Amazon's Q4 2025 Earnings and 2026 Outlook: Strong Results and a $200B CapEx Plan

Solid fundamentals, an outsized CapEx guide, and the signposts that will define 2026

“We expect to invest about $200 billion in capital expenditures across Amazon, but predominantly in AWS because we have very high demand, […] and we’re monetizing capacity as fast as we can install it.”

— Andy Jassy, Amazon CEO

Amazon’s (AMZN 0.00%↑) Q4 2025 results were fundamentally solid: double-digit revenue growth, accelerating AWS growth, and rising operating income, but the market’s attention snapped to one number. The company expects to invest $200 billion in capital expenditures (CapEx) during 2026.

The market selloff didn’t happen in a vacuum. The market has been in a “CapEx panic” regime: Big Tech has been getting hit whether it spends a lot or a little, and the debate has turned into a referendum on whether hyperscalers can earn attractive returns on an unprecedented scale of investment.

Amazon was no exception. In after-hours trading immediately after the earnings release (Feb 5, 2026), shares fell about 11% as investors reacted to the magnitude of the 2026 CapEx plan - up 56% from 2025.

The near-term story isn’t “demand is weak”. It’s that Amazon is choosing to convert today’s cash-generating power into capacity (AI infrastructure, chips, robotics, and low Earth orbit satellites), and investors are repricing the uncertainty around how quickly that capacity translates into incremental profit.

In this article, I analyze Amazon’s financial performance, its business segments, and why I remain bullish despite near-term volatility, while also laying out the signposts that will determine whether the $200 billion posture is disciplined or reckless.

Quarterly Highlights

The Q4 2025 results had plenty of moving parts, but four data points captured my attention:

Revenue stayed in double-digit growth territory: sales grew to $213.4 billion, up 14% year over year (YoY). Beyond segment reporting, the internal mix continued shifting toward services: Q4’s advertising services rose to $21.3 billion (+23% YoY) and third-party seller services rose to $52.8 billion (+11% YoY).

Operating income rose to $25 billion, up 18% YoY, but Q4 included notable special charges - $2.4 billion in tax dispute resolution/litigation settlement, severance, and physical-store impairments. Stripping those out, operating income would have been $27.4 (+29.2% YoY), useful context when comparing quarter-to-quarter margin narratives.

The engine that justifies the investment cycle accelerated: AWS revenue grew 24% YoY to $35.6 billion, its fastest growth in over 3 years. In Jassy own words, “AWS is now a $142 billion annualized run rate business”. AWS operating margin was 35%, down from 36.9% in the prior-year quarter. Margin matters because a meaningful portion of the $200 billion build-out will flow through AWS depreciation and operating expense, and the market is already testing whether AI-era cloud returns can stay attractive.

AWS is larger than Azure and Google Cloud. So even if peers post higher percentage growth in a given quarter, AWS is still adding massive absolute dollars. Jassy noted that “[…] it’s very different having 24% year-over-year growth on a $142 billion annualized run rate than to have a higher percentage growth on a meaningfully smaller base”. He emphasized AWS’s embeddedness in large enterprises, noting that more S&P 500 companies run “AWS as their primary cloud provider” than the next two largest competitors combined - a moat that’s hard to ignore when evaluating whether demand is real or speculative.

Business Segments’ Performance in 2025

The full-year 2025 results clarify the core reality of Amazon’s model: retail is the scale flywheel with improving profitability, AWS is the operating profit engine, and services (ads, third-party, subscriptions) increasingly subsidize both.

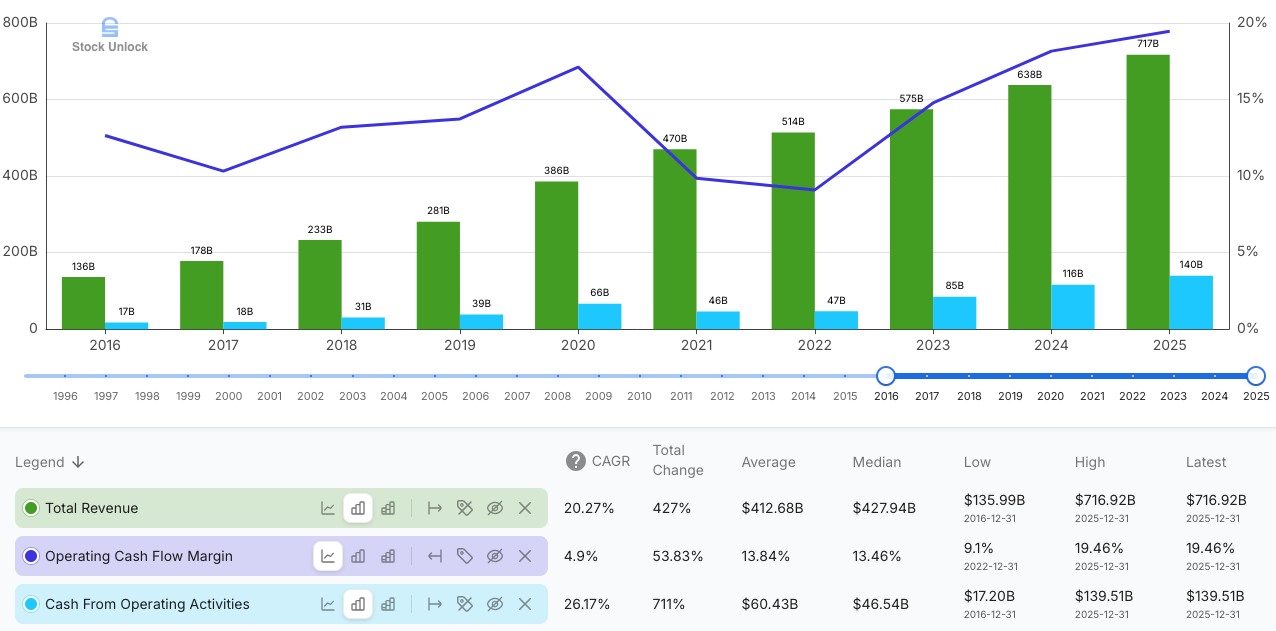

At the consolidated level, 2025 revenue was $716.9 billion (+12% YoY) and operating cash flow (OCF) was $139.5 billion (+20% YoY), a 19.5% OCF margin, while free cash flow (FCF) fell to $11.2 billion. Amazon explicitly attributed the FCF decline to a $50.7 billion YoY increase in CapEx, stating that the increase “primarily reflects investments in artificial intelligence”.

By segment for the year:

North America delivered $426.3 billion of revenue (+10% YoY) with operating income of $29.6 billion (+18.4% YoY), a 6.9% operating margin. This is the “quiet win”: Amazon keeps extracting efficiency from a logistics machine that many still think of as structurally low-margin.

International produced $161.9 billion of revenue (+13% YoY) with operating income of $4.7 billion (+23.7% YoY), a 2.9% operating margin. International remains the least “finished” part of the story - progress is real, but the segment still absorbs local fulfillment build-out and is more exposed to local execution and macro variability.

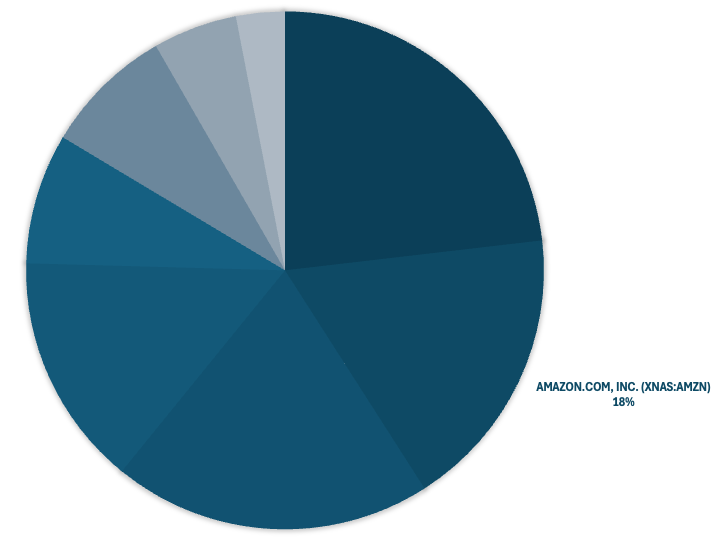

AWS delivered $128.7 billion of revenue (+20% YoY) with operating income of $45.6 billion (+14.6% YoY), a 35.4% operating margin. AWS generated about 57% of total operating income while representing about 18% of total revenue. This is what gives Amazon the confidence to press the spending pedal harder and tolerate near-term FCF compression to protect and extend AWS leadership, even as the market demands proof that margins won’t structurally reset lower.

Beyond the segment numbers, services are increasingly the margin layer. Advertising grew 23% YoY in Q4 to roughly $21.3 billion, helped by Prime Video’s ad tiers, and Amazon is reducing advertiser friction by unifying Demand Side Platform (DSP) and Sponsored Ads into a single campaign workflow with AI-assisted tools.

Finally, Amazon is pushing AI monetization inside retail, not just AWS. Jassy emphasized:

“Our creative agent lets advertisers research, brainstorm and generate full funnel ad campaigns from concept to completion using conversational guidance in Amazon’s retail data, transforming what was a week-long process into just hours.”

The CEO also highlighted agentic shopping features like Rufus, noting users are more likely to complete a purchase and can automate tasks like research, price tracking, and auto-buy, potentially turning AI spend into higher conversion and more high-margin attach over time.

Capital Intensity and Balance Sheet

Capital intensity is visible on the balance sheet.

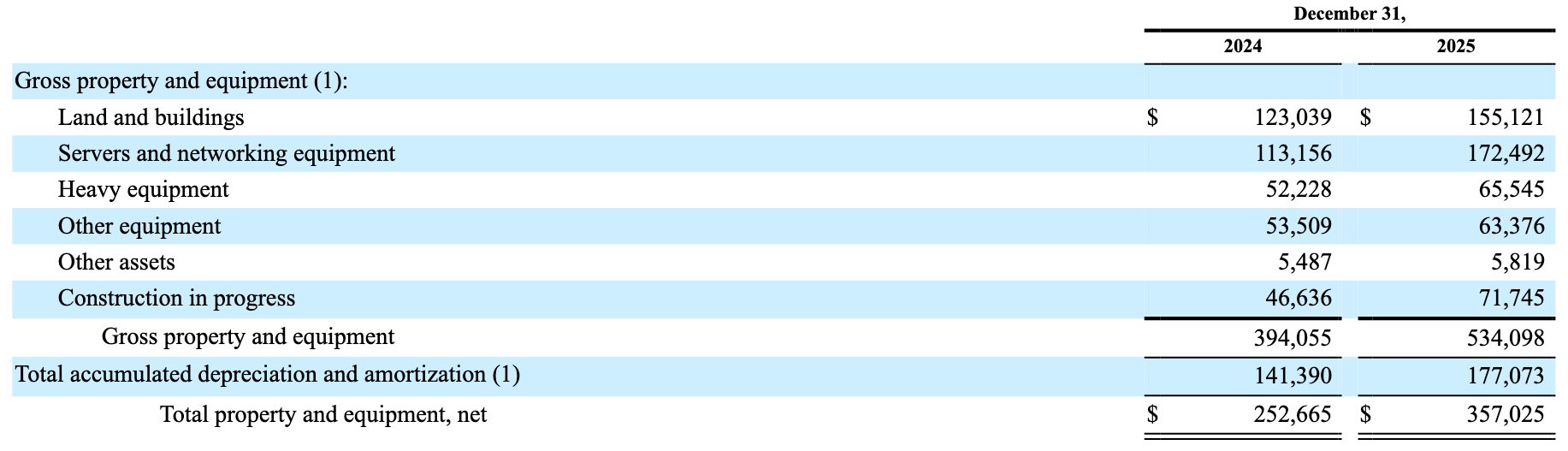

Gross property and equipment rose to $534.1 billion (+35.5% YoY) in 2025, while net property and equipment increased to $357 billion (+41.3% YoY). Within that, servers and networking equipment increased to $172.5 billion (+52.4% YoY) and construction-in-progress increased to $71.7 billion (+53.9% YoY) - two line items that are consistent with hyperscaler data center build-outs, and the supporting “assembly line” behind them: land, concrete, power, cooling, networking, switches, memory, chips, and GPUs.

Depreciation and amortization expense on property and equipment rose to $41.9 billion (+30.5% YoY) in 2025, which provides a preview of the net income margin headwind that will grow if CapEx continues to accelerate. This is one reason some investors get uncomfortable: even if the cash is there, the accounting drag becomes more visible before the payoff does.

The balance sheet shows funding flexibility, even in a heavy-investment year. At year-end, Amazon reported $123 billion of cash, cash equivalents, and marketable securities (net of restricted amounts).

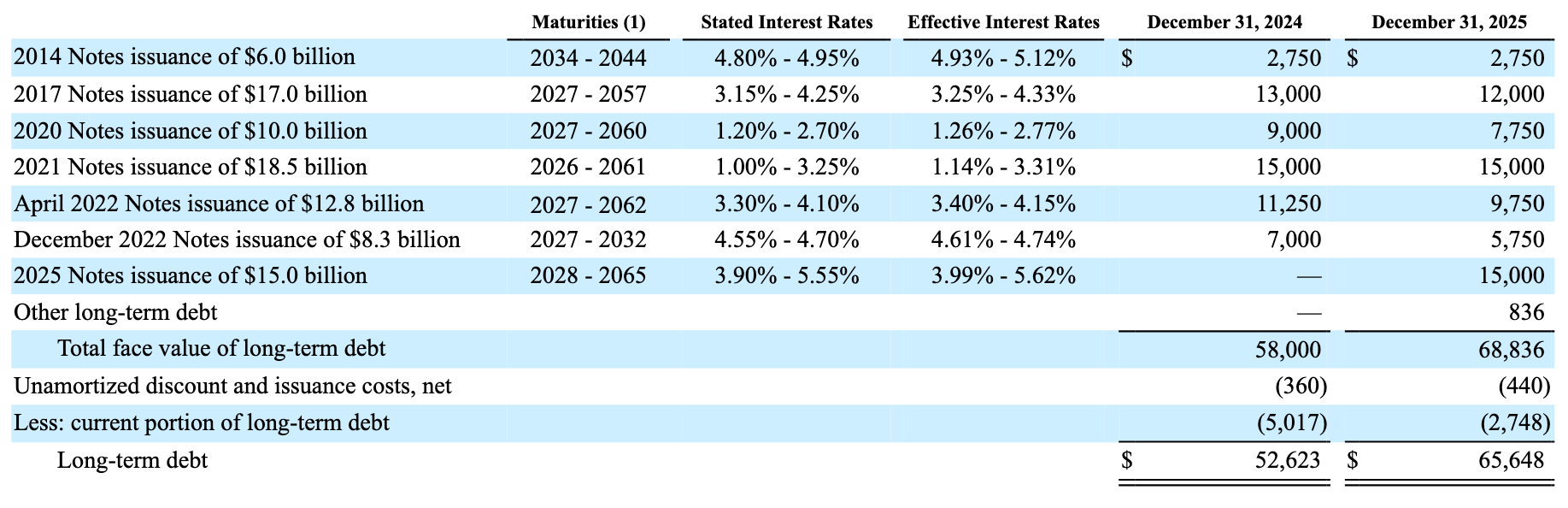

Long-term debt was $65.6 billion, and Amazon disclosed it had $68 billion of unsecured senior notes outstanding, including $15 billion issued in November 2025 for general corporate purposes.

The company also reported no share buybacks, which matters because it keeps “dry powder” available for CapEx at the expense of near-term capital returns. That choice is part of the Amazon identity, and one reason Amazon can outspend peers without immediately turning the conversation into dividends, buybacks, and capital return tradeoffs.

Interpreting the 2026 CapEx Plan

“We have deep experience understanding demand signals in the AWS business and then turning that capacity into strong return on invested capital.”

— Andy Jassy

Amazon’s $200 billion 2026 CapEx guide is mostly a message-versus-optics issue. Management framed the step-up as demand-driven, not speculative: Jassy anticipates “strong long-term return on invested capital” and he emphasized the spend will be “predominantly in AWS”, because customers “really want AWS for core and AI workloads” and Amazon is “monetizing capacity as fast as we can install it”.

The selloff reflects investors’ sentiment, not a solvency issue. $200 billion is well above expectations and, by definition, compresses near-term FCF, fueling the broader “Big Tech CapEx crowds out short-term returns” narrative. The better way to view it is against Amazon’s run-rate: cash CapEx rose from $77.7 billion (2024) to $128.3 billion (2025), and $200 billion implies another 56% step-up. Amazon can fund that with strong OCF and a liquid balance sheet; the uncertainty is payback timing as depreciation rises.

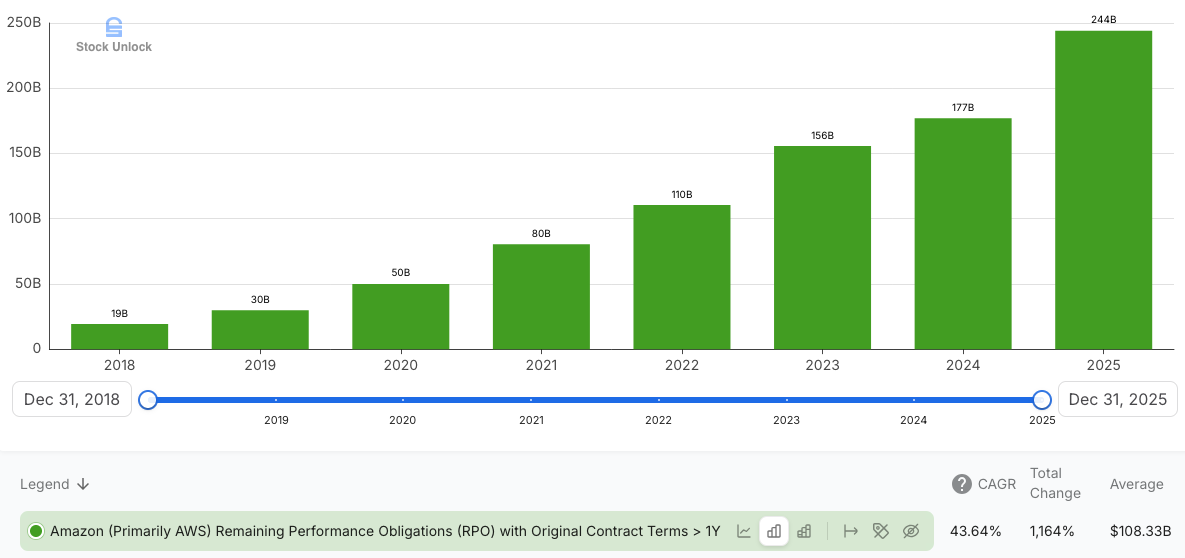

The bull case is demand visibility plus better unit economics. Amazon disclosed in the 2025 10-K filing $244 billion of long-duration performance obligations (mostly AWS) with a 4.1-year life, a backlog-like support for a multi-year build if utilization and pricing hold.

Jassy also framed demand as “barbelled”: AI labs as near-term anchor tenants, with enterprise productivity/cost-avoidance workloads broadening over time. On economics, Trainium + Graviton are now above $10 billion run-rate and growing triple digits; Trainium2 is sold out (1.4 million chips) and underpins most Bedrock inference (100,000+ customers), with Trainium3 largely committed by mid-2026 and Trainium4 coming in 2027. Graviton is up to 40% more price-performant than leading x86 chips, helping bend AWS’s cost curve.

The bear case is classic overbuild risk in a crowded cycle: power/chip constraints and price pressure can compress returns before they show up. If OCF stays near $140 billion and cash CapEx hits $200 billion, FCF likely goes negative, shifting scrutiny to funding mix (cash vs. debt) and whether ROIC holds.

Key Signposts to Watch Through 2026

If the “catalysts” case is the strategy for years to come, 2026 is about widening the business’ moats. A $200 billion CapEx posture is disciplined only if incremental capacity converts into durable AWS monetization and acceptable incremental returns once depreciation and ramp costs hit the P&L.

First, AWS growth and margin durability. Amazon is tying most spend to AWS and saying demand is the constraint. The signpost is sustained re-acceleration as capacity comes online, without a lasting margin reset downward after the build-out peak.

Second, backlog quality. The $244 billion of long-duration performance obligations is the closest thing to a backlog signal. I will be watching whether it keeps expanding and whether the remaining life stays healthy - those two metrics shape confidence in utilization and pricing.

“Our backlog is $244 billion. That’s up 40% year-over-year [and] up 22% quarter-over-quarter.”

— Andy Jassy

Third, custom silicon commercialization. Trainium and Graviton matter most if they scale as products, not just internal advantage. The signpost is adoption into major workloads and growing revenue mix, because that’s how Amazon bends the compute cost curve in its favor.

Fourth, cash versus optics. I expect 2026 margin noise as depreciation and ramp costs rise. I don’t anchor on FCF in isolation; I anchor on OCF and the balance sheet path, especially whether any FCF gap is funded by cash drawdown or incremental debt.

Valuation: Is Amazon Undervalued?

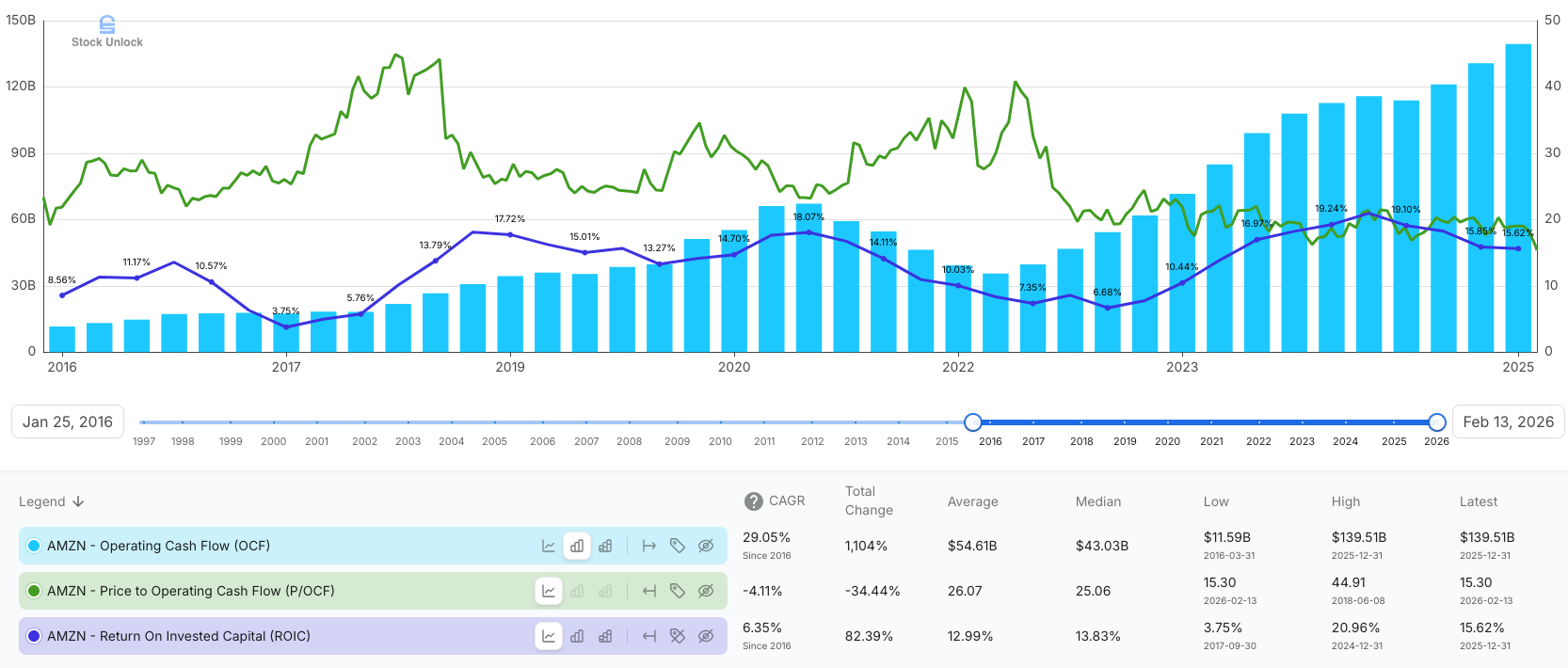

With CapEx spiking, I value Amazon on OCF, not on GAAP earnings or near-term FCF. OCF is cleaner, and it’s still compounding. In 2025, Amazon generated $139.5 billion of OCF (+20% YoY). The chart also shows why the stock reacted so violently: while OCF has marched higher, the P/OCF multiple has compressed sharply. At 15.3x today, it’s the low end of the past decade range and well below the historical median of 25x.

To translate that into an underwriting-style fair value, here’s a simple OCF framework:

Start with 2025 OCF of $139.5 billion and grow it at 20% per year for five years: OCF reaches $347.2 billion in year five.

Assume dilution of 1.15% per year: shares rise from 10.863 billion to 11.5 billion.

Apply a 20x P/OCF multiple (below the longer-run median): implied year-five price is $603.64.

Discount back at 10% for five years: present fair value is $374.81 per share.

This isn’t a target price; it’s a sanity check on what the stock could be worth if OCF continues compounding at a strong rate and the market rerates the multiple closer to a more normal band once the CapEx cycle is better understood. The risk is straightforward: if the $200 billion build leads to a structural ROIC or margin reset in AWS (or OCF growth slows materially), the multiple should stay depressed, and the math changes quickly.

Despite short-term market concerns, my long-term investment thesis remains intact. Should negative sentiment persist, I will consider increasing my position, even though it is already my second-largest holding.

Final Thoughts

The market’s reaction to the earnings report wasn’t really about the quarter. It was about underwriting a steeper investment slope. A $200 billion 2026 CapEx guide forces investors to choose between two narratives: “Amazon is overbuilding into a crowded AI cycle”, or “Amazon is pulling forward capacity into demand it can already see”.

Amazon’s Q4 2025 didn’t read like a business losing momentum. It read like a business choosing to compress near-term FCF to extend its lead in infrastructure and AI-adjacent services, and asking shareholders to underwrite the timing risk. Whether that’s attractive depends on your tolerance for a “build now, harvest later” cycle, but the underlying operating trajectory (especially AWS re-acceleration and OCF growth) is the part I treat as signal.

I still lean toward the disciplined-investment interpretation. The operating picture is solid, and the balance sheet gives Amazon room to invest without turning this into a financing story. If the incremental spend shows up as sustained AWS growth with resilient margins, expanding long-term commitments, and rising commercial adoption of Trainium/Graviton, the 2026 CapEx plan will look less like a bet and more like a deliberate move to extend cost and scale advantages.

Investors are right to demand proof. Depreciation and ramp costs will pressure reported margins, and FCF may look worse before it looks better. That’s why the signposts matter. Through 2026, the debate won’t be settled by one quarter’s FCF print; it will be settled by whether Amazon converts capacity into durable earnings power, without sacrificing pricing discipline or letting the build-out reset AWS returns structurally lower.