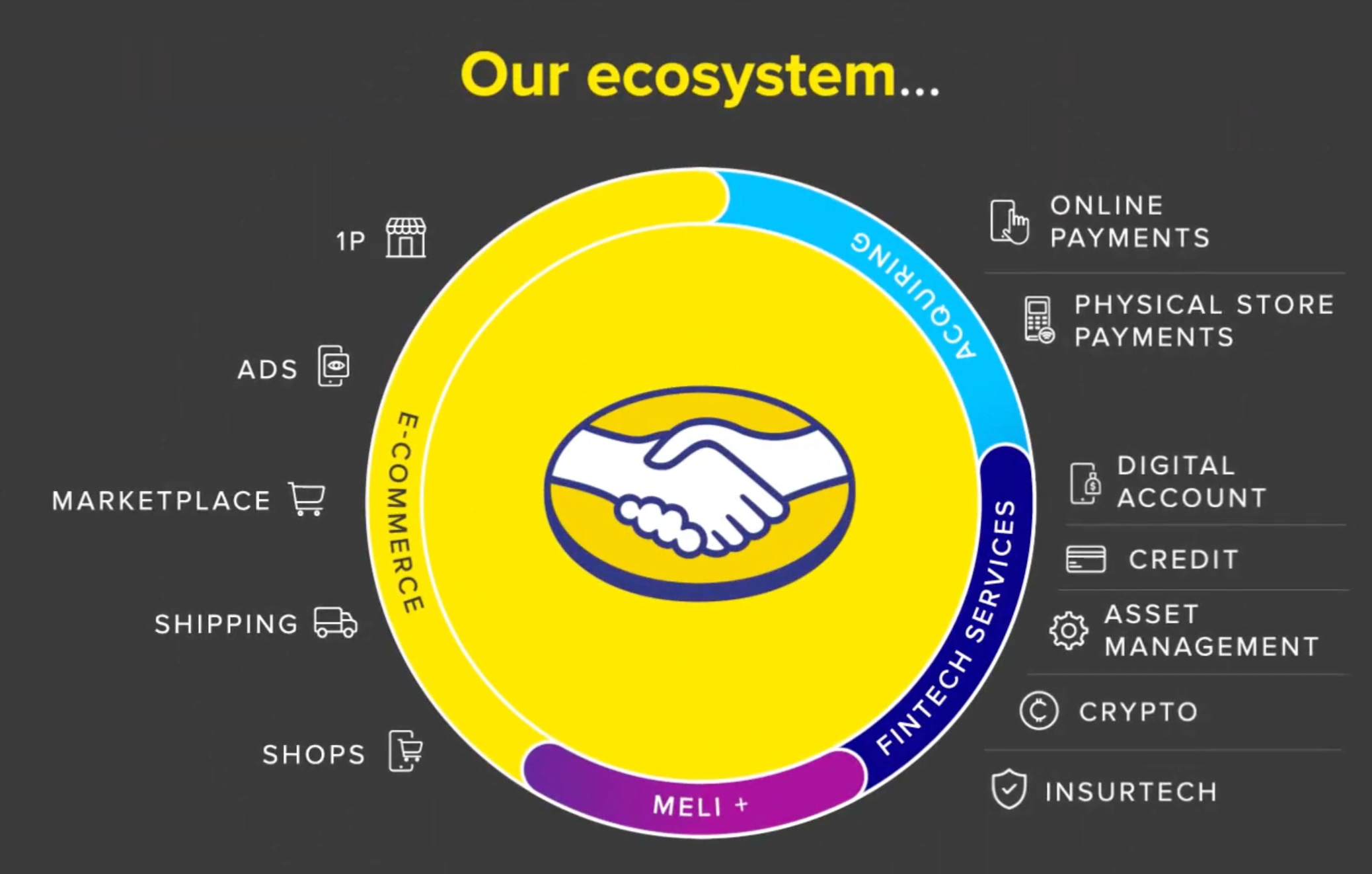

MercadoLibre is the leading e-commerce and fintech ecosystem in Latin America. Commerce compounds via selection → demand → seller supply → logistics density → faster delivery → higher conversion and repeat, with ads monetizing that engagement; Mercado Envios is “integral and crucial” to reducing friction and enabling fast delivery at competitive cost. Fintech (Mercado Pago) started at checkout and expanded into acquiring, accounts, savings/investments, and credit; the edge is data + distribution, using “repeated interactions with our ecosystem” to underwrite and offer credit contextually. Together, commerce drives fintech adoption, fintech boosts commerce frequency, and the data loop strengthens underwriting, reinforcing the moat.

The runway remains large; management notes “penetration is roughly half the level seen in the US, UK and China, and we see no structural reason why the region should not reach similar levels”.

Q4 2025 and Year-End 2025: 5 Key Results That Matter

The Q4 2025 results had plenty of moving parts, but five data points captured my attention.

1. Elite Growth at Scale: Quarterly Acceleration on Top of a Strong Year

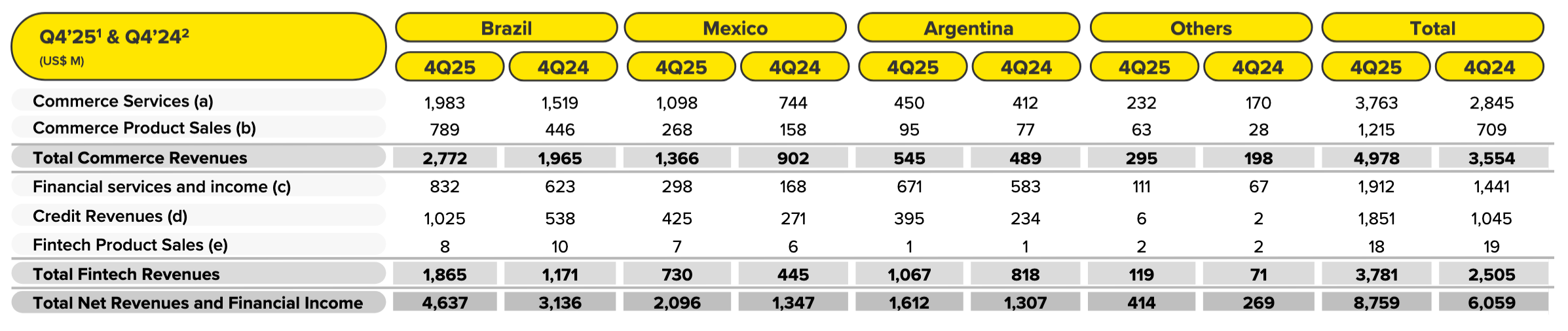

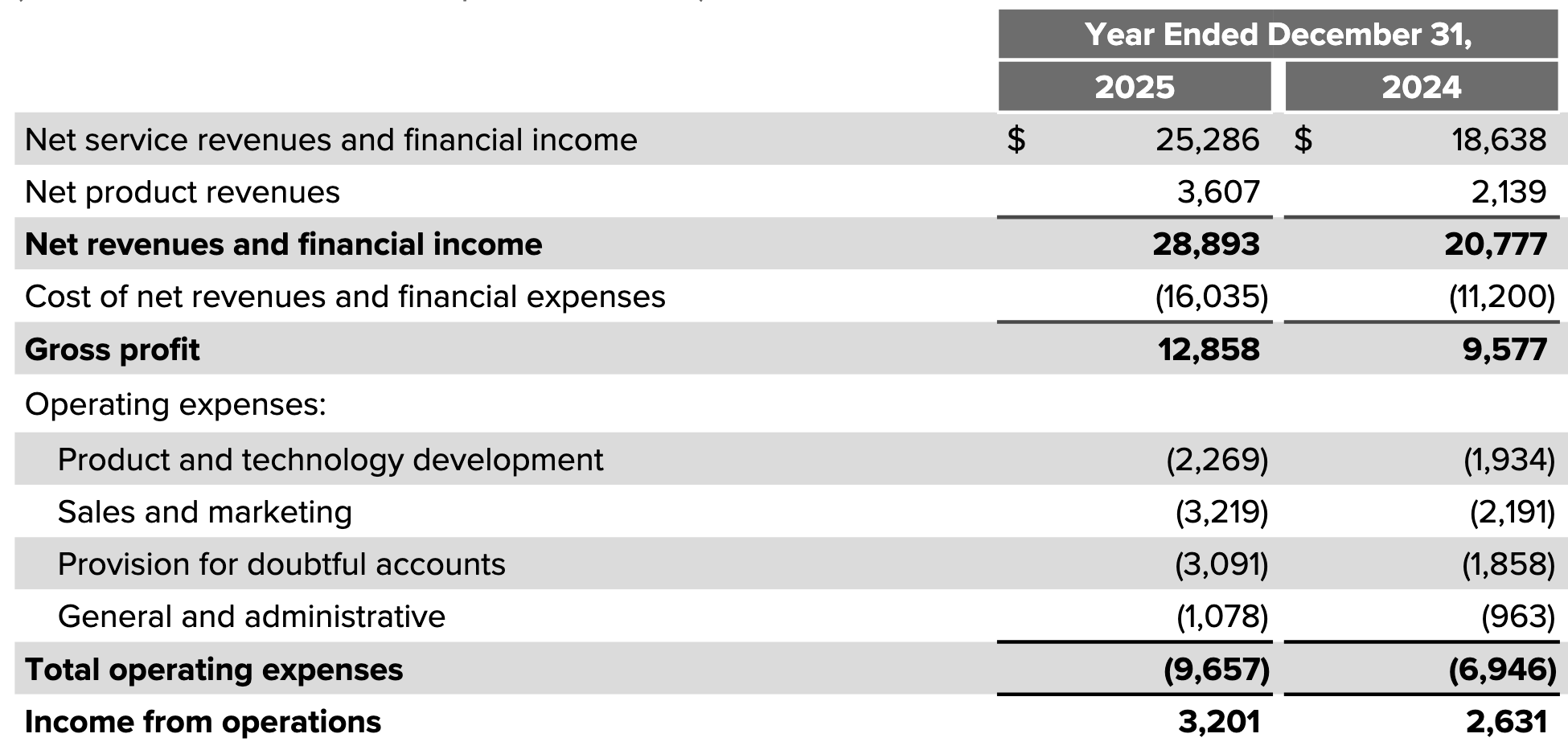

Q4 net revenues and financial income were $8.8 billion (+44.6% YoY), capping FY 2025 growth of 39% YoY with operating income growing 21.7% YoY, despite stepped-up investment intensity.

On the earnings call, management framed the quarter as “robust operating trends that reinforce the strength of the MercadoLibre ecosystem”, supported by “two primary growth drivers: the acceleration of our commerce business and the rapid adoption and structural expansion of our fintech services”.

The company has now grown the top line above 30% YoY for 28 consecutive quarters, underscoring the “effectiveness of the long-term investment and customer focus that we have within our ecosystem”.

2. Commerce: Frequency and Retention Are Improving, the Clearest Signal of Durability

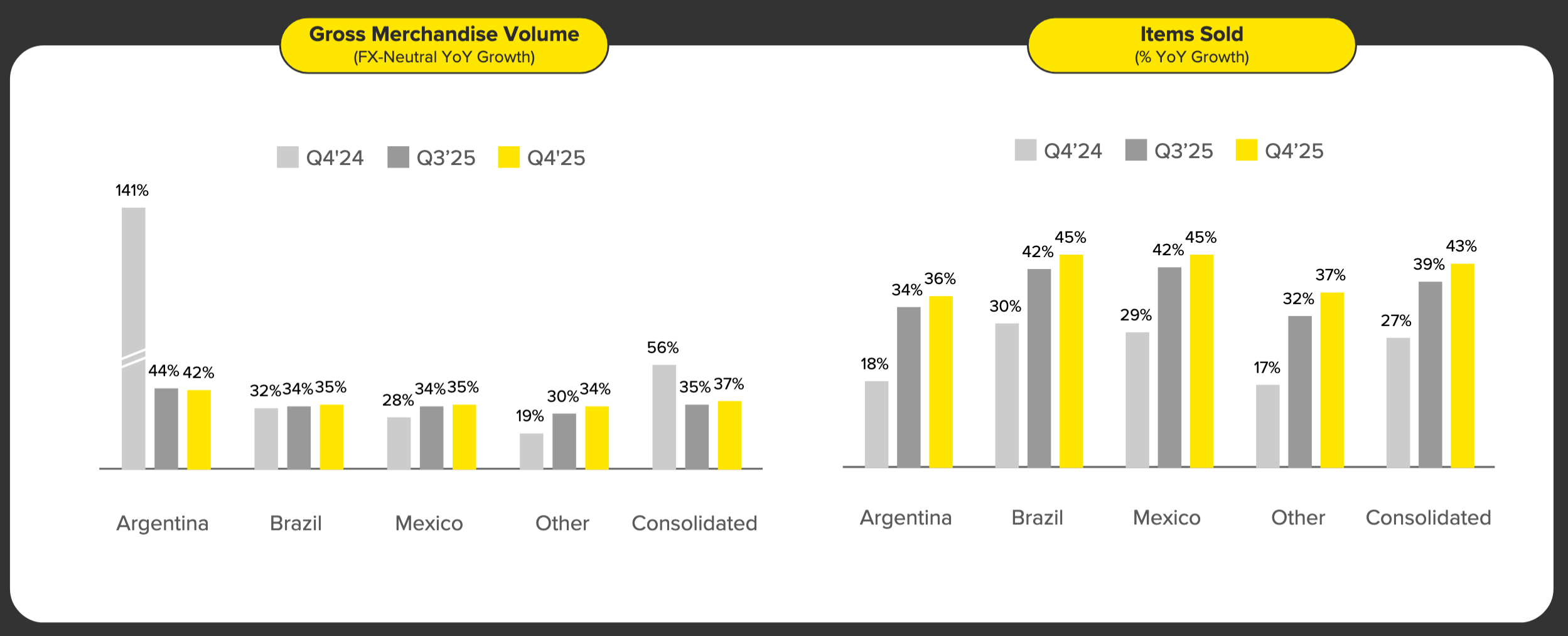

The headline is easy to summarize: more buyers, buying more often, across more categories. In Q4, Gross Merchandise Volume (GMV)1 was $19.9 billion (+36.8% YoY), unique active buyers reached 83.2 million (+23.6% YoY). Items sold accelerated from 39% YoY growth in Q4 2024 to 43% YoY growth in Q4 2025.

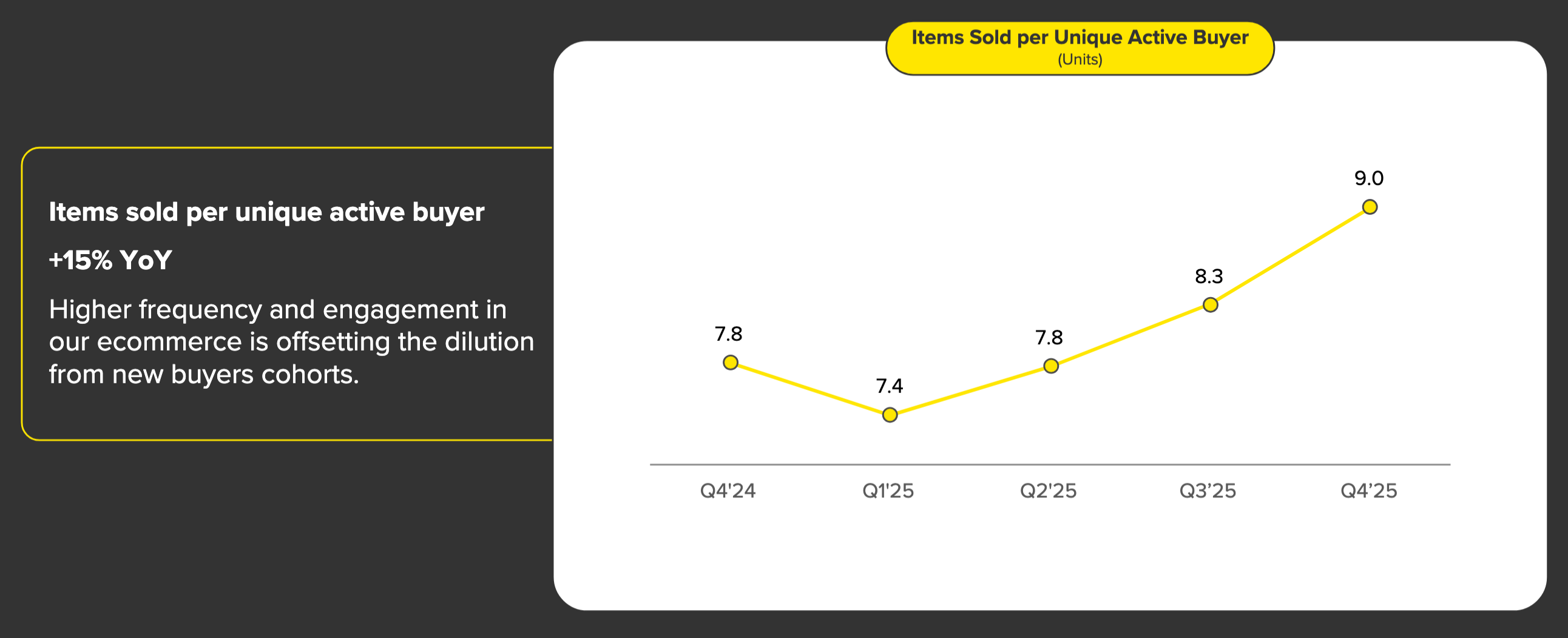

Items sold per unique active buyer rose to 9 items (+15.4% YoY). This matters because frequency is the hidden engine of e-commerce compounding: higher frequency improves retention economics, creates more ad inventory, and increases logistics density (which then improves unit costs and delivery speed).

Management directly connects this behavioral change to their value proposition investments in Brazil. In the shareholder letter, they wrote: “Free shipping has been one of the most important pillars of our value proposition for a decade […] Extending free shipping in Brazil to items starting from R$19 reflects this conviction […] The impact on behavior is clear”. They added: “Since June, new buyers in Brazil have purchased more items across a larger number of categories with higher retention than cohorts that joined prior to the lower free shipping threshold”. In plain terms: MELI is buying habit formation today to harvest operating leverage tomorrow.

Advertising is the high-margin layer on top of this Commerce growth. Mercado Ads’ revenue grew 70% YoY in the quarter, and management noted penetration is still small versus its potential. As frequency rises, ads should contribute more to Commerce revenue and help offset shipping-related margin pressure over time.

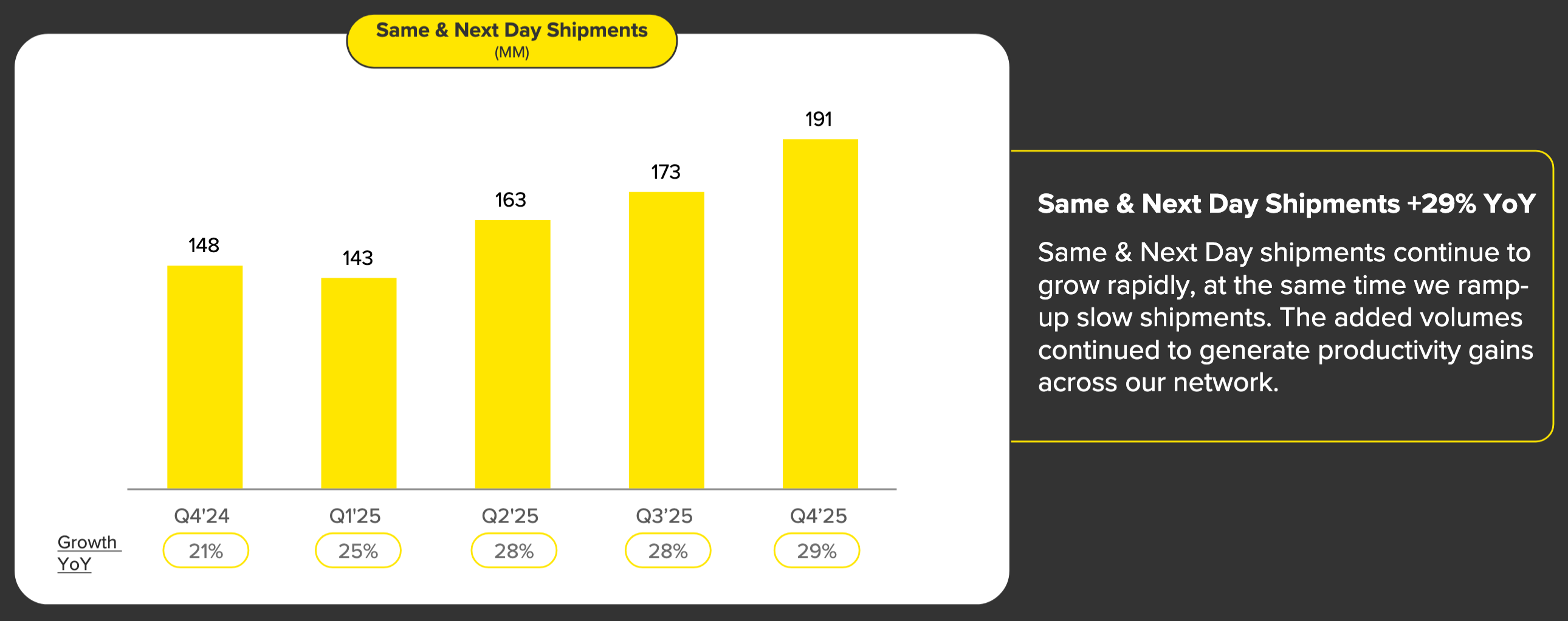

3. Logistics Scaled and Unit Economics Improved

“Operating an efficient logistics network is another critical pillar of our value proposition and a major competitive advantage. A large majority of orders across the region […] qualify for free & fast delivery, with nearly 75% of fast shipments delivered within 48 hours.”

In Q4, same/next-day shipments reached 191 million (+29% YoY).

For the full year the “network absorbed a 41% YoY increase in volume during the year (nearly 500 million) additional shipments”. Management highlighted what I consider one of the most important proof points in the entire shareholder letter: “Unit shipping costs in local currency fell 11% YoY in Brazil in Q4’25”, while “maintaining the high service levels that have built trust over time”.

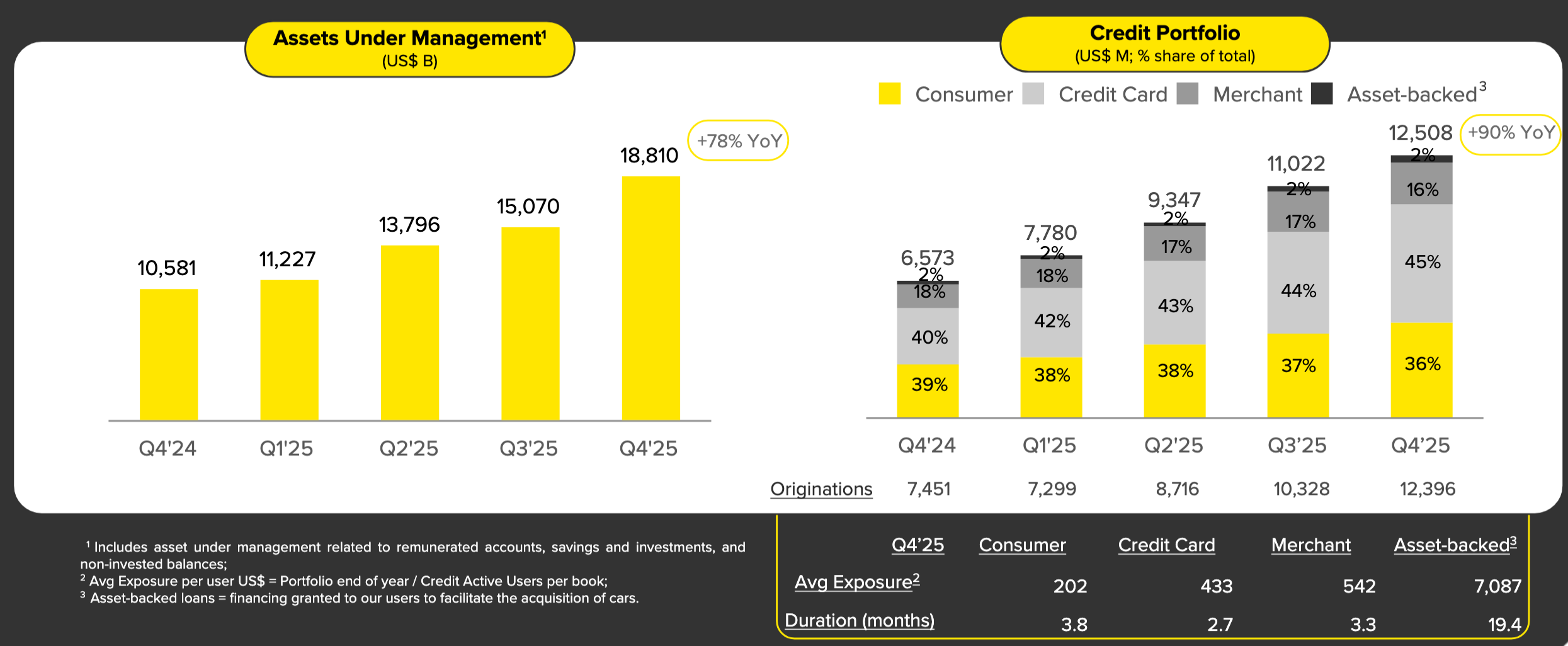

4. Fintech: Moving From Payments To a Full Financial Institution

Management is explicit about their ambition:

“We operate in a region where many millions of people are poorly served by the traditional financial system, or not served at all […] Our ambition is to build Latin America’s largest digital financial institution”.

In Q4, fintech monthly active users (MAU) were 77.9 million (+27.3% YoY) - management highlighted that “MAU have been growing close to 30% for ten consecutive quarters, as our value proposition continues to improve”. Assets under management (AUM) reached $18.8 billion (+78% YoY, and a record +24.8% QoQ), and the credit portfolio ended at $12.5 billion (+90% YoY, 4x in three years).

MELI uses the marketplace checkout as a distribution engine for credit, and the real advantage is the underwriting loop behind it. Management says maintaining strong asset quality is a key enabler of growth, achieved by “combining technology with our marketplace’s high-quality audience of buyers”, where “data from repeated interactions with our ecosystem feeds into our underwriting models”. As a result, MELI has “millions of pre-approved users who are offered credit at the marketplace checkout (and elsewhere)” which was particularly effective in Q4 2025 as the company “issued almost 3 million credit cards by leveraging our marketplace’s peak season”. On the merchant side, the flywheel is similar: 33.8% of marketplace sellers are taking Mercado Crédito to fund inventory and growth, reinforcing selection, availability, and GMV back on the commerce platform.

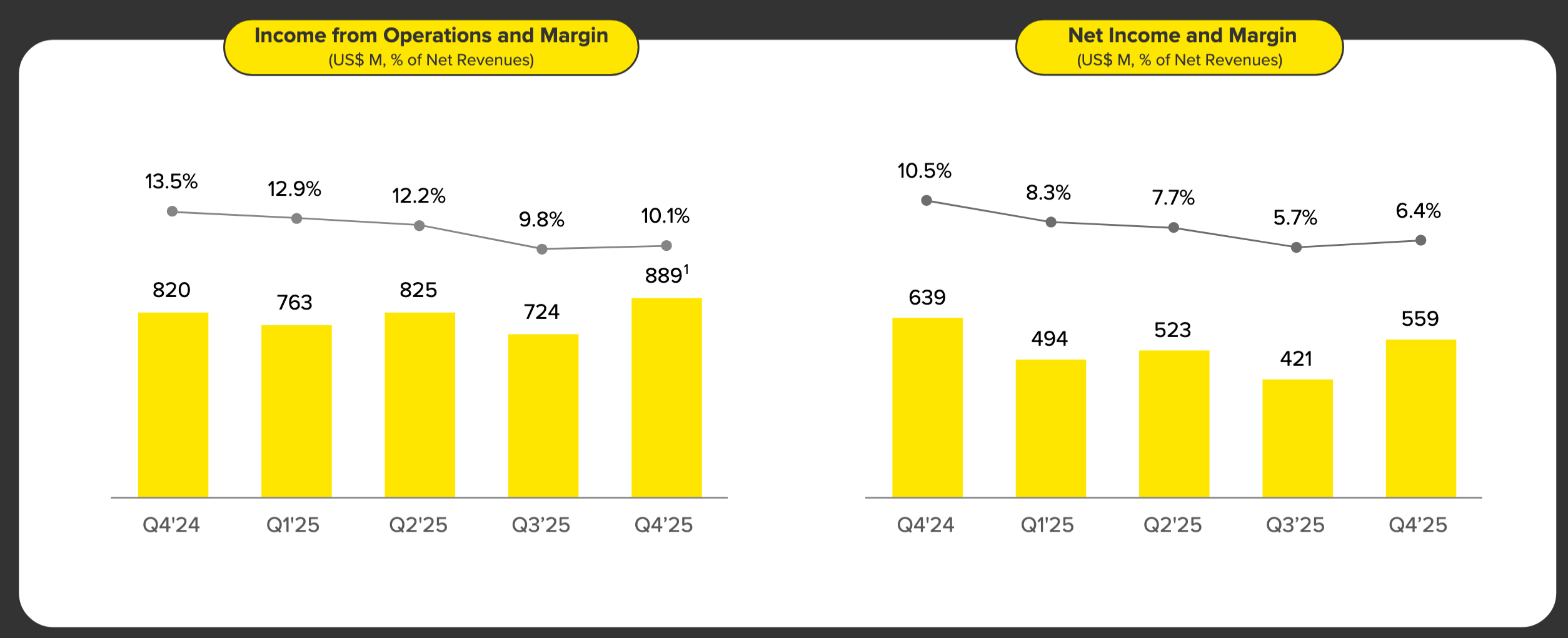

5. Margins Compressed by Design, and Management Quantified the “Moat Spend”

The market’s issue with the quarter was straightforward: profitability didn’t keep up with revenue growth. Q4 operating income was $889 million (10.1% margin, -25.2% YoY) and net income was $559 million (6.4% margin, -39% YoY).

MELI quantified the operating margin compression and explained it as deliberate, early-stage investment. In the shareholder letter: “We estimate the combined impact of our strategic investments […] was equivalent to 5-6 percentage points of operating margin in Q4’25”. They list the major initiatives: “lower free shipping threshold in Brazil, CBT, 1P and the credit card”. Management made the philosophy unambiguous:

“[…] we do not solve for short-term margin optimization. Our investment plan for 2026 will be consistent with this bold and disciplined approach to investing behind long-term growth.”

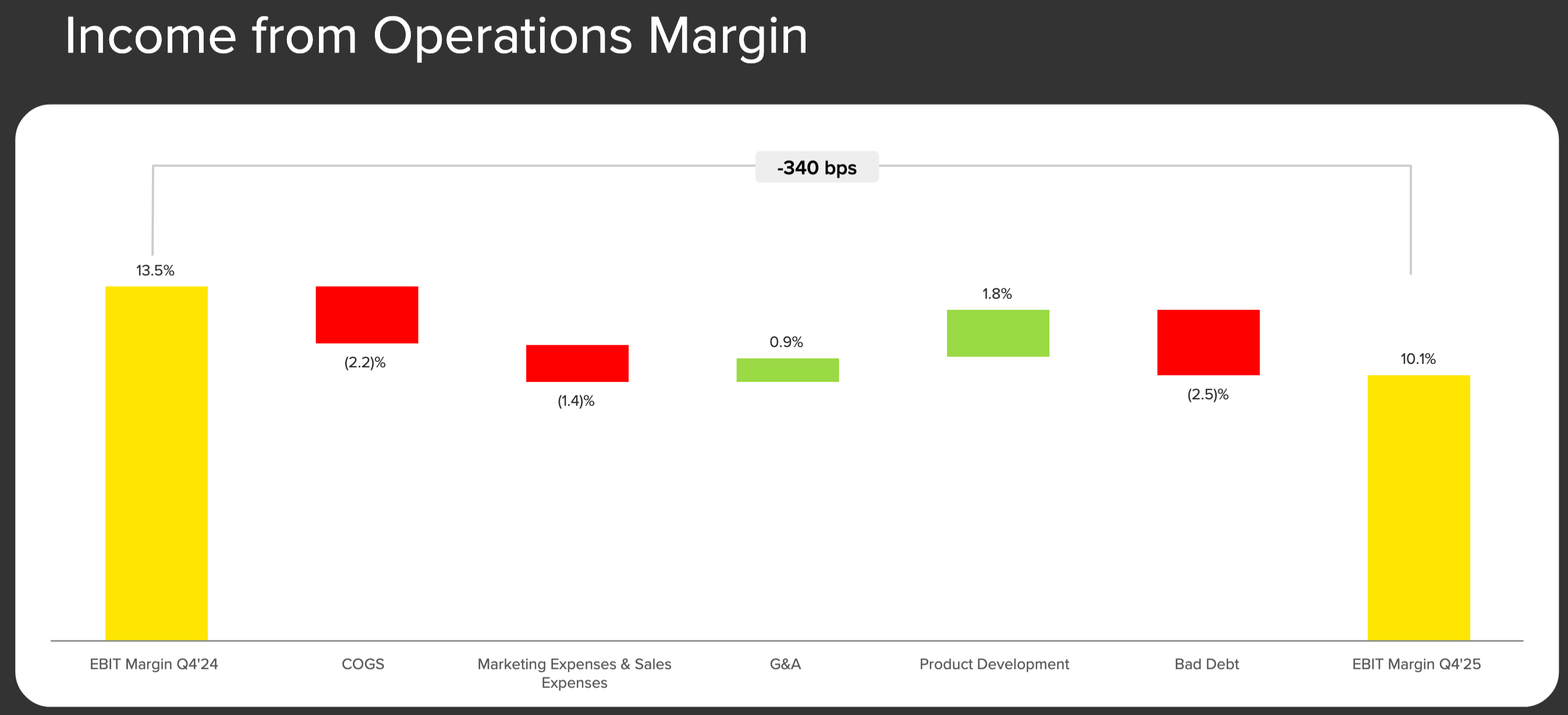

One line item worth calling out is “Bad Debt”, which is MercadoLibre’s provision for doubtful accounts (expected credit losses recognized through the P&L as the credit portfolio expands). Management addresses this directly in the shareholder letter:

“Although Q4 typically benefits from positive seasonality in provisions for doubtful accounts, this line was broadly flat QoQ, partly due to acceleration of growth in our Consumer books in Brazil and Mexico.”

In plain English, MELI grew credit aggressively, and that growth requires building loss reserves up front, so even if underlying credit performance is healthy, provisions can still weigh on operating margin in the near term.

Year-End “Platform Proof”: Two Engines, Broader Footprint, Strong Cash Generation Despite Reinvestment

Stepping back from the quarter, the full-year numbers validate that MELI is scaling both flywheels. FY 2025 net revenues and financial income were $28.9 billion (+39.1% YoY). Commerce generated $16.3 billion and fintech $12.6 billion. Operating expenses rose 39% YoY to $9.66 billion, driven mainly by sales and marketing (+46.9%) and provision for doubtful accounts (+66.4%), as MELI is leaning into growth levers without letting the core cost base (product and technology +17.3% and G&A +11.9%) balloon.

This cost structure also helps explain the margin narrative: gross margin (COGS) and operating margin (OpEx) pressure in 2025 was largely the deliberate cost of scaling long-term initiatives: expanded free shipping in Brazil, ramping 1P and fulfillment capacity, and early-stage investments in cross-border trade and credit. Those moves increased logistics subsidies and lowered shipping-related monetization (contributing to modest take-rate pressure), while 1P, CBT international fulfillment, and newer credit cohorts remain margin-dilutive during their build-out phase. Management framed the investment as a conscious trade-off to deepen engagement and widen the ecosystem moat as these initiatives scale toward maturity.

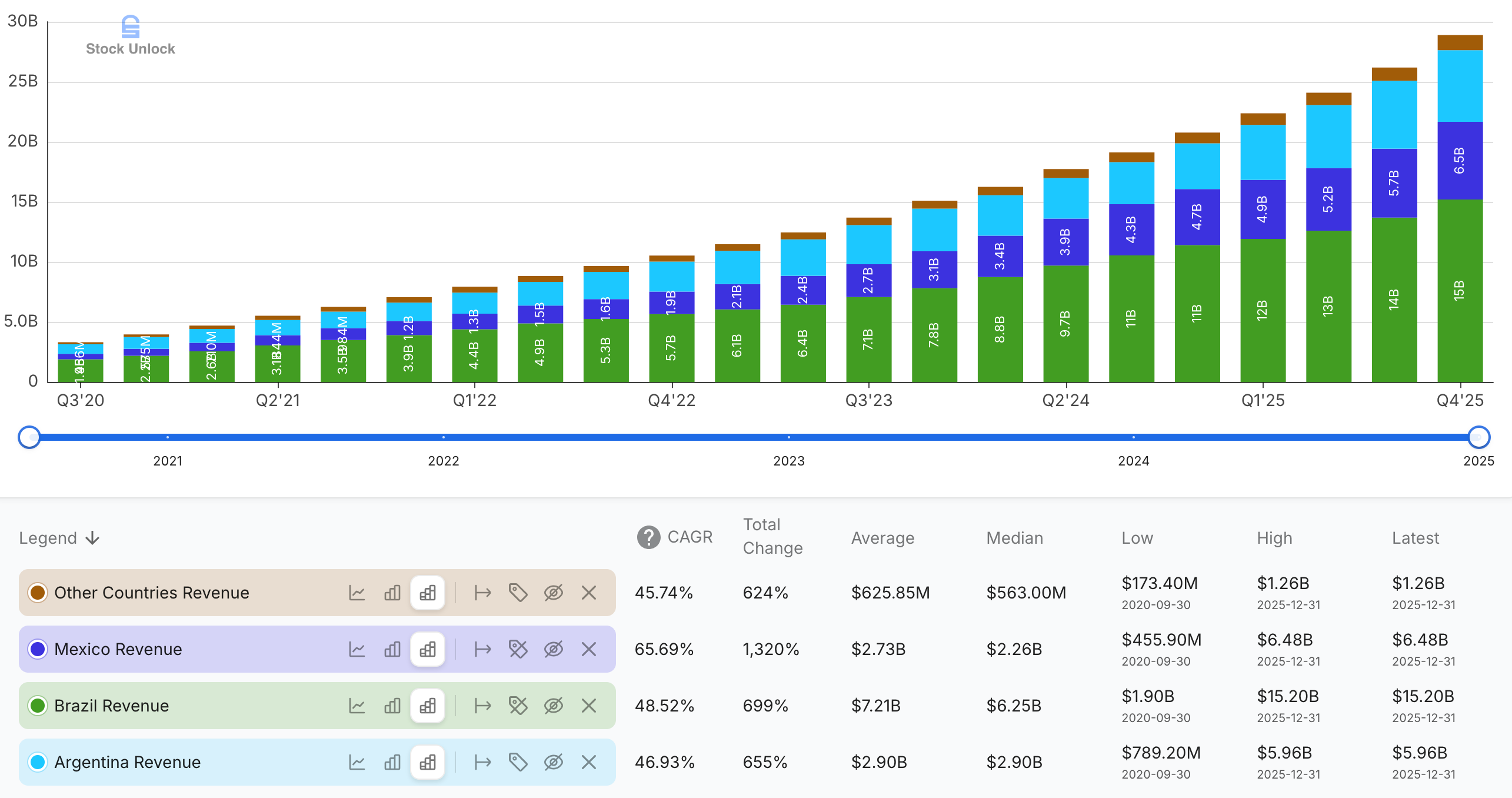

The ecosystem KPIs kept compounding: FY 2025 GMV was $65 billion (+26.4% YoY), Total Payment Volume (TPV) was $277.8 billion (+41.3% YoY), and Acquiring TPV was $188.1 billion (+32.3% YoY).

One of the cleanest ways to see MELI’s “platform proof” is to zoom out. Since 2012, Commerce and Fintech revenues have both compounded aggressively: Fintech even faster, while operating income has scaled alongside them. That long-term trajectory also highlights a structural shift in the mix: Fintech is no longer an add-on to Commerce, and it is approaching parity in revenue contribution, which meaningfully changes MELI’s earnings power profile. Commerce drives engagement and purchase frequency; fintech drives monetization depth and balance-sheet products.

Crucially, MELI did not fund this expansion by burning the balance sheet. Despite heavy reinvestment, the company generated approximately $1.48 billion in adjusted free cash flow2 in FY 2025. The ecosystem is internally generating capital while still scaling aggressively.

Equally important is the geographic breadth of that growth. Brazil remains the largest engine while Mexico and Argentina are no longer “supporting markets” - they are material contributors with accelerating adoption across commerce and fintech. The ecosystem is diversifying its revenue and profit pools across multiple countries, reducing reliance on any single macro backdrop while reinforcing network density in each local market.

Valuation: Is MercadoLibre Undervalued?

When a company is rapidly expanding a credit portfolio, conventional free cash flow gets distorted by balance-sheet swings, especially cash deployed into new loans. That’s why MELI reports adjusted free cash flow (AFCF) and why I start there. In FY 2025, operating cash flow (OCF) was $12.12 billion. After backing out movements tied to customer funds and regulatory restrictions ($4.99 billion), subtracting CapEx ($1.33 billion), and adjusting for the net cash deployed into the loan book ($6.66 billion) and the net proceeds from loans payable/other fintech liabilities ($2.35 billion), MELI reported AFCF of $1.48 billion.

To approximate normalized cash earnings power, I adjust AFCF for reinvestment into loan growth and estimated growth CapEx: $6.32 billion = $1.48 billion (AFCF) + $0.53 billion (40% of CapEx) + $6.66 billion (loan book growth) - $2.35 billion (net loan funding). This is not a forecast - if MELI slowed these investments, growth would likely slow too. It’s a useful way to frame underlying earning power during an investment-heavy phase.

On today’s ~$86.5 billion market cap, that implies ~13.7x price-to-normalized earnings power: modest for a business compounding revenue above 30% for 28 consecutive quarters while investing heavily into logistics density, fintech adoption, and credit penetration.

Final Thoughts

MELI exited 2025 with rare fundamentals: 28 straight quarters above 30% growth while investing aggressively in logistics, payments, and credit. The stock sold off on margin compression, but management was explicit that this was a deliberate choice tied to specific initiatives. I’m staying focused on the operating scorecard - frequency, logistics efficiency, fintech engagement, and credit quality - because that’s what will drive long-term earnings power.

Gross Merchandise Volume (GMV) is the total value of goods sold through MercadoLibre’s commerce platform over a given period, before returns, discounts, and fees (e.g. a measure of marketplace sales activity, not MELI’s revenue).

Adjusted Free Cash Flow (AFCF) is MercadoLibre’s measure of underlying cash generated by the business. It starts with cash from operating activities (OCF) and strips out the distortion caused by loan book growth so investors can see a cleaner view of cash generation.

Thanks for this informative article. Perhaps I overlooked something, but can you please explain more about why you added $6.6 billion into the loan book growth for AFCF? Do you account for bad loans and even potential catastrophic loss in that area (i.e. changing government regulations on loan interest rates etc.)? Would you still apply a similar multiple to the loan book? Thanks.