MercadoLibre (MELI) Q1 2026 Results: The Right Response Is Not to Harvest, It Is to Invest

Brazil items doubled in nine months, unit shipping costs accelerated lower, and the cross-sell flywheel widened from 26% to 36% of merchants. Margin compression is moat-building in real time

“When your business is behaving like this, we believe the right response is not to harvest — it is to invest.”

— MercadoLibre Q1 2026 Letter to Shareholders

MercadoLibre, Inc. (MELI 0.00%↑) posted Q1 2026 results on May 7, 2026, and the stock fell 12.7% the following day, extending a 12-month drawdown of 32% that has taken MELI stock back to its lowest price since June 2024.

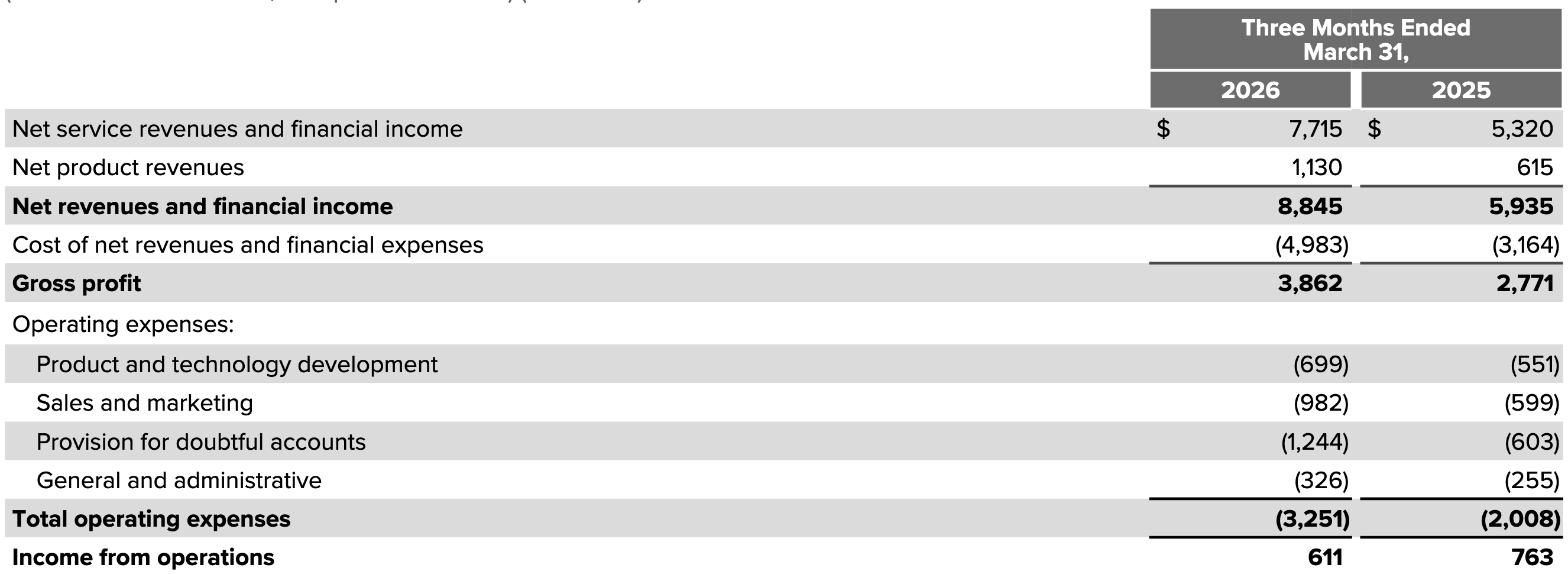

The headline numbers are striking in two opposite directions: consolidated revenue grew 49% year-over-year (YoY) to $8.8 billion, the fastest pace since Q2 2022, while operating income declined 19.9% YoY to $611 million at a 6.9% operating margin (-6% YoY). Twenty-six years after launch, this is one of MELI’s strongest top-line quarters ever, on a business approaching a $35 billion annualized revenue run-rate. It is also the quarter where management has been most explicit that they will continue to compress near-term margins to capture what they describe as a “once-in-a-generation opportunity” across Latin America (LatAm) commerce and fintech.

I covered the Q4 2025 quarter under the headline “Paying for Growth on Purpose”.

Q1 2026 is the same playbook with a hotter dial. I bought the dip in February and March after the Q4 2025 results disappointed the market, and the Q1 2026 results confirm my investment thesis. During the Q1 2026 earnings call, CFO Martin de Los Santos used the call to make the philosophy unmissable:

“We are not optimizing for short-term margin. We are making investments based on the results that we’re seeing and the results are very positive. When you look at revenue growing at +49%, which is the highest rate of growth over the past 4 years, that’s one example of our investments performing very, very well.”

The market did not like this framing. I do, because the operating KPIs - frequency, retention, unit shipping costs, credit card NPLs, advertising growth, fulfillment penetration - are saying the same thing the revenue line is saying: the investments are compounding. MELI remains a high-conviction holding.

MercadoLibre: The Commerce + Fintech Flywheels, Re-stated

MELI is the largest commerce and fintech ecosystem in LatAm: #1 e-commerce platform in the region by GMV, #1 fintech by monthly active users in Argentina, Chile and Mexico, and #2 in Brazil. Two engines feed each other. Commerce engagement (selection → demand → seller supply → logistics density → faster delivery → higher conversion and repeat) feeds fintech adoption (checkout → acquiring → accounts → savings → credit), and the data loop from both sides feeds the underwriting models. What is new in Q1 2026 is how directly management is framing the credit card as the Mercado Pago equivalent of what fulfillment was for the marketplace ten years ago. From the Q1 2026 Letter to Shareholders:

“Investing in our credit card is as pivotal for Mercado Pago as the launch of our managed logistics network was for our marketplace ten years ago. Just as fulfillment was a critical element of achieving market leadership in Commerce, the credit card is central to our ambition of being the region’s largest digital bank. […] The credit card increases marketplace conversion, GMV per user, and transactions across the ecosystem. This is the cross-sell flywheel at work.”

The runway, in management’s own framing: the average American makes 41 online purchases per year; the average Latin American makes 7; MELI’s own buyers average 11. In Mexico, more than half the population still relies on informal credit and 85% uses cash for purchases under $30. In Argentina, more than 80% of adults have a bank account but credit-to-individuals as a percentage of GDP is one-fifth of Brazil’s level. The letter adds bluntly:

“In Latin America, the digital economy is not slowing down - it is just getting started.”

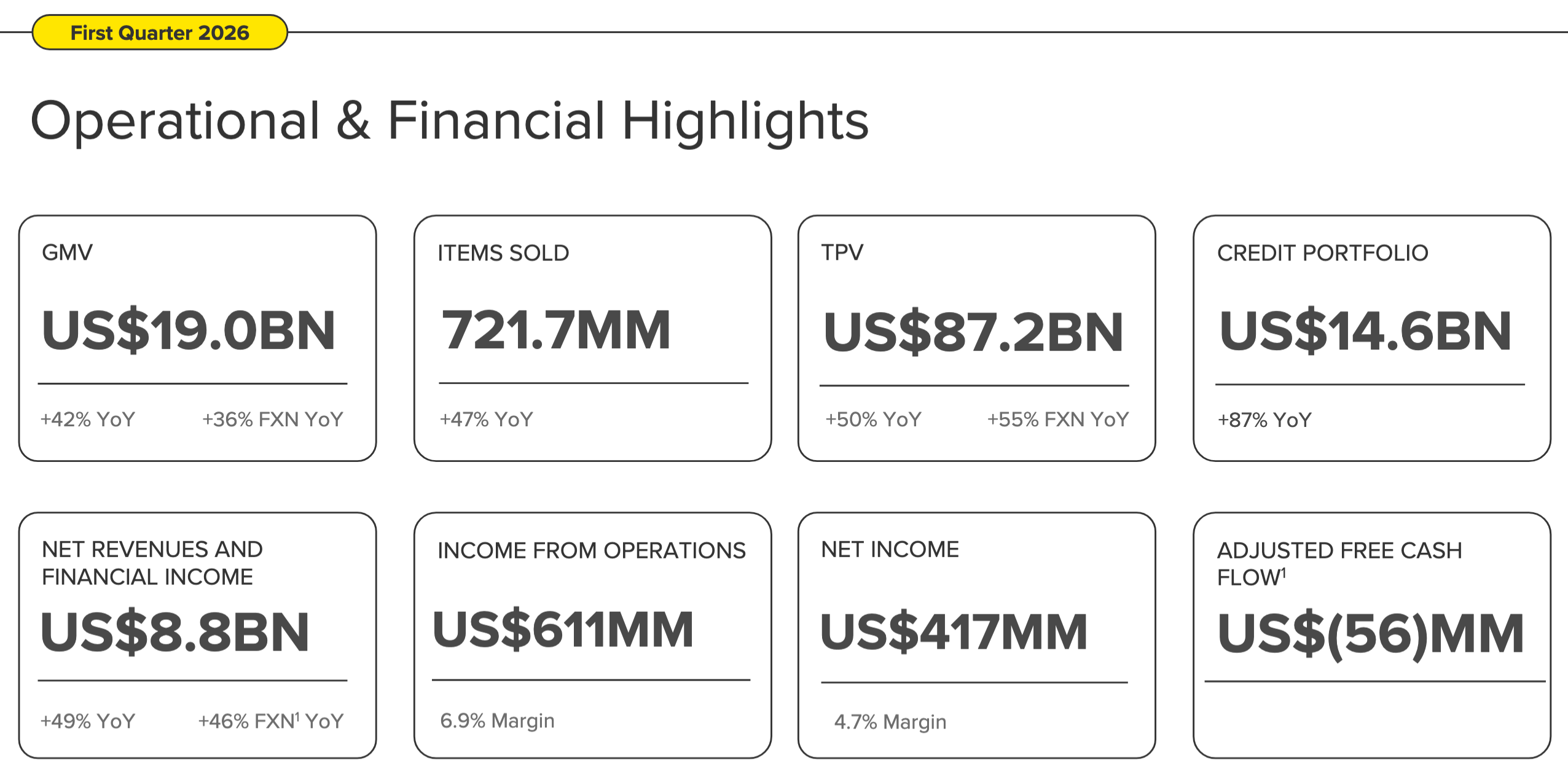

Q1 2026 Highlights

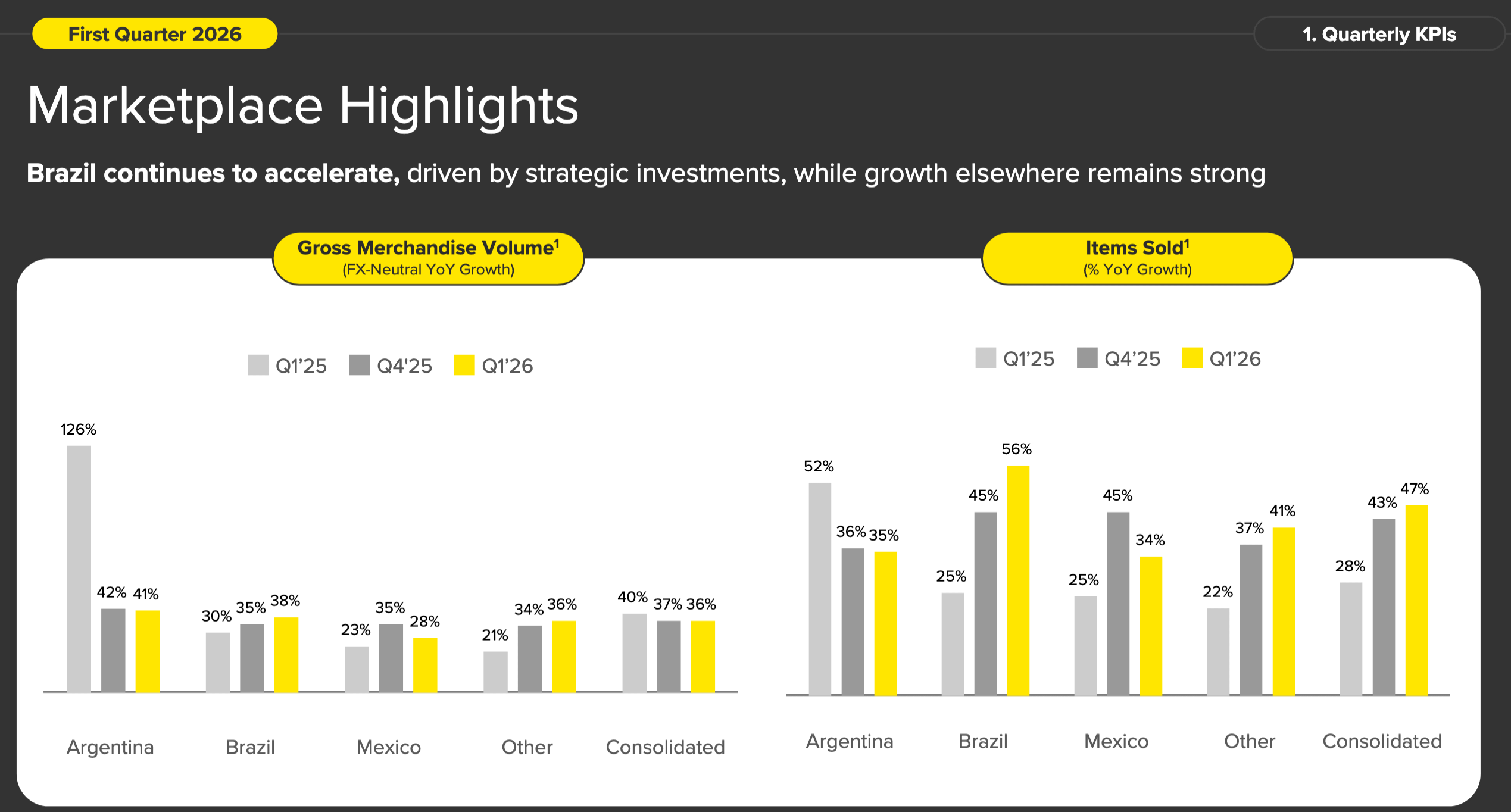

Revenue $8.8 billion (+49% YoY) - the fastest pace since Q2 2022 and the 29th consecutive quarter of >30% YoY growth. Brazil revenue +54.9%; Mexico +61.7%; Argentina +22.9%.

Brazil items sold +56% YoY, accelerating from +45% Q4 2025, +42% Q3 2025, and +26% Q2 2025 - volume growth has doubled in nine months. Unique buyer growth in Brazil reached +32% YoY, the fastest in five years, with a record +17 million YoY increase in unique buyers. Conversion1 in Brazil rose +1 percentage point YoY, large for a marketplace at MELI’s scale.

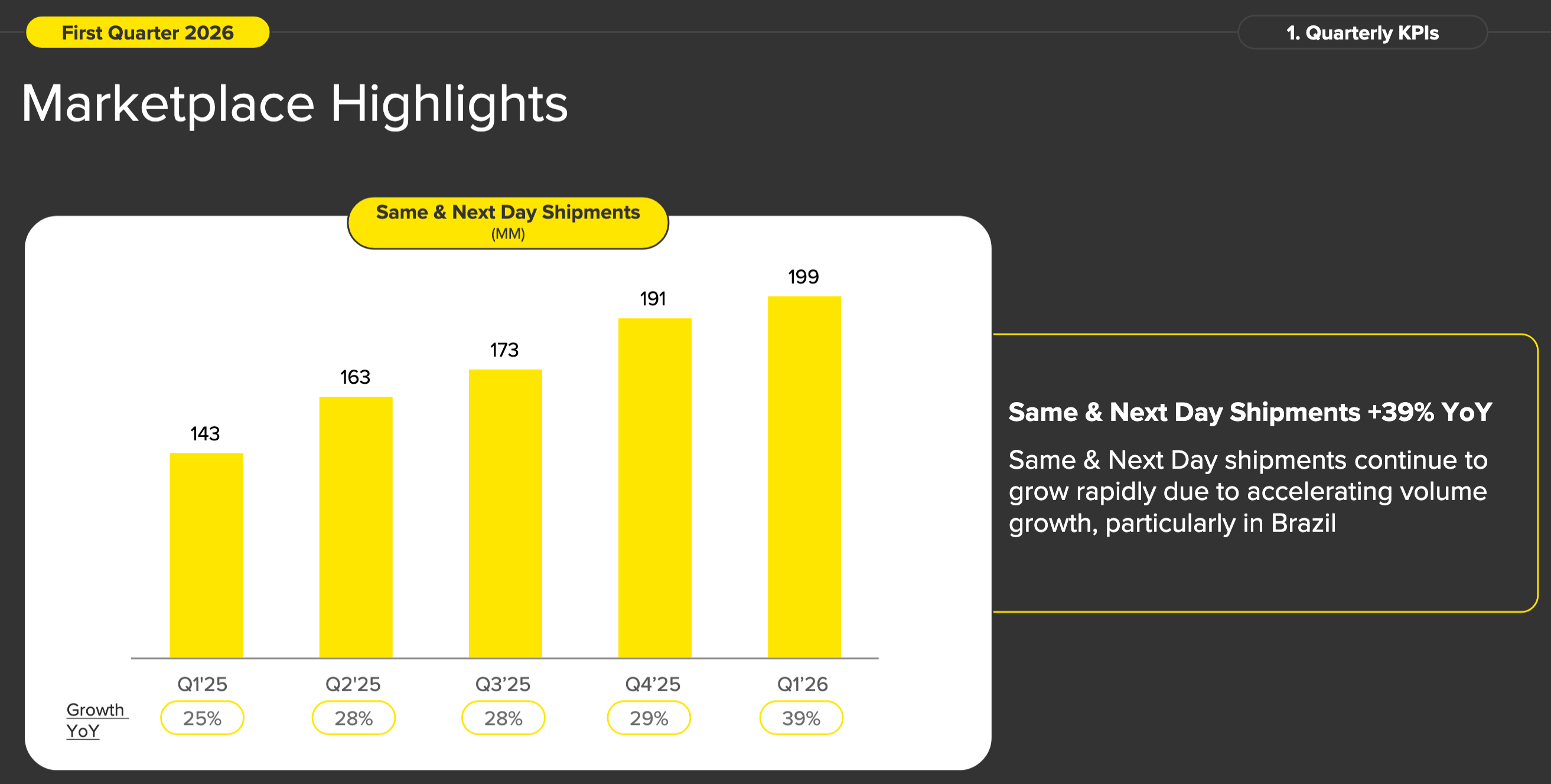

Brazil unit shipping costs fell 17% YoY in local currency - accelerating from -11% in Q4 2025 while absorbing 56% volume growth. Same/next-day shipments reached 199 million (+39% YoY). Some price points below the new R$79 (~$16) free-shipping threshold are already breakeven on a variable contribution basis.

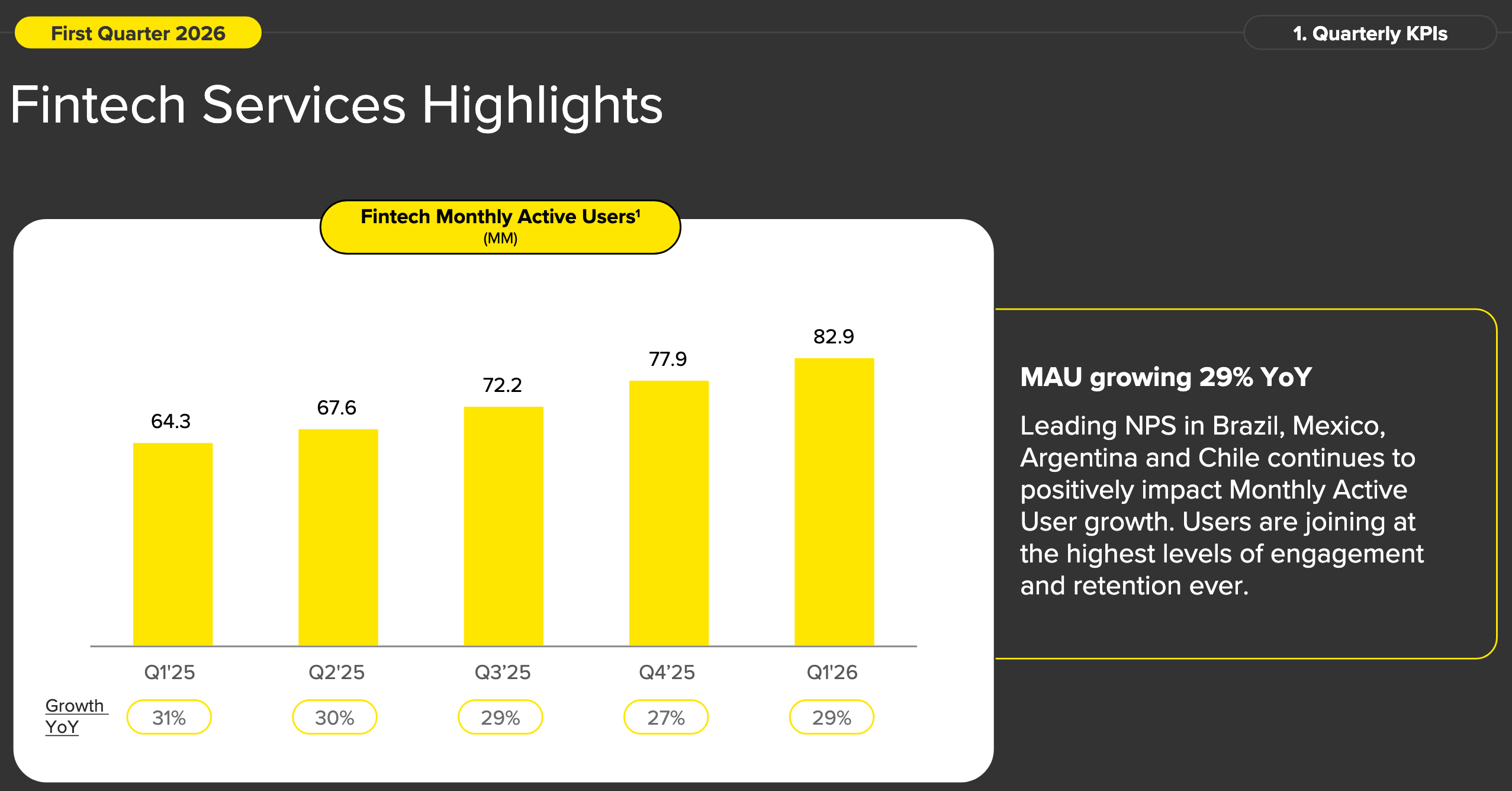

Fintech engine compounding at scale - Mercado Pago monthly active users (MAU) hit 82.9 million (+29% YoY); AUM $19.9 billion (+77% YoY); credit portfolio $14.6 billion gross (+87% YoY), the largest nominal quarterly increase ever. Credit cards issued in Q1: 2.7 million.

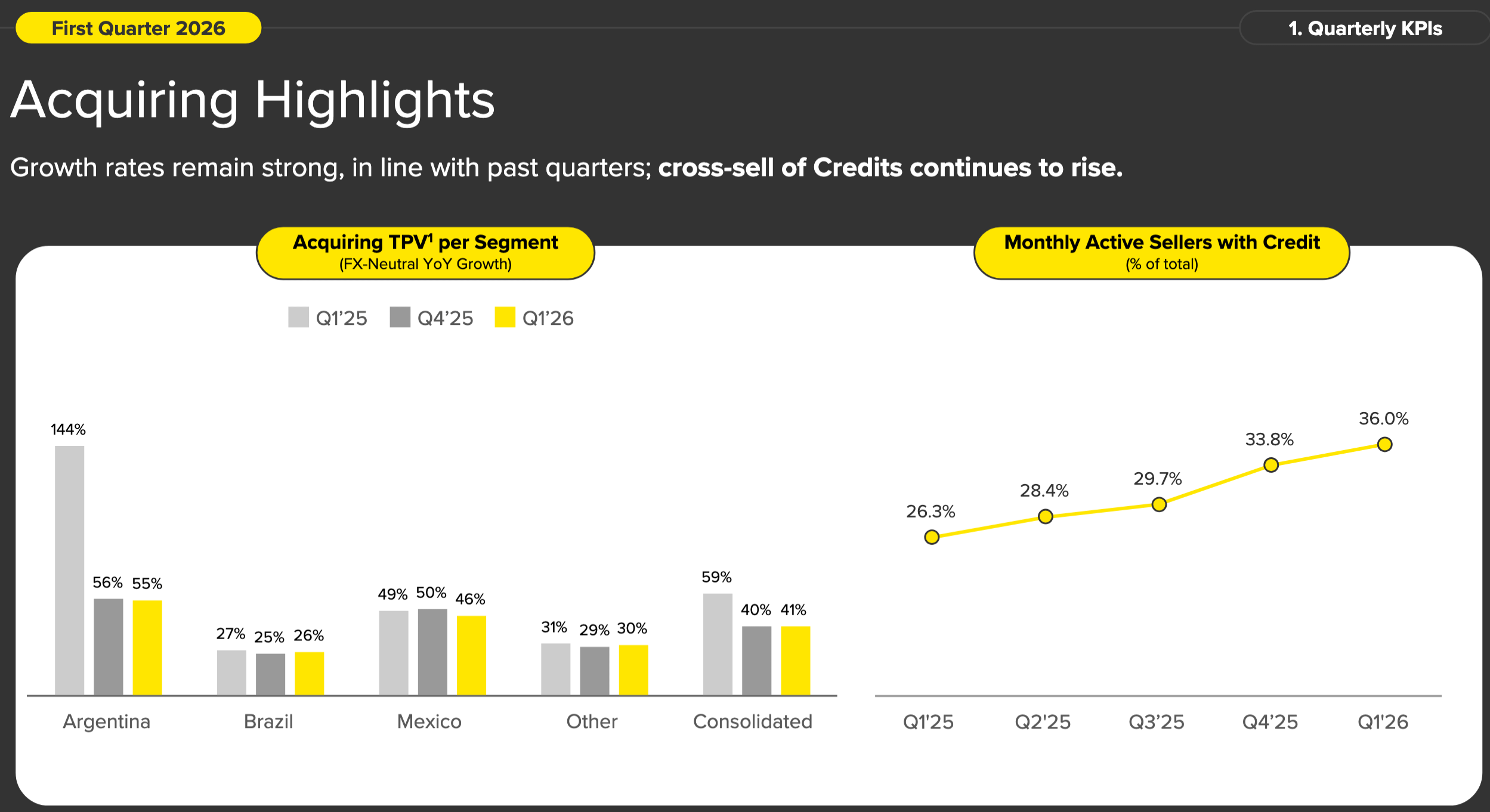

Cross-sell flywheel is widening - The share of monthly active sellers using Mercado Crédito grew from 26.3% in Q1 2025 to 36% in Q1 2026. The credit card is the most powerful instrument for converting marketplace-only users into active fintech users.

Mercado Ads grew +73% YoY, roughly 4x the regional digital ad market growth in 2025, and continuing in Q1 2026. LatAm’s digital ad market is still only ~50% of total ad spend, versus ~75% in the US.

AI starts showing up in the bridge: Product & technology expense fell from 9.3% of revenue to 7.9%, contributing +1.4% of operating leverage to the margin bridge - the first quarter where AI-driven productivity is materially visible. Engineer headcount is now planned to be broadly flat in 2026 thanks to AI productivity. Claude Cowork is rolled out to 31,000 employees, making the company one of the earliest large-scale enterprise adopters of AI agents globally.

Q1 2026 Lowlights

Operating margin compressed 6% YoY to 6.9%, the lowest since 2022 - Operating income declined 19.9% YoY to $611 million. Provisions for doubtful accounts drove 3.9% of the operating margin decline alone and management has been explicit that this dial will not change materially in the near term. Margins now depend on competitive intensity as much as on management’s choice to double down on investments the opportunity ahead of them.

The credit book’s risk profile is widening - Average duration2 of Brazil personal loans extended from 5 months to 8 months as MELI deliberately reaches customers it previously declined. Credit card mix in the total credit portfolio rose from 42% to 46%, mechanically lowering blended NIMAL3 because credit cards require full upfront provisioning before they generate income. NIMAL fell to 17.8% (vs 22.7% Q1 2025 and 23.3% Q4 2025) - partly seasonal, partly mix, partly the deliberate Brazil expansion. Reserve coverage and 15-90 day Non-Performing Loans (NPL) look stable to improving. The risk profile of the next dollar of new credit is not the same as the average dollar of existing credit. This is real and worth monitoring.

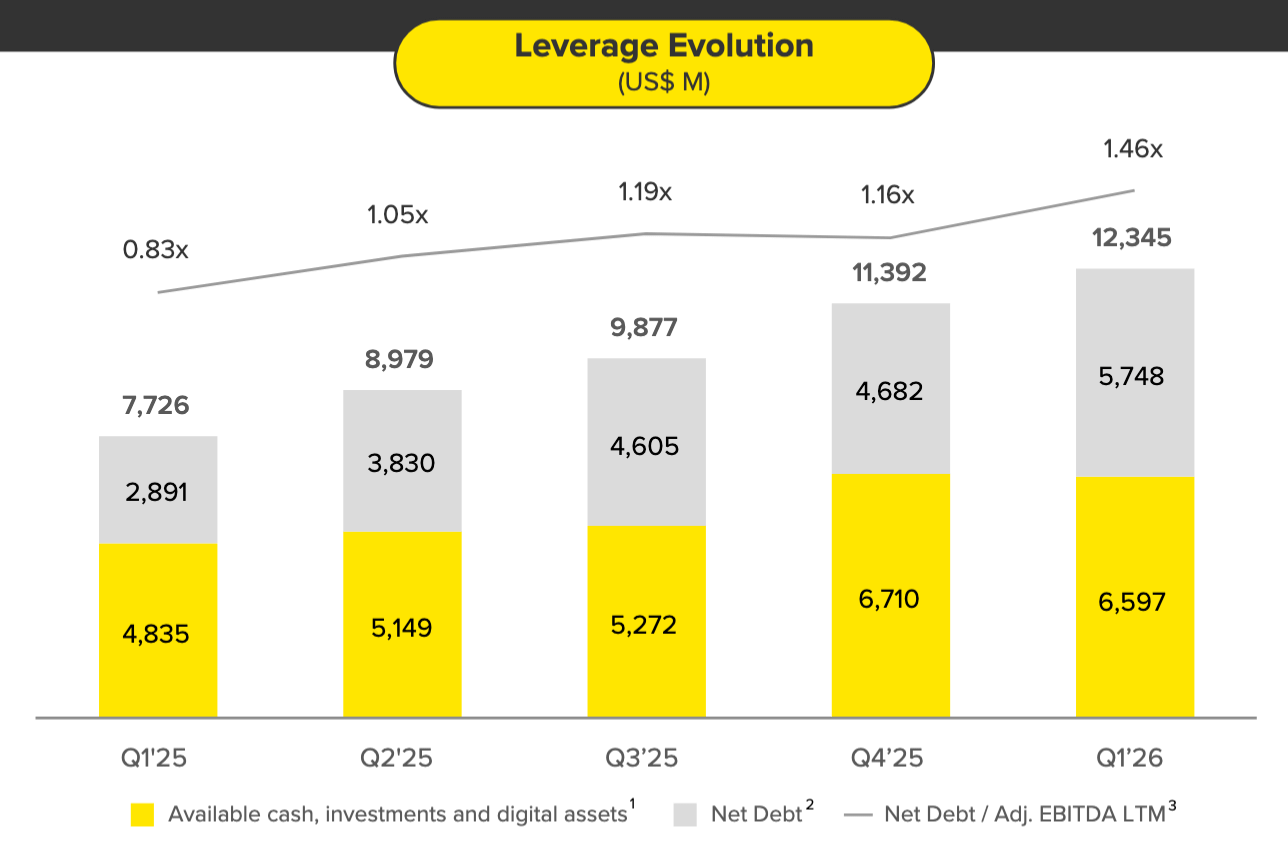

Net Debt / Last Twelve Months (LTM) Adjusted EBITDA stepped up to 1.46x (from 1.16x at year-end 2025) as the credit portfolio ramp pulls in working capital funding from the balance sheet. Cash and marketable securities $6.6 billion. Net debt $5.7 billion. Still investment-grade and almost entirely tied to fintech operations funding, but a clear directional shift from the cash-rich balance sheet of two years ago.

Marketplace: Brazil Volume Doubled, Logistics Density Compounding

The strongest part of the quarter was Brazil, and the country is the test of the entire investment thesis. From the Q1 2026 Letter to Shareholders:

“Brazil GMV growth accelerated to 38% YoY on an FX-neutral basis, supported by items sold growth of 56% YoY, up from 45% in Q4’25, 42% in Q3’25 and 26% in Q2’25. Our volume growth has doubled from a high base in just nine months. Unique buyer growth accelerated to 32% YoY – the fastest pace in five years. Conversion, frequency, retention and NPS are at record highs.”

Three things are happening simultaneously here. Volume growth is accelerating off a base that was already large. New buyer growth is the fastest in five years - the lower free-shipping threshold is bringing in new people, not just churning existing ones harder. Cohort behavior is improving: new buyer cohorts since the threshold change are purchasing more items across more categories with higher retention than older cohorts.

CEO Ariel Szarfsztejn, on the earnings call, on what underpins this:

“Our conversion rate in Brazil has increased 1 percentage point year-over-year. That’s a huge increase when you think about conversions. And all this feeds into the rapid growth that we are delivering, the record market shares, so we have never been in a stronger position on that regard.”

For a marketplace at MELI’s scale, a 1% lift in conversion is enormous. Conversion compounds through every other lever - ads inventory, frequency, retention, logistics density, cross-sell.

The other key data point is unit shipping cost. In Q1 2026, Brazil unit shipping costs fell 17% YoY in local currency, accelerating from the 11% reduction reported in Q4 2025, while absorbing 56% volume growth and the largest free-shipping expansion in MELI’s history. CFO Martin de Los Santos:

“Free shipping penetration reached a new record and unit economics continue to improve with cost per shipment down 17% year-over-year in local currency. In other words, higher demand is driving lower costs.”

This is not what defensive spending usually looks like. Defensive spending produces activity but worsens unit economics. What MELI is showing in Brazil is accelerating activity and improving unit economics at the same time, the signature of a network that is wider than its competitors and getting wider as it scales. Variable contribution per shipment for items in the R$19-79 range (the new free shipping bracket, ~$4-16 USD) has materially recovered: almost half of the May-to-June 2025 variable contribution (VC) drop has been offset by scale, productivity, efficiency and selective pricing. “Some ASP [Average Selling Price] ranges below R$79 are now breakeven”. That is the 2016 free shipping playbook re-running with faster economics.

Mercado Ads grew +73% YoY, roughly 4x the regional digital ad market growth in 2025 and continuing into Q1 2026. LatAm’s digital ad market is only ~50% of total ad spend (vs ~75% in the US), and MELI has the largest first-party data set on consumer behavior in the region. Ads is the high-margin, low-incremental-cost layer most likely to offset the credit cycle margin compression as the investment phase matures.

How MercadoLibre Stacks Up Against Shopee, Amazon, TikTok Shop, and the Brazilian Incumbents

The bear case for the marketplace is that competitive intensity has structurally raised the cost of staying #1. In Brazil, a market where MELI firmly commands a dominant 35-38% market share, Shopee now does an estimated ~$18-20 billion in annualized GMV and is profitable; Amazon has aggressively ramped up its investments, surpassing R$55 billion (~$10.8 billion) in total investments in Brazil over the last decade; TikTok Shop launched in Brazil in May 2025 and Banco Santander projects it could reach 9% of Brazilian e-commerce by 2028. Each of these competitors attacks one specific layer of what MELI has spent two decades building, and each one is a real challenger in their own right.

None of them attacks the full stack. The question is what each of them can credibly compress. MELI is the only player with a full-stack offer. Shopee attacks low-ASP frequency and cross-border supply. Amazon offers premium delivery but doesn’t combine it with credit, payments and a domestic first-party (1P) assortment in the same surface. Magazine Luiza, an incumbent Brazilian large retail chain, has the local retail heritage but management has explicitly chosen not to chase third-party (3P) GMV, which means its growth trajectory is structurally below MELI’s. TikTok Shop is genuinely interesting on the discovery layer but is years away from a logistics network of its own. Each MELI investment in the Q1 2026 trajectory maps cleanly to one of these threats: lower free shipping threshold defends the low-ASP frequency Shopee attacks; cross-border trade (CBT) defends the cross-border supply Temu, Shein and AliExpress attack; fulfillment defends the premium-delivery layer Amazon attacks; 1P merchandise defends the assortment depth Magazine Luiza historically led on.

The Brazilian e-commerce target addressable market (TAM), now tracking close to R$380 billion (~$75 billion), is expanding faster than the market share war is settling: it is projected to grow at a 19% CAGR through 2030 (per ABComm), half the growth rate of MELI, and even Shopee at +30% GMV growth and TikTok Shop at triple-digit ramp are not enough to absorb the entire incremental volume. Asked directly about Amazon’s recent moves in Brazil and competitive intensity more broadly, Szarfsztejn pointed at the same dynamic:

“We thrive in competitive environments. Competition makes us stronger. […] Every single engagement metric you look in MercadoLibre Brazil is strengthening — frequency, multi-category shopping, retention — all those are structural gains in our value proposition. Those are not short-term gains or growth that we are buying. […] This competitive intensity is also having a positive impact in the market as a whole by bringing new consumers from the offline world into the online world. […] The pie is increasing at a faster pace than it was before, and we are taking an even larger slice of that pie.”

In Mexico, the picture is similar but at an earlier stage: MELI revenue grew +50.8% YoY; MELI and Amazon now form a duopoly with 29-35% combined market share of a $52.6 billion online retail market growing at ~18% CAGR through 2031 (per Mordor Intelligence). In Argentina, the $25.7 billion market is projected to grow at 12.5-17% CAGR through 2031, where MELI holds a firm 60-65% of the market share and is the dominant marketplace and fintech with no comparable competitor.

Fintech: A Bank Inside the Marketplace At Different Stages by Country

The fintech engine is at three distinct stages depending on geography, and management was crisp about which stage each market is in. The Q1 2026 numbers in aggregate:

Mercado Pago monthly active users: 82.9 million (+29% YoY) - equivalent to onboarding nearly the entire population of Chile in a single year. MAU has now grown close to 30% YoY for eleven consecutive quarters.

Assets under management: $19.9 billion (+77% YoY), growing 2.6x faster than MAU, the signature of deepening engagement rather than just user acquisition.

Credit portfolio: $14.6 billion gross, a +87% YoY increase - the largest quarterly nominal increase ever. Credit card portfolio $6.6 billion (+104% YoY) now represents 46% of the total credit book (vs 42% Q1 2025). 2.7 million cards issued in Q1 2026 alone.

Acquiring Total Payment Volume (TPV): $56 billion (+39% YoY) - Brazil +26%, Mexico +46%, Argentina +55%, Chile +69%; market share gains across every geography.

The Fintech cohort4 logic by country:

Brazil (5+ years in): Older credit card cohorts are increasingly offsetting the dilutive impact of new cohorts. The whole portfolio is approaching profitability acceleration.

Mexico: “Attractive projected paybacks” - issuance is being deliberately accelerated.

Argentina: Credit card launched in late 2025; “early stages of investment”. Cohort behavior so far is “very similar to our first steps in Brazil”.

The cross-sell flywheel is the cleanest evidence that the ecosystem is widening, not narrowing. The share of monthly active sellers (MAS) using Mercado Crédito has jumped from 26.3% in Q1 2025 to 36% in Q1 2026.

On Argentina specifically, a market where the financial system is showing rising delinquency, Fintech President Osvaldo Giménez drew a sharp contrast with the local banking system on the call:

“I would say that in general, the 15-90 day NPL [Non-Performing Loan ratio] in Argentina has improved sequentially. When we look at the market, we see that some banks are having worsening NPLs, but that has not been our case. […] We have several advantages. We are issuing loans with very short durations relative to the banks and we have a very nimble approach to pricing those loans. And we have high levels of principality in Argentina. A lot of our users use their Mercado Pago account every day, and we have very sophisticated underwriting models.”

This is the data-and-distribution moat showing up where it should: MELI is underwriting better than the incumbent banks in a deteriorating Argentine credit market because it has a data advantage with its users using Mercado Pago daily, many of which also buy online on the marketplace. The 10-Q discloses Argentina’s average inter-annual inflation rate at 32.7% for Q1 2026, a brutal underwriting environment, in which MELI’s 15-90 day NPL improved sequentially.

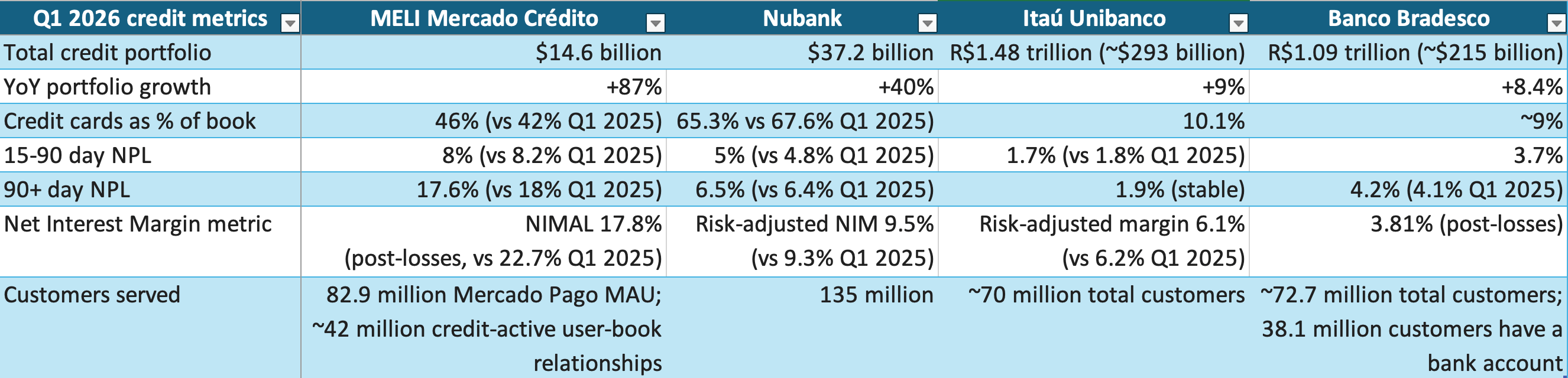

How MercadoLibre’s Credit Book Compares to LatAm Banks

MELI is now operating credit at meaningful scale. To calibrate what “scale” means, and what to make of the headline NIMAL and NPL movements, it is worth comparing Mercado Crédito to the largest LatAm banks: Nubank (NU 0.00%↑, digital, Brazil-led), Itaú Unibanco (ITUB 0.00%↑, Brazil incumbent), Banco Bradesco (BBD 0.00%↑, Brazil incumbent):

MELI’s credit book is small relative to the Brazilian banking incumbents. At $14.6 billion it is 5% the size of Itaú’s book and 39.2% the size of the main competitor, Nubank’s. It is also the fastest-growing book by a wide margin: +87% YoY against Nubank’s +40%. The runway looks enormous when the closest comparable credit book, Itaú’s, is at $293 billion and growing single-digits.

MELI’s Non-Performing Loans (NPL) are higher than the bank comparison set, and that is by design. MELI lends to merchants and consumers the traditional banking system has historically overlooked or underserved, exactly the segment with structurally higher loss rates. MELI’s 15-90 day NPL is 8% (0.2% YoY), and 90+ NPL is 17.6% (-0.4% YoY), slight improvements YoY. Nubank’s 15-90 NPL sits at 5% (+0.2% YoY) and 90+ NPL at 6.5% (+0.1% YoY). Bradesco’s 90+ NPL sits at 4.2% (+0.1% YoY). Both competitors have higher NPLs YoY and MELI’s cohort risk metrics are holding up better than peers’ on direction, which is a signal I pay attention to.

The relevant question is not whether MELI’s NPLs are higher than Itaú’s or Bradesco’s; it is whether the spread MELI charges compensates for the loss rate. NIMAL of 17.8% (post-losses ratio) compared to Nubank’s risk-adjusted NIM of 9.5% (the most apples-to-apples comparable, since both subtract realized losses) suggests the answer is yes, even after this quarter’s YoY compression. Itaú and Bradesco operate at low-to-mid single-digit risk-adjusted net interest margins in much lower-risk segments - different business, different return profile.

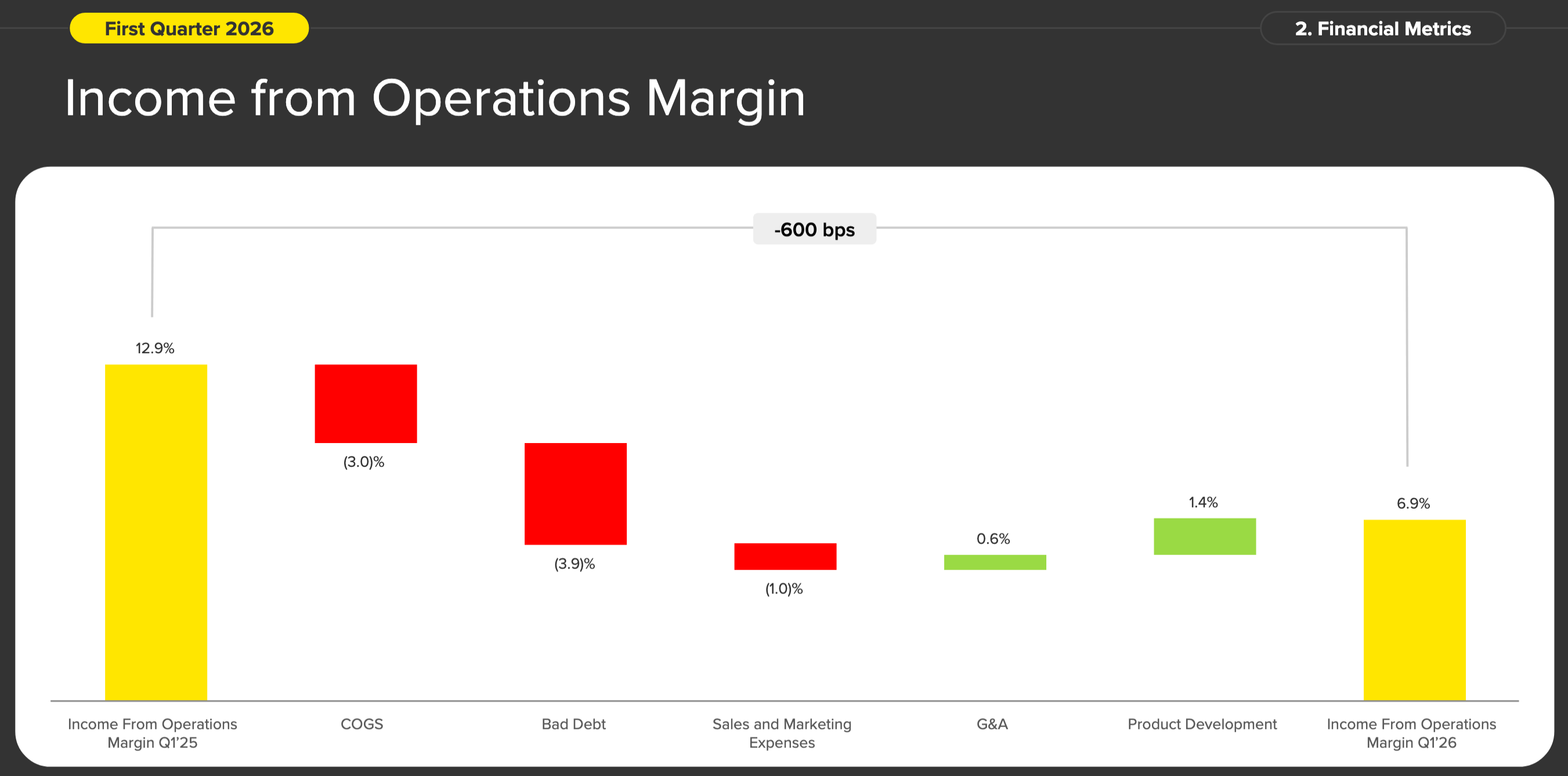

Margins Compressed by Design and Management Quantified Every Line

Q1 gross profit was $3.86 billion at a 43.7% gross margin (-3% YoY); income from operations $611 million, 6.9% operating margin, -19.9% YoY.

The 6% YoY operating margin compression breaks down, and management was explicit about the compression drivers, line by line:

Cost of Goods Sold (COGS) - lower free shipping threshold in Brazil plus fast 1P scaling: -3%

Provisions for doubtful accounts (Bad Debt) - credit portfolio growing faster than revenue and longer loan terms in Brazil: -3.9%

Sales and marketing - affiliate and performance marketing channel scaling: -1%

General and administration - operating leverage: +0.6%

Product & technology - AI-driven productivity gains: +1.4%

The provisions line generated 3.9% of margin compression. Two third is mechanical: the credit book grew 87% YoY while consolidated revenue grew 49% YoY. Under U.S. GAAP, MELI must provision for the full expected loss of every new loan up front, well before that loan generates any revenue. When you double a credit portfolio in a year, you book provisions today for losses that may materialize over months. The remaining one third of the compression is the deliberate Brazilian consumer loan extension. Giménez framed the trade-off:

“Basically, our duration was fairly small, it was only 5 months and it was very profitable. It continues to be very profitable, less so than a year ago, but it continues to be fully profitable. […] We can’t change the periods at which we lend at any point in time, but we wanted to experiment with this, and this confirmed that we could do this in a profitable way.”

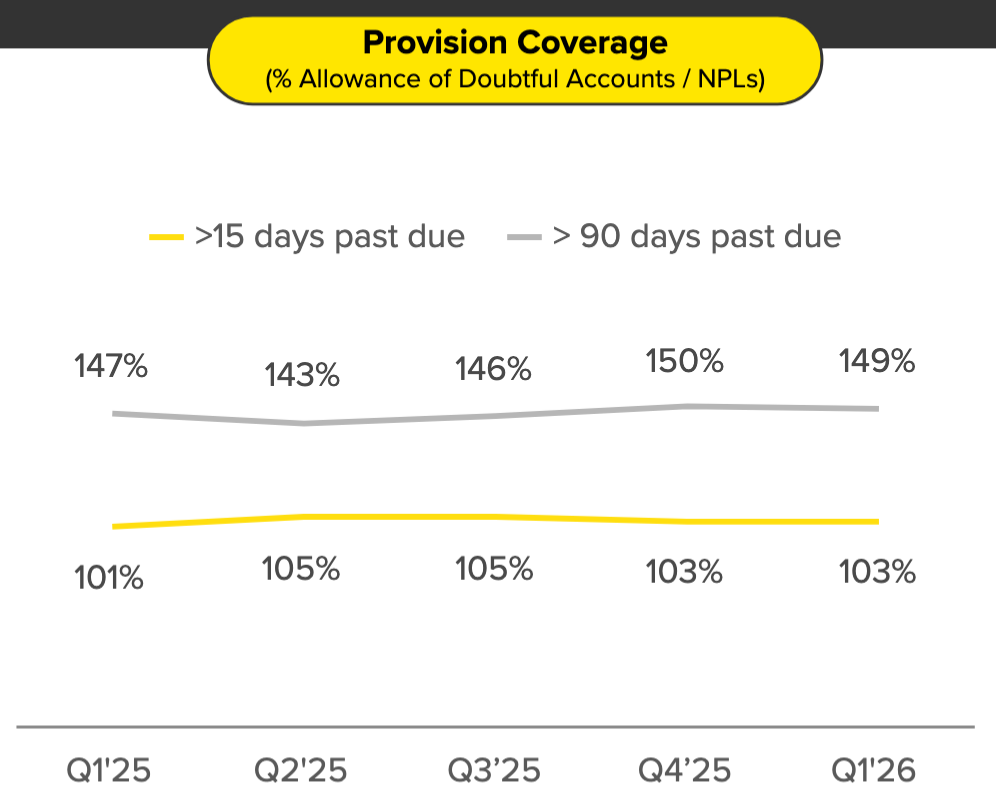

The deterioration the market is reading off the -6% YoY margin step-down is overwhelmingly provisioning ahead of growth, not realized credit deterioration. MELI is reserved at 103% of all >15-day past-due loans and 149% of >90-day past-due loans. The book is over-reserved, not under-reserved.

The product and technology line is the surprising bright spot. Headcount grew 8% YoY (a carryover from 2025 hiring) but management said productivity KPIs are growing 7-10x faster. From the letter:

“We rolled out our first AI-powered search experience in our marketplace in Q1’26, shifting the architecture away from keywords and rebuilding it around LLMs. In Brazil and Mexico, the improvement in product relevance led to uplifts in conversion and click-through-rate for sponsored listings, both of which represent incremental revenue. […] More broadly, we have rolled out Claude Cowork to 31,000 employees, making Mercado Libre one of the earliest, large-scale enterprise adopters globally.”

Engineer headcount is now planned to be broadly flat in 2026 thanks to AI productivity. That is the closest thing yet to evidence that AI-driven cost leverage is a real offset to the investment intensity elsewhere.

Who Captures the Surplus?

MELI is creating enormous value across LatAm: cheaper shipping for buyers, working capital credit for sellers, first-time access to credit cards and savings products for the underbanked, advertising precision for brands, faster delivery for everyone. The business is winning. The stock depends on a different question - how much of that created value reaches the shareholders after shipping subsidies, seller incentives, provision expense, credit losses, fulfillment CapEx, and funding costs.

Lowering the free shipping threshold transfers surplus from the company to the buyer; lowering seller take-rates transfers surplus from the company to the seller; provisioning aggressively against a credit book where realized losses run materially below provisions transfers surplus from current shareholders to future ones (because the reserves either get released or absorb future losses without flowing through future income statements). MELI is making explicit choices about how to distribute the surplus the ecosystem generates, and Q1 2026 is the most aggressive pro-buyer/pro-seller/pro-future-shareholder mix it has ever set the dial to.

There is a useful distinction worth drawing here, because the two big investment categories work very differently.

Logistics scales like physics. Move more packages through the same network and the next package gets cheaper than the last one - better routing, better utilization, better line-haul density, better fulfillment flow. Density compounds. The Q1 2026 17% unit cost reduction on 56% volume growth is exactly this dynamic playing out. Once the network is built, more volume improves the economics.

Credit does not scale like physics. Credit improves only if underwriting models, funding costs, repayment behavior, and cohort seasoning collectively improve faster than provisions consume the P&L. Mercado Pago has structural advantages - first-party transaction data, daily user engagement, short loan duration giving fast feedback loops, the cohort-by-cohort underwriting visibility Giménez described, but each new product launch (a longer-duration personal loan, a new geography for the credit card, a new segment of underwritten customer) resets a portion of the seasoning clock. The Q1 2026 numbers say the underwriting models are still earning the right to keep extending.

The bull case is that the data-and-distribution moat MELI has built across both engines lets it capture an outsized share of the surplus over time, through ad monetization (4x market growth), through credit cohort seasoning (older Brazil cohorts now offsetting new cohort dilution), through fulfillment density (17% YoY unit cost reductions), and through the cross-sell flywheel (36% of merchants using credit, vs 26.3% a year ago). The bear case is that competition keeps the dial pinned at the current investment intensity for years, the credit cohorts season more slowly than expected, and the margin profile is structurally lower than the 13% the market priced in two years ago.

I think the bull case wins over time, while I take the surplus question more seriously than I did a year ago.

Valuation: Anchoring on Owner’s Earnings

For a business simultaneously scaling a credit portfolio at 87% YoY and a logistics/1P/CBT investment cycle, neither reported GAAP earnings nor reported free cash flow captures underlying earning power. Reported adjusted free cash flow (AFCF) was -$56 million in Q1 2026, seasonally low and dominated by the $1.95 billion Q1 increase in loans receivable. Neither line tells you what the business actually generates if it stopped reinvesting in growth.

I find Buffett’s owner’s earnings frame a suitable anchor here: reported earnings + non-cash charges - capital required to maintain the business at current scale, with growth investment held separate. For Q1 2026, working bottom-up: $1.53 billion in Q1 2026 normalized owner’s earnings = $417 million (net income) + $246 million (depreciation and amortization) + $100 (non-cash interest & debt-cost amortization) + $830 million (provision for doubtful accounts attributable to credit book growth, two third of $1.24 billion) + $96 million (non-cash long-term retention compensation) - $162 million (maintenance CapEx, 60% of $271 million). Annualized normalized earnings run-rate is $6.12 billion.

On today’s ~$78.4 billion market capitalization, the company is selling for 12.8x normalized owner’s earnings, a modest multiple for a business compounding revenue above 30% for 29 consecutive quarters, accelerating to 49% growth, and explicit management runway language describing the large opportunity ahead.

Final Thoughts

Q1 2026 confirms the margin compression is part of the strategy: Brazil items sold doubled in nine months, unit shipping costs fell 17% YoY while volume rose 56%, credit card NPL improved while the portfolio doubled, conversion lifted +1% in Brazil, advertising compounded at 4x the regional ad market, and AI-driven productivity contributed +1.4% of operating leverage for the first time. Each of those is a structural moat-widening result.

My question is how much of the surplus MELI is creating reaches shareholders. I am willing to underwrite that the answer is enough, for three reasons. The cross-sell flywheel widening from 26.3% to 36% of merchants on credit is the cleanest sign that the ecosystem keeps accreting value to MELI rather than leaking it to competitors. Advertising, where MELI grows at 4x the digital ad market with first-party data no competitor can replicate, is the highest-margin offset to credit-cycle compression and is barely 5% of revenue today. Fintech cohort math on the Brazil credit card: five years of seasoning in the country, second only to Nubank by fintech scale, says older cohorts are now meaningfully offsetting the dilution from new ones.

I see MELI as a long-term compounder with a long runway of growth ahead, the closest analog to early-2010s is Amazon, in a region where digital commerce, digital payments and credit penetration are all still in early innings. I have been using the stock weakness as a buying opportunity.

The opening stance and closing words of the Q1 2026 Letter to Shareholders are a statement of intent, and I take them at face value:

“We have a once-in-a-generation opportunity to transform how hundreds of millions of Latin Americans shop, pay and access financial services. […] For Mercado Libre and Latin America, the best is yet to come.”

In MELI’s terms, conversion is the percentage of marketplace visits that result in a completed purchase. Higher conversion means the same incoming traffic produces more orders, which produces more shipments, which improves logistics density, which lowers per-package cost — and it produces more sponsored-listing impressions to monetize, more credit-card transactions, more frequency cohort effects. A single percentage point of conversion lift cascades across the whole flywheel.

Average loan duration is the average scheduled repayment period of a loan portfolio. A longer duration means borrowers repay over more installments, generating more interest income per loan but also requiring larger upfront expected-loss provisions under U.S. GAAP, which mechanically compresses near-term NIMAL even when cohort credit quality is stable.

NIMAL (Net Interest Margin After Losses) is MELI’s measure of the spread between credit revenues and the combined cost of provisions for doubtful accounts and funding, expressed as a percentage of the average loan portfolio. It is structurally lower for credit cards (because the full expected lifetime loss must be provisioned up-front when each card is issued) and improves as cohorts season.

A fintech cohort is the group of loans or credit cards originated in a given period. Under U.S. GAAP, the full expected lifetime credit loss must be provisioned the moment a loan is issued, before any revenue accrues. New cohorts are therefore a P&L drag at origination: heavy upfront provisions, minimal income. Seasoned cohorts - those that have run for several quarters - have already had losses confirmed (charged off) or shown the original provision was conservative, and they are reliably profitable on the interest and fees that have flowed through. In a fast-growing credit book like MELI’s, new cohorts dominate the mix and depress blended NIMAL. As the book matures and growth moderates, older cohorts come to dominate the mix and NIMAL recovers.

One of the best Q1 breakdowns I've read on this — the logistics vs credit distinction ("scales like physics vs doesn't") is exactly the right frame and most coverage doesn't make it.

One thing worth adding to the valuation section: the reported AFCF of -$56mm will alarm readers who don't read the footnotes. The $1.95B increase in loans receivable running through operating activities is the entire explanation — that capital is a financial asset earning interest, not a cost. Reported OCF was $3.2B in Q1 alone, ~$12.1B for FY2025, a 15% yield on ~$80B market cap. Your owner's earnings frame is the right instinct; OCF yield gets you to the same place faster for the sceptics.

Also sitting at 12-15% of portfolio and adding on weakness. Published a full IC last weekend with scenario framework and financial model if useful.

https://substack.com/@wallmanresearch/note/p-199050829

Margin compression by design is exactly the right framing.

49% revenue growth while deliberately reinvesting every dollar back into logistics density, fintech rails, and credit. The market sees the margin and panics. The filing shows a company building infrastructure competitors can’t replicate on any timeline.

Brazil items sold doubled in nine months. 82.9M MAUs. Credit portfolio up 87%. This is the build phase. The harvest comes later.

In at $1,750. Holding for at least five years.